Citibank 2014 Annual Report Download - page 263

Download and view the complete annual report

Please find page 263 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

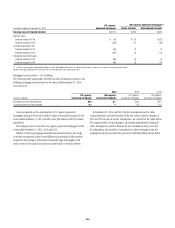

246

Exposure to credit risk on derivatives is affected by market volatility,

which may impair the ability of counterparties to satisfy their obligations

to the Company. Credit limits are established and closely monitored for

customers engaged in derivatives transactions. Citi considers the level of

legal certainty regarding enforceability of its offsetting rights under master

netting agreements and credit support annexes to be an important factor in

its risk management process. Specifically, Citi generally transacts much lower

volumes of derivatives under master netting agreements where Citi does not

have the requisite level of legal certainty regarding enforceability, because

such derivatives consume greater amounts of single counterparty credit

limits than those executed under enforceable master netting agreements.

Cash collateral and security collateral in the form of G10 government

debt securities is often posted by a party to a master netting agreement to

secure the net open exposure of the other party; the receiving party is free

to commingle/rehypothecate such collateral in the ordinary course of its

business. Nonstandard collateral such as corporate bonds, municipal bonds,

U.S. agency securities and/or MBS may also be pledged as collateral for

derivative transactions. Security collateral posted to open and maintain a

master netting agreement with a counterparty, in the form of cash and/or

securities, may from time to time be segregated in an account at a third-party

custodian pursuant to a tri-party account control agreement.

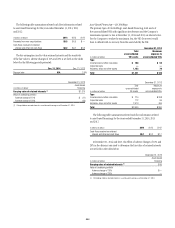

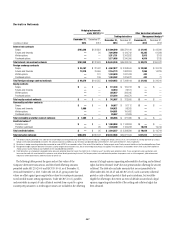

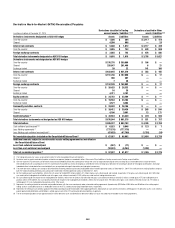

Information pertaining to Citigroup’s derivative activity, based on notional

amounts, as of December 31, 2014 and December 31, 2013, is presented in

the table below. Derivative notional amounts are reference amounts from

which contractual payments are derived and, in Citigroup’s view, do not

accurately represent a measure of Citi’s exposure to derivative transactions.

Rather, as discussed above, Citi’s derivative exposure arises primarily from

market fluctuations (i.e., market risk), counterparty failure (i.e., credit

risk) and/or periods of high volatility or financial stress (i.e., liquidity

risk), as well as any market valuation adjustments that may be required on

the transactions. Moreover, notional amounts do not reflect the netting of

offsetting trades (also as discussed above). For example, if Citi enters into an

interest rate swap with $100 million notional, and offsets this risk with an

identical but opposite position with a different counterparty, $200 million in

derivative notionals is reported, although these offsetting positions may result

in de minimus overall market risk. Aggregate derivative notional amounts

can fluctuate from period-to-period in the normal course of business based

on Citi’s market share as well as levels of client activity.