Citibank 2014 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

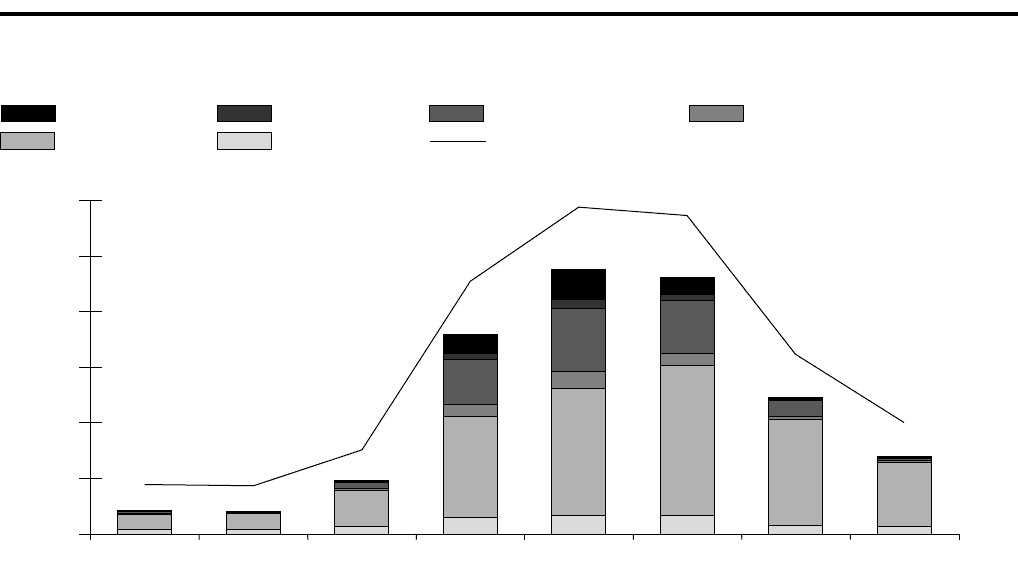

84

North America Consumer Mortgage Quarterly Credit

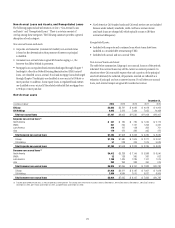

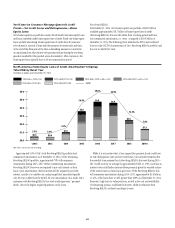

Trends—Net Credit Losses and Delinquencies—Home

Equity Loans

Citi’s home equity loan portfolio consists of both fixed-rate home equity loans

and loans extended under home equity lines of credit. Fixed-rate home equity

loans are fully amortizing. Home equity lines of credit allow for amounts

to be drawn for a period of time with the payment of interest only and then,

at the end of the draw period, the then-outstanding amount is converted to

an amortizing loan (the interest-only payment feature during the revolving

period is standard for this product across the industry). After conversion, the

home equity loans typically have a 20-year amortization period.

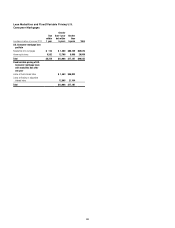

Revolving HELOCs

At December 31, 2014, Citi’s home equity loan portfolio of $28.1 billion

included approximately $16.7 billion of home equity lines of credit

(Revolving HELOCs) that are still within their revolving period and have

not commenced amortization, or “reset,” compared to $18.9 billion at

December 31, 2013. The following chart indicates the FICO and combined

loan-to-value (CLTV) characteristics of Citi’s Revolving HELOCs portfolio and

the year in which they reset:

FICO 660+,CLTV>100 FICO<660,CLTV>100 FICO 660+,CLTV>=80<=100 FICO<660,CLTV>=80<=100

FICO 660+,CLTV<80 FICO<660,CLTV<80 %ENR

$6.0

$5.0

$4.0

$3.0

$2.0

$1.0

$0.0

2019+201820172016201520142013<2013

$0.4

2.3%

$0.4

2.2% $1.0

5.3%

$3.6

19.4% $4.8

25.6%

$4.6

24.9%

$2.5

13.3%

$1.3

7.0%

North America Home Equity Lines of Credit Amortization—Citigroup

Total ENR by Reset Year

In billions of dollars as of December 31, 2014

Note: Totals may not sum due to rounding.

Approximately 10% of Citi’s total Revolving HELOCs portfolio had

commenced amortization as of December 31, 2014. Of the remaining

Revolving HELOCs portfolio, approximately 78% will commence

amortization during 2015–2017. Before commencing amortization,

Revolving HELOC borrowers are required to pay only interest on their

loans. Upon amortization, these borrowers will be required to pay both

interest, usually at a variable rate, and principal that amortizes typically

over 20 years, rather than the typical 30-year amortization. As a result, Citi’s

customers with Revolving HELOCs that reset could experience “payment

shock” due to the higher required payments on the loans.

While it is not certain what, if any, impact this payment shock could have

on Citi’s delinquency rates and net credit losses, Citi currently estimates that

the monthly loan payment for its Revolving HELOCs that reset during 2015–

2017 could increase on average by approximately $360, or 170%. Increases in

interest rates could further increase these payments given the variable nature

of the interest rates on these loans post-reset. Of the Revolving HELOCs that

will commence amortization during 2015–2017, approximately $1.6 billion,

or 12%, of the loans have a CLTV greater than 100% as of December 31, 2014.

Borrowers’ high loan-to-value positions, as well as the cost and availability

of refinancing options, could limit borrowers’ ability to refinance their

Revolving HELOCs as these loans begin to reset.