Citibank 2014 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

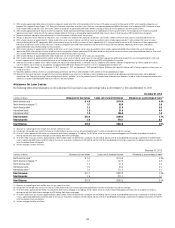

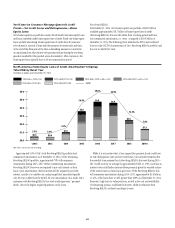

82

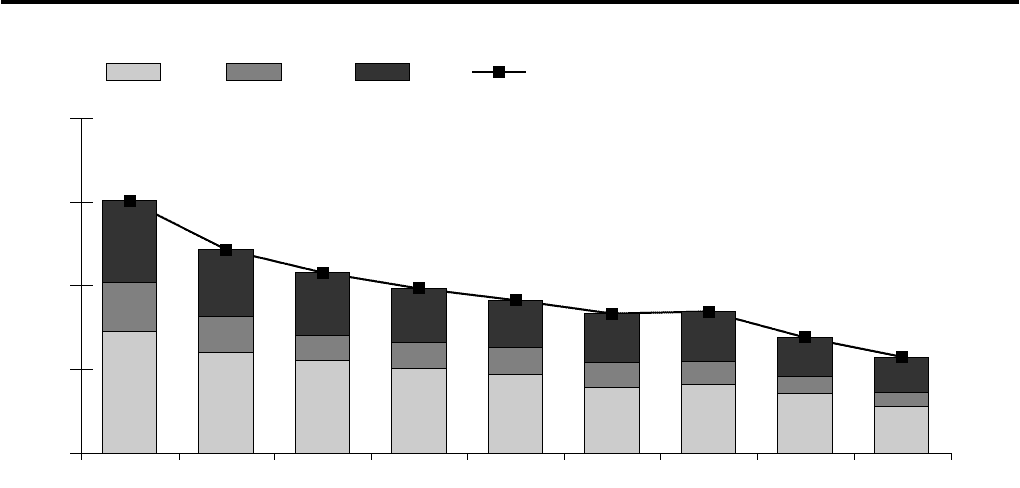

North America Residential First Mortgage Delinquencies—Citi Holdings

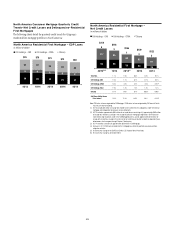

In billions of dollars

Days Past Due:

0

2

4

8

6

30+ DPD

180+

90-179

30-89

4Q’143Q’142Q’141Q’144Q’133Q’132Q’131Q’134Q’12

2.91 2.41 2.21 2.02 1.88 1.58 1.64 1.43 1.12

1.17

0.85 0.61 0.63 0.64 0.59 0.55 0.41 0.34

1.95

1.61 1.50 1.30 1.13 1.18 1.20

0.84

0.94

6.03

4.87

4.32 3.94 3.66 3.34 3.39

2.77 2.31

Note: Days past due excludes (i) U.S. mortgage loans that are guaranteed by U.S. government-sponsored agencies because the potential loss predominantly resides with the U.S. agencies, and (ii) loans recorded at fair value.

Totals may not sum due to rounding.

Credit performance (net credit losses and delinquencies) of the residential

first mortgage portfolio continued to improve during 2014, although the

home price index (HPI), which varies from market to market (as indicated

in the table below), moderated throughout 2014 compared to the prior

year. The decline in net credit losses during 2014 was driven by continued

improvement in credit, HPI, the economic environment and continued

management actions, primarily asset sales and loans transferred to held-

for-sale and, to a lesser extent, loan modifications. CitiFinancial’s net credit

losses improved more modestly in 2014 compared to CitiMortgage, including

an increase in net credit losses in the fourth quarter of 2014 due to portfolio

seasoning and loss mitigation activities.

Residential first mortgages originated by CitiFinancial have a higher

net credit loss rate (4.6%, compared to 0.4% for CitiMortgage as of the

fourth quarter of 2014), as CitiFinancial borrowers tend to have higher LTVs

and lower FICOs than CitiMortgage borrowers. CitiFinancial’s residential

first mortgages also have a significantly different geographic distribution,

with different mortgage market conditions that tend to lag the overall

improvements in HPI.

During 2014, continued management actions, primarily assets sales and

loans transferred to held-for-sale and, to a lesser extent, loan modifications,

were the primary drivers of the overall improvement in delinquencies in Citi

Holdings’ residential first mortgage portfolio. Citi sold or transferred to held-

for-sale approximately $1.2 billion of delinquent residential first mortgages

in 2014 (compared to $2.1 billion in 2013), including $0.6 billion during

the fourth quarter of 2014. Credit performance from quarter to quarter could

continue to be impacted by the volume of delinquent loan sales (or lack of

significant sales) and HPI, as well as increases in interest rates.