PNC Bank 2012 Annual Report Download - page 205

Download and view the complete annual report

Please find page 205 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

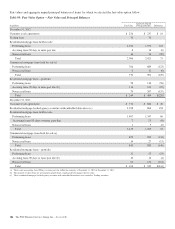

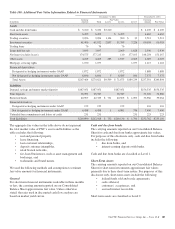

|

|

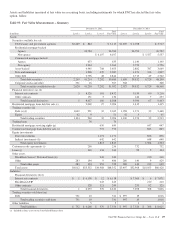

Securities

Securities include both the investment securities (comprised of

available for sale and held to maturity securities) and trading

securities portfolios. We primarily use prices obtained from

pricing services, dealer quotes or recent trades to determine

the fair value of securities. As of December 31, 2012, 86% of

the positions in these portfolios were priced by pricing

services provided by third-party vendors. The third-party

vendors use a variety of methods when pricing securities that

incorporate relevant market data to arrive at an estimate of

what a buyer in the marketplace would pay for a security

under current market conditions. One of the vendor’s prices is

set with reference to market activity for highly liquid assets,

such as U.S. Treasury and agency securities and agency

mortgage-backed securities, and matrix pricing for other asset

classes, such as commercial mortgage and other asset-backed

securities. Another vendor primarily uses pricing models

considering adjustments for ratings, spreads, matrix pricing

and prepayments for the instruments we value using this

service, such as non-agency residential mortgage-backed

securities, agency adjustable rate mortgage securities, agency

CMOs, commercial mortgage-backed securities, and

municipal bonds. Management uses various methods and

techniques to validate prices obtained from pricing services

and dealers, including reference to another third-party source,

by reviewing valuations of comparable instruments, or by

comparison to internal valuations.

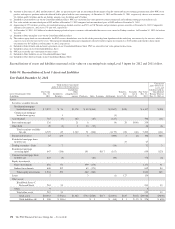

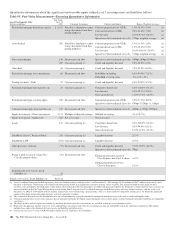

Net Loans And Loans Held For Sale

Fair values are estimated based on the discounted value of

expected net cash flows incorporating assumptions about

prepayment rates, net credit losses and servicing fees. For

purchased impaired loans, fair value is assumed to equal

PNC’s carrying value, which represents the present value of

expected future principal and interest cash flows, as adjusted

for any ALLL recorded for these loans. See Note 6 Purchased

Loans for additional information. For revolving home equity

loans and commercial credit lines, this fair value does not

include any amount for new loans or the related fees that will

be generated from the existing customer relationships.

Nonaccrual loans are valued at their estimated recovery value.

Also refer to the Fair Value Measurement and Fair Value

Option sections of this Note 9 regarding the fair value of

commercial and residential mortgage loans held for sale.

Loans are presented net of the ALLL and do not include future

accretable discounts related to purchased impaired loans.

Other Assets

Other assets as shown in the preceding table includes the

following:

• FHLB and FRB stock,

• equity investments carried at cost and fair value, and

• BlackRock Series C Preferred Stock.

Investments accounted for under the equity method, including

our investment in BlackRock, are not included in the

preceding Table 100: Additional Fair Value Information

Related to Financial Instruments.

Refer to the Fair Value Measurement section of this Note 9

regarding the fair value of equity investments.

The aggregate carrying value of our investments that are

carried at cost and FHLB and FRB stock was $1.7 billion at

December 31, 2012 and was $1.9 billion at December 31,

2011, which approximates fair value at each date.

Mortgage Servicing Assets

Fair value is based on the present value of the estimated future

cash flows, incorporating assumptions as to prepayment rates,

discount rates, default rates, escrow balances, interest rates,

cost to service and other factors.

The key valuation assumptions for commercial and residential

mortgage loan servicing assets at December 31, 2012 and

December 31, 2011 are included in Note 10 Goodwill and

Other Intangible Assets.

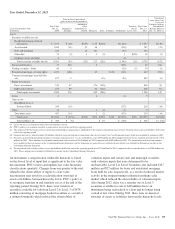

Customer Resale Agreements

Refer to the Fair Value Measurement section of this Note 9

regarding the fair value of customer resale agreements.

Deposits

The carrying amounts of noninterest-bearing and interest-

bearing demand, interest-bearing money market and savings

deposits approximate fair values. For time deposits, which

include foreign deposits, fair values are estimated based on the

discounted value of expected net cash flows assuming current

interest rates. All deposits are classified as Level 2.

Borrowed Funds

The carrying amounts of Federal funds purchased, commercial

paper, repurchase agreements, trading securities sold short,

cash collateral, other short-term borrowings, acceptances

outstanding and accrued interest payable are considered to be

their fair value because of their short-term nature. For all other

borrowed funds, fair values are estimated using either prices

obtained from third-party vendors or an internally developed

discounted cash flow approach taking into consideration our

current incremental borrowing rates for similar instruments.

Unfunded Loan Commitments And Letters of Credit

The fair value of unfunded loan commitments and letters of

credit is determined from a market participant’s view

including the impact of changes in interest rates, credit and

other factors. Because our obligation on substantially all

unfunded loan commitments and letters of credit varies with

changes in interest rates, these instruments are subject to little

fluctuation in fair value due to changes in interest rates. We

establish a liability on these facilities related to the

creditworthiness of our counterparty. These instruments are

classified as Level 3.

F

INANCIAL

D

ERIVATIVES

Refer to the Fair Value Measurement section of this Note 9

regarding the fair value of financial derivatives.

186 The PNC Financial Services Group, Inc. – Form 10-K