Citibank 2014 Annual Report Download - page 204

Download and view the complete annual report

Please find page 204 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

187

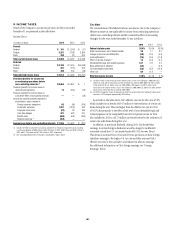

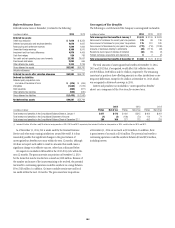

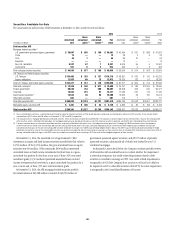

11. FEDERAL FUNDS, SECURITIES BORROWED,

LOANED AND SUBJECT TO REPURCHASE AGREEMENTS

Federal funds sold and securities borrowed or purchased under

agreements to resell, at their respective carrying values, consisted of the

following at December 31:

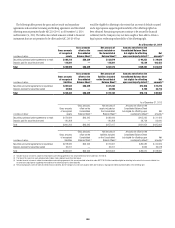

In millions of dollars 2014 2013

Federal funds sold $ — $ 20

Securities purchased under agreements to resell 123,979 136,649

Deposits paid for securities borrowed 118,591 120,368

Total $242,570 $257,037

Federal funds purchased and securities loaned or sold under

agreements to repurchase, at their respective carrying values, consisted of

the following at December 31:

In millions of dollars 2014 2013

Federal funds purchased $ 334 $ 910

Securities sold under agreements to repurchase 147,204 175,691

Deposits received for securities loaned 25,900 26,911

Total $173,438 $203,512

The resale and repurchase agreements represent collateralized financing

transactions. The Company executes these transactions primarily through its

broker-dealer subsidiaries to facilitate customer matched-book activity and

to efficiently fund a portion of the Company’s trading inventory. Transactions

executed by the Company’s bank subsidiaries primarily facilitate customer

financing activity.

It is the Company’s policy to take possession of the underlying collateral,

monitor its market value relative to the amounts due under the agreements

and, when necessary, require prompt transfer of additional collateral in order

to maintain contractual margin protection. Collateral typically consists of

government and government-agency securities, corporate and municipal

bonds, equities, and mortgage-backed and other asset-backed securities.

The resale and repurchase agreements are generally documented

under industry standard agreements that allow the prompt close-out of all

transactions (including the liquidation of securities held) and the offsetting

of obligations to return cash or securities by the non-defaulting party,

following a payment default or other type of default under the relevant

master agreement. Events of default generally include (i) failure to deliver

cash or securities as required under the transaction, (ii) failure to provide

or return cash or securities as used for margining purposes, (iii) breach

of representation, (iv) cross-default to another transaction entered into

among the parties, or, in some cases, their affiliates, and (v) a repudiation

of obligations under the agreement. The counterparty that receives the

securities in these transactions is generally unrestricted in its use of the

securities, with the exception of transactions executed on a tri-party basis,

where the collateral is maintained by a custodian and operational limitations

may restrict its use of the securities.

A substantial portion of the resale and repurchase agreements is

recorded at fair value, as described in Note 25 to the Consolidated Financial

Statements. The remaining portion is carried at the amount of cash

initially advanced or received, plus accrued interest, as specified in the

respective agreements.

The securities borrowing and lending agreements also represent

collateralized financing transactions similar to the resale and repurchase

agreements. Collateral typically consists of government and government-

agency securities and corporate debt and equity securities.

Similar to the resale and repurchase agreements, securities borrowing

and lending agreements are generally documented under industry standard

agreements that allow the prompt close-out of all transactions (including

the liquidation of securities held) and the offsetting of obligations to return

cash or securities by the non-defaulting party, following a payment default

or other default by the other party under the relevant master agreement.

Events of default and rights to use securities under the securities borrowing

and lending agreements are similar to the resale and repurchase agreements

referenced above.

A substantial portion of securities borrowing and lending agreements is

recorded at the amount of cash advanced or received. The remaining portion

is recorded at fair value as the Company elected the fair value option for

certain securities borrowed and loaned portfolios, as described in Note 26

to the Consolidated Financial Statements. With respect to securities loaned,

the Company receives cash collateral in an amount generally in excess

of the market value of the securities loaned. The Company monitors the

market value of securities borrowed and securities loaned on a daily basis

and obtains or posts additional collateral in order to maintain contractual

margin protection.

The enforceability of offsetting rights incorporated in the master netting

agreements for resale and repurchase agreements and securities borrowing

and lending agreements is evidenced to the extent that a supportive legal

opinion has been obtained from counsel of recognized standing that

provides the requisite level of certainty regarding the enforceability of these

agreements, and that the exercise of rights by the non-defaulting party to

terminate and close-out transactions on a net basis under these agreements

will not be stayed or avoided under applicable law upon an event of default

including bankruptcy, insolvency or similar proceeding.

A legal opinion may not have been sought or obtained for certain

jurisdictions where local law is silent or sufficiently ambiguous to determine

the enforceability of offsetting rights or where adverse case law or conflicting

regulation may cast doubt on the enforceability of such rights. In some

jurisdictions and for some counterparty types, the insolvency law for a

particular counterparty type may be nonexistent or unclear as overlapping

regimes may exist. For example, this may be the case for certain sovereigns,

municipalities, central banks and U.S. pension plans.