Citibank 2014 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

100

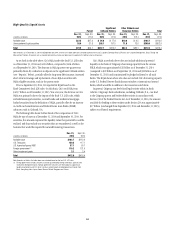

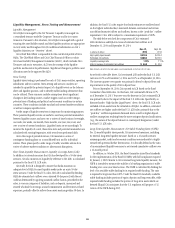

Credit Ratings

Citigroup’s funding and liquidity, its funding capacity, ability to access

capital markets and other sources of funds, the cost of these funds, and its

ability to maintain certain deposits are partially dependent on its credit

ratings. The table below sets forth the ratings for Citigroup and Citibank, N.A.

as of December 31, 2014. While not included in the table below, Citigroup

Global Markets Inc. (CGMI) is rated A/A-1 by Standard & Poor’s and A/F1 by

Fitch as of December 31, 2014.

Debt Ratings as of December 31, 2014

Citigroup Inc. Citibank, N.A.

Senior

debt

Commercial

paper Outlook

Long-

term

Short-

term Outlook

Fitch Ratings (Fitch) A F1 Stable A F1 Stable

Moody’s Investors Service (Moody’s) Baa2 P-2 Stable A2 P-1 Stable

Standard & Poor’s (S&P) A- A-2 Negative A A-1 Stable

Recent Credit Rating Developments

On December 17, 2014, Fitch issued a bank “criteria exposure draft.” The

document consolidates all bank rating criteria into one report and refines

certain aspects of the criteria, including clarification as to when the agency

might rate an operating company’s long-term rating above its unsupported

rating due to the protection offered to senior creditors by loss absorbing

junior instruments. Since March 2014, Fitch has been contemplating the

introduction of a ratings differential between U.S. bank holding companies

and operating companies due to the evolving regulatory landscape.

Currently, Fitch equalizes holding company and operating company ratings,

reflecting what it views as the close correlation between default probabilities.

On November 24, 2014, S&P issued a proposal to add a component to its

bank rating methodology to address how a bank’s long-term rating may be

higher than the bank’s unsupported rating due to “additional loss absorbing

capacity” (ALAC). The ALAC proposal considers that loss absorption by

instruments subject to bail-in could partly or fully replace a government

bail-out and could reduce the likelihood of default on an operating

company’s senior unsecured debt obligations. S&P continues to evaluate

government support into the ratings of systemically important U.S. bank

holding companies.

On September 9, 2014, Moody’s also released for comment a new bank

rating methodology. The new methodology proposed a streamlined baseline

credit assessment (with removal of the bank financial strength rating) and

introduced a “loss given failure” assessment into the ratings. The comment

period has closed and resolution is expected in early 2015.

Potential Impacts of Ratings Downgrades

Ratings downgrades by Moody’s, Fitch or S&P could negatively impact

Citigroup’s and/or Citibank, N.A.’s funding and liquidity due to reduced

funding capacity, including derivatives triggers, which could take the form of

cash obligations and collateral requirements.

The following information is provided for the purpose of analyzing the

potential funding and liquidity impact to Citigroup and Citibank, N.A. of

a hypothetical, simultaneous ratings downgrade across all three major

rating agencies. This analysis is subject to certain estimates, estimation

methodologies, and judgments and uncertainties. Uncertainties include

potential ratings limitations that certain entities may have with respect

to permissible counterparties, as well as general subjective counterparty

behavior. For example, certain corporate customers and trading

counterparties could re-evaluate their business relationships with Citi

and limit the trading of certain contracts or market instruments with Citi.

Changes in counterparty behavior could impact Citi’s funding and liquidity,

as well as the results of operations of certain of its businesses. The actual

impact to Citigroup or Citibank, N.A. is unpredictable and may differ

materially from the potential funding and liquidity impacts described below.

For additional information on the impact of credit rating changes on Citi

and its applicable subsidiaries, see “Risk Factors—Liquidity Risks” above.