Citibank 2014 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

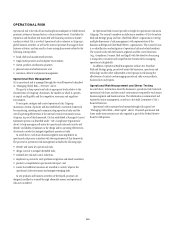

124

SIGNIFICANT ACCOUNTING POLICIES AND SIGNIFICANT ESTIMATES

Note 1 to the Consolidated Financial Statements contains a summary of

Citigroup’s significant accounting policies, including a discussion of recently

issued accounting pronouncements. These policies, as well as estimates made

by management, are integral to the presentation of Citi’s results of operations

and financial condition. While all of these policies require a certain level of

management judgment and estimates, this section highlights and discusses

the significant accounting policies that require management to make highly

difficult, complex or subjective judgments and estimates at times regarding

matters that are inherently uncertain and susceptible to change (see also

“Risk Factors—Business and Operational Risks” above). Management has

discussed each of these significant accounting policies, the related estimates,

and its judgments with the Audit Committee of the Citigroup Board of

Directors. Additional information about these policies can be found in Note 1

to the Consolidated Financial Statements.

Valuations of Financial Instruments

Citigroup holds debt and equity securities, derivatives, retained interests

in securitizations, investments in private equity and other financial

instruments. Substantially all of these assets and liabilities are reflected at

fair value on Citi’s Consolidated Balance Sheet.

Citi purchases securities under agreements to resell (reverse repos) and

sells securities under agreements to repurchase (repos), a majority of which

are carried at fair value. In addition, certain loans, short-term borrowings,

long-term debt and deposits, as well as certain securities borrowed and

loaned positions that are collateralized with cash, are carried at fair value.

Citigroup holds its investments, trading assets and liabilities, and resale

and repurchase agreements on the Consolidated Balance Sheet to meet

customer needs and to manage liquidity needs, interest rate risks and private

equity investing.

When available, Citi generally uses quoted market prices to determine

fair value and classifies such items within Level 1 of the fair value hierarchy

established under ASC 820-10, Fair Value Measurement. If quoted market

prices are not available, fair value is based upon internally developed

valuation models that use, where possible, current market-based or

independently sourced market parameters, such as interest rates, currency

rates and option volatilities. Such models are often based on a discounted

cash flow analysis. In addition, items valued using such internally generated

valuation techniques are classified according to the lowest level input or

value driver that is significant to the valuation. Thus, an item may be

classified under the fair value hierarchy as Level 3 even though there may be

some significant inputs that are readily observable.

The credit crisis caused some markets to become illiquid, thus reducing

the availability of certain observable data used by Citi’s valuation techniques.

This illiquidity, in at least certain markets, continued through 2014. When

or if liquidity returns to these markets, the valuations will revert to using the

related observable inputs in verifying internally calculated values.

Citi is required to exercise subjective judgments relating to the

applicability and functionality of internal valuation models, the significance

of inputs or value drivers to the valuation of an instrument, and the degree

of illiquidity and subsequent lack of observability in certain markets.

These judgments have the potential to impact the Company’s financial

performance for instruments where the changes in fair value are recognized

in either the Consolidated Statement of Income or in Accumulated other

comprehensive income (loss) (AOCI).

Moreover, for certain investments, decreases in fair value are only

recognized in earnings in the Consolidated Statement of Income if such

decreases are judged to be an other-than-temporary impairment (OTTI).

Adjudicating the temporary nature of fair value impairments is also

inherently judgmental.

The fair value of financial instruments incorporates the effects of

Citi’s own credit risk and the market view of counterparty credit risk, the

quantification of which is also complex and judgmental. For additional

information on Citi’s fair value analysis, see Notes 1, 6, 25 and 26 to the

Consolidated Financial Statements.

Allowance for Credit Losses

Management provides reserves for an estimate of probable losses inherent in

the funded loan portfolio and in unfunded loan commitments and standby

letters of credit on the Consolidated Balance Sheet in the Allowance for loan

losses and in Other liabilities, respectively.

Estimates of these probable losses are based upon (i) Citigroup’s internal

system of credit-risk ratings, which are analogous to the risk ratings of

the major credit rating agencies; and (ii) historical default and loss data,

including rating agency information regarding default rates from 1983

to 2013, and internal data dating to the early 1970s on severity of losses

in the event of default. Adjustments may be made to this data, including

(i) statistically calculated estimates to cover the historical fluctuation

of the default rates over the credit cycle, the historical variability of loss

severity among defaulted loans, and the degree to which there are large

obligor concentrations in the global portfolio; and (ii) adjustments made

for specifically known items, such as current environmental factors and

credit trends.

In addition, representatives from both the risk management and finance

staffs who cover business areas with delinquency-managed portfolios

containing smaller homogeneous loans present their recommended reserve

balances based upon leading credit indicators, including loan delinquencies

and changes in portfolio size, as well as economic trends, including housing

prices, unemployment and GDP. This methodology is applied separately

for each individual product within each geographic region in which these

portfolios exist.

This evaluation process is subject to numerous estimates and judgments.

The frequency of default, risk ratings, loss recovery rates, the size and

diversity of individual large credits, and the ability of borrowers with foreign

currency obligations to obtain the foreign currency necessary for orderly debt

servicing, among other things, are all taken into account during this review.

Changes in these estimates could have a direct impact on Citi’s credit costs

and the allowance in any period.

For a further description of the loan loss reserve and related accounts, see

Notes 1 and 16 to the Consolidated Financial Statements.