PNC Bank 2012 Annual Report Download - page 186

Download and view the complete annual report

Please find page 186 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

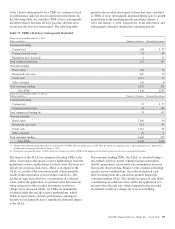

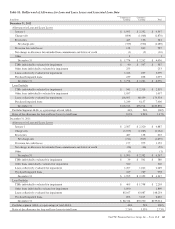

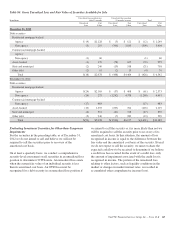

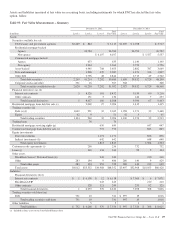

Table 84: Gross Unrealized Loss and Fair Value of Securities Available for Sale

In millions

Unrealized loss position less

than 12 months

Unrealized loss position

12 months or more Total

Unrealized

Loss

Fair

Value

Unrealized

Loss

Fair

Value

Unrealized

Loss

Fair

Value

December 31, 2012

Debt securities

Residential mortgage-backed

Agency $ (9) $1,128 $ (3) $ 121 $ (12) $ 1,249

Non-agency (3) 219 (306) 3,185 (309) 3,404

Commercial mortgage-backed

Agency

Non-agency (1) 60 (1) 60

Asset-backed (1) 370 (78) 625 (79) 995

State and municipal (2) 240 (19) 518 (21) 758

Other debt (2) 61 (2) 15 (4) 76

Total $(18) $2,078 $ (408) $4,464 $ (426) $ 6,542

December 31, 2011

Debt securities

Residential mortgage-backed

Agency $(24) $2,165 $ (37) $ 408 $ (61) $ 2,573

Non-agency (26) 273 (1,242) 4,378 (1,268) 4,651

Commercial mortgage-backed

Non-agency (17) 483 (17) 483

Asset-backed (13) 1,355 (203) 764 (216) 2,119

State and municipal (6) 512 (41) 318 (47) 830

Other debt (5) 240 (7) 289 (12) 529

Total $(91) $5,028 $(1,530) $6,157 $(1,621) $11,185

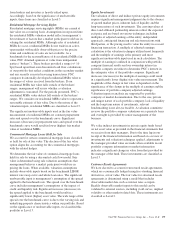

Evaluating Investment Securities for Other-than-Temporary

Impairments

For the securities in the preceding table, as of December 31,

2012 we do not intend to sell and believe we will not be

required to sell the securities prior to recovery of the

amortized cost basis.

On at least a quarterly basis, we conduct a comprehensive

security-level assessment on all securities in an unrealized loss

position to determine if OTTI exists. An unrealized loss exists

when the current fair value of an individual security is less

than its amortized cost basis. An OTTI loss must be

recognized for a debt security in an unrealized loss position if

we intend to sell the security or it is more likely than not we

will be required to sell the security prior to recovery of its

amortized cost basis. In this situation, the amount of loss

recognized in income is equal to the difference between the

fair value and the amortized cost basis of the security. Even if

we do not expect to sell the security, we must evaluate the

expected cash flows to be received to determine if we believe

a credit loss has occurred. In the event of a credit loss, only

the amount of impairment associated with the credit loss is

recognized in income. The portion of the unrealized loss

relating to other factors, such as liquidity conditions in the

market or changes in market interest rates, is recorded in

accumulated other comprehensive income (loss).

The PNC Financial Services Group, Inc. – Form 10-K 167