Citibank 2014 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

86

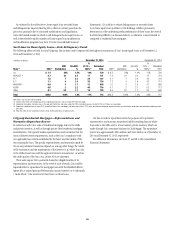

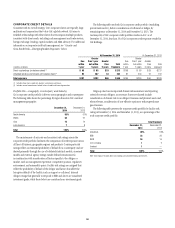

As evidenced by the tables above, home equity loan net credit losses

and delinquencies improved during 2014, albeit at a slower pace than the

prior year, primarily due to continued modifications and liquidations.

Given the limited market in which to sell delinquent home equity loans, as

well as the relatively smaller number of home equity loan modifications

and modification programs (see Note 15 to the Consolidated Financial

Statements), Citi’s ability to reduce delinquencies or net credit losses

in its home equity loan portfolio in Citi Holdings, whether pursuant to

deterioration of the underlying credit performance of these loans, the reset of

the Revolving HELOCs (as discussed above) or otherwise, is more limited as

compared to residential first mortgages.

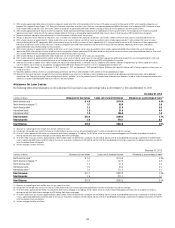

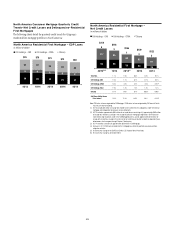

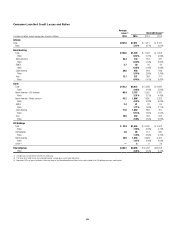

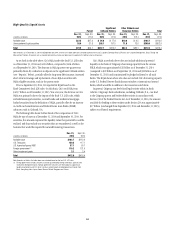

North America Home Equity Loans—State Delinquency Trends

The following tables set forth, for total Citigroup, the six states and/or regions with the highest concentration of Citi’s home equity loans as of December 31,

2014 and December 31, 2013.

In billions of dollars December 31, 2014 December 31, 2013

State (1) ENR (2)

ENR

Distribution

90+DPD

%

%

CLTV >

100% (3)

Refreshed

FICO ENR (2)

ENR

Distribution

90+DPD

%

%

CLTV >

100% (3)

Refreshed

FICO

CA $ 7.4 28% 1.5% 10% 729 $ 8.2 28% 1.6% 17% 726

NY/NJ/CT (4) 6.7 25 2.4 11 721 7.2 24 2.3 12 718

FL (4) 1.8 7 2.2 36 707 2.1 7 2.9 44 704

IL (4) 1.1 4 1.4 35 716 1.2 4 1.6 42 713

IN/OH/MI (4) 0.8 3 1.7 31 688 1.0 3 1.6 47 686

AZ/NV 0.6 2 2.2 46 716 0.7 2 2.1 53 713

Other 8.1 30 1.7 19 703 9.5 32 1.7 26 699

Total $26.6 100% 1.8% 17% 715 $29.9 100% 1.9% 23% 712

Note: Totals may not sum due to rounding.

(1) Certain of the states are included as part of a region based on Citi’s view of similar HPI within the region.

(2) Ending net receivables. Excludes loans in Canada and Puerto Rico and loans subject to LTSCs. Excludes balances for which FICO or LTV data are unavailable.

(3) Represents combined loan-to-value (CLTV) for both residential first mortgages and home equity loans. CLTV ratios (loan balance divided by appraised value) are calculated at origination and updated by applying market

price data.

(4) New York, New Jersey, Connecticut, Indiana, Ohio, Florida and Illinois are judicial states.

Citigroup Residential Mortgages—Representations and

Warranties Repurchase Reserve

In connection with Citi’s sales of residential mortgage loans to the GSEs

and private investors, as well as through private-label residential mortgage

securitizations, Citi typically makes representations and warranties that the

loans sold meet certain requirements, such as the loan’s compliance with

any applicable loan criteria established by the buyer and the validity of the

lien securing the loan. The specific representations and warranties made by

Citi in any particular transaction depend on, among other things, the nature

of the transaction and the requirements of the investor (e.g., whole loan sale

to the GSEs versus loans sold through securitization transactions), as well as

the credit quality of the loan (e.g., prime, Alt-A or subprime).

These sales expose Citi to potential claims for alleged breaches of its

representations and warranties. In the event of such a breach, Citi could be

required either to repurchase the mortgage loans with the identified defects

(generally at unpaid principal balance plus accrued interest) or to indemnify

(“make whole”) the investors for their losses on these loans.

Citi has recorded a repurchase reserve for purposes of its potential

representation and warranty repurchase liability resulting from its whole

loan sales to the GSEs and, to a lesser extent, private investors, which are

made through Citi’s consumer business in CitiMortgage. The repurchase

reserve was approximately $224 million and $341 million as of December 31,

2014 and December 31, 2013, respectively.

For additional information, see Notes 27 and 28 to the Consolidated

Financial Statements.