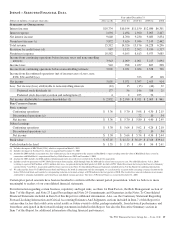

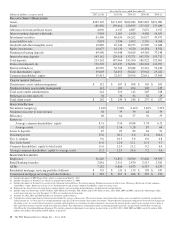

PNC Bank 2012 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

ITEM

7–M

ANAGEMENT

’

S

D

ISCUSSION AND

A

NALYSIS OF

F

INANCIAL

C

ONDITION AND

R

ESULTS OF

O

PERATIONS

E

XECUTIVE

S

UMMARY

K

EY

S

TRATEGIC

G

OALS

At PNC we manage our company for the long term. We are

focused on revenue growth, with an emphasis on deepening

customer relationships and increasing fee income, while

reducing expenses. Our goal for 2013 is to deliver positive

operating leverage and create momentum going into 2014,

while investing for the future, and managing risk and capital.

We continue to invest in our products, markets and brand, and

embrace our corporate responsibility to the communities

where we do business.

The primary drivers of revenue are the acquisition, expansion

and retention of customer relationships. We strive to expand

and deepen customer relationships by offering convenient

banking options and innovative technology solutions,

providing a broad range of fee-based and credit products and

services, focusing on customer service, and enhancing our

brand. This strategy is designed to give our customers choices

based on their needs. Our approach is focused on effectively

growing targeted market share and “share of wallet” rather

than short term fee revenue optimization. We may also grow

revenue through appropriate and targeted acquisitions and, in

certain businesses, by expanding into new geographical

markets.

PNC faces a variety of risks that may impact various aspects

of our risk profile from time to time. The extent of such

impacts may vary depending on factors such as the current

economic, political and regulatory environment, merger and

acquisition activity, and operational challenges. Many of these

risks and our risk management strategies are described in

more detail elsewhere in this Report.

Our priorities for 2013 are to build capital to support client

growth and business investment, maintain appropriate capital

in light of economic uncertainty and the Basel III framework

and return excess capital to shareholders, subject to regulatory

approval. We continue to work to improve the quality of our

capital and expect to build capital through retained earnings.

PNC continues to maintain a strong bank holding company

liquidity position. See the Capital and Liquidity Actions

section of this Executive Summary, the Funding and Capital

Sources section of the Consolidated Balance Sheet Review

section and the Liquidity Risk Management section of this

Financial Review and the Supervision and Regulation section

in Item 1 of this Report.

RBC B

ANK

(USA) A

CQUISITION

On March 2, 2012, we acquired 100% of the issued and

outstanding common stock of RBC Bank (USA), the U.S.

retail banking subsidiary of Royal Bank of Canada. As part of

the acquisition, PNC also purchased a credit card portfolio

from RBC Bank (Georgia), National Association. PNC paid

$3.6 billion in cash as the consideration for the acquisition of

both RBC Bank (USA) and the credit card portfolio. The

transaction added approximately $18.1 billion in deposits,

$14.5 billion of loans and $1.1 billion of goodwill and

intangible assets to PNC’s Consolidated Balance Sheet. Our

Consolidated Income Statement includes the impact of

business activity associated with the RBC Bank (USA)

acquisition subsequent to March 2, 2012.

RBC Bank (USA), based in Raleigh, North Carolina, operated

more than 400 branches in North Carolina, Florida, Alabama,

Georgia, Virginia and South Carolina. The primary reasons for

the acquisition of RBC Bank (USA) were to enhance

shareholder value, to improve PNC’s competitive position in

the financial services industry, and to further expand PNC’s

existing branch network in the states where it currently

operates as well as expanding into new markets. When

combined with PNC’s existing network, PNC now has 2,881

branches across 17 states and the District of Columbia,

ranking it fifth among U.S. banks in branches. See Note 2

Acquisition and Divestiture Activity in the Notes To

Consolidated Financial Statements in Item 8 of this Report for

additional information regarding this acquisition and the

Smartstreet divestiture and 2011 branch acquisitions described

below.

S

ALE OF

S

MARTSTREET

Effective October 26, 2012, PNC divested certain deposits and

assets of the Smartstreet business unit, which was acquired by

PNC as part of the RBC Bank (USA) acquisition, to Union

Bank, N.A. Smartstreet is a nationwide business focused on

homeowner or community association managers and had

approximately $1 billion of assets and deposits as of

September 30, 2012. The gain on sale was immaterial and

resulted in a reduction of goodwill and core deposit

intangibles of $46 million and $13 million, respectively.

B

RANCH

A

CQUISITIONS

Effective December 9, 2011, PNC acquired 27 branches in the

northern metropolitan Atlanta, Georgia area from Flagstar

Bank, FSB, a subsidiary of Flagstar Bancorp, Inc. Effective

June 6, 2011, PNC acquired 19 branches in the greater Tampa,

Florida area from BankAtlantic, a subsidiary of BankAtlantic

Bancorp, Inc. Our Consolidated Income Statement includes

the impact of the branch activity subsequent to each date of

the respective acquisitions.

The PNC Financial Services Group, Inc. – Form 10-K 31