Citibank 2014 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

102

Price Risk

Price risk losses arise from fluctuations in the market value of non-trading

and trading positions resulting from changes in interest rates, credit

spreads, foreign exchange rates, equity and commodity prices, and in their

implied volatilities.

Price Risk Measurement and Stress Testing

Price risks are measured in accordance with established standards to

ensure consistency across businesses and the ability to aggregate risk. The

measurements used for non-trading and trading portfolios, as well as

associated stress testing processes, are described below.

Price Risk—Non-Trading Portfolios

Net Interest Revenue and Interest Rate Risk

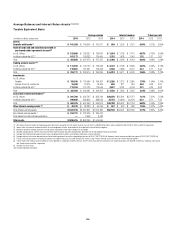

Net interest revenue, for interest rate exposure purposes, is the difference

between the yield earned on the non-trading portfolio assets (including

customer loans) and the rate paid on the liabilities (including customer

deposits or company borrowings). Net interest revenue is affected by changes

in the level of interest rates, as well as the amounts of assets and liabilities,

and the timing of repricing of assets and liabilities to reflect market rates.

Interest Rate Risk Measurement—IRE

Citi’s principal measure of risk to net interest revenue is interest rate

exposure (IRE). IRE measures the change in expected net interest revenue

in each currency resulting solely from unanticipated changes in forward

interest rates.

Citi’s estimated IRE incorporates various assumptions including

prepayment rates on loans, customer behavior, and the impact of pricing

decisions. For example, in rising interest rate scenarios, portions of the

deposit portfolio may be assumed to experience rate increases that are less

than the change in market interest rates. In declining interest rate scenarios,

it is assumed that mortgage portfolios experience higher prepayment rates.

IRE assumes that businesses and/or Citi Treasury make no additional

changes in balances or positioning in response to the unanticipated

rate changes.

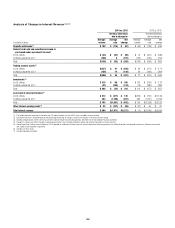

Mitigation and Hedging of Interest Rate Risk

In order to manage changes in interest rates effectively, Citi may modify

pricing on new customer loans and deposits, purchase fixed rate securities,

issue debt that is either fixed or floating or enter into derivative transactions

that have the opposite risk exposures. Citi regularly assesses the viability of

these and other strategies to reduce its interest rate risks and implements

such strategies when it believes those actions are prudent.

Citi manages interest rate risk as a consolidated company-wide position.

Citi’s client-facing businesses create interest rate sensitive positions,

including loans and deposits, as part of their ongoing activities. Citi Treasury

aggregates these risk positions and manages them centrally. Operating within

established limits, Citi Treasury makes positioning decisions and uses tools,

such as Citi’s investment securities portfolio, company-issued debt, and

interest rate derivatives, to target the desired risk profile. Changes in Citi’s

interest rate risk position reflect the accumulated changes in all non-trading

assets and liabilities, with potentially large and offsetting impacts, as well as

Citi Treasury’s positioning decisions.

Stress Testing

Citigroup employs additional measurements, including stress testing the

impact of non-linear interest rate movements on the value of the balance

sheet; the analysis of portfolio duration and volatility, particularly as they

relate to mortgage loans and mortgage-backed securities; and the potential

impact of the change in the spread between different market indices.

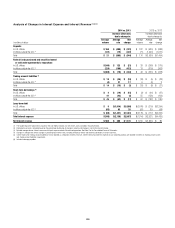

Interest Rate Risk Measurement—OCI at Risk

Citi also measures the potential impacts of changes in interest rates on the

value of its Other Comprehensive Income (OCI), which can in turn impact

Citi’s Common Equity Tier 1 Capital ratio. Citi’s goal is to benefit from an

increase in the market level of interest rates, while limiting the impact of

changes in OCI on its regulatory capital position.

OCI at risk is managed as part of the company-wide interest rate

risk position. OCI at risk considers potential changes in OCI (and the

corresponding impact on the Common Equity Tier 1 Capital ratio) relative to

Citi’s capital generation capacity.