Citibank 2014 Annual Report Download - page 131

Download and view the complete annual report

Please find page 131 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

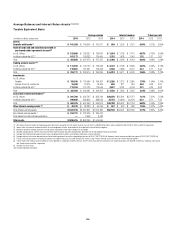

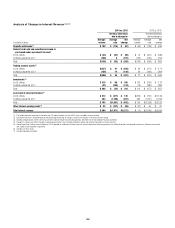

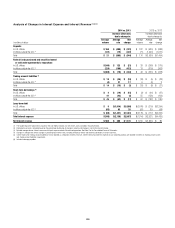

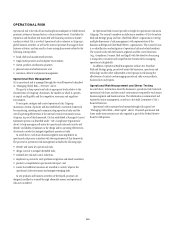

114

Stress Testing

Citi performs stress testing on a regular basis to estimate the impact of

extreme market movements. It is performed on individual positions and

trading portfolios, as well as in aggregate inclusive of multiple trading

portfolios. Citi’s independent market risk management organization, after

consultations with the businesses, develops both systemic and specific stress

scenarios, reviews the output of periodic stress testing exercises, and uses the

information to assess the ongoing appropriateness of exposure levels and

limits. Citi uses two complementary approaches to market risk stress testing

across all major risk factors (i.e., equity, foreign exchange, commodity,

interest rate and credit spreads): top-down systemic stresses and bottom-

up business specific stresses. Systemic stresses are designed to quantify the

potential impact of extreme market movements on a firm-wide basis, and are

constructed using both historical periods of market stress and projections of

adverse economic scenarios. Business specific stresses are designed to probe

the risks of particular portfolios and market segments, especially those risks

that are not fully captured in VAR and systemic stresses.

The systemic stress scenarios and business specific stress scenarios at

Citi are used in several reports reviewed by senior management and also to

calculate internal risk capital for trading market risk. In general, changes in

market factors are defined over a one-year horizon. However, for the purpose

of calculating internal risk capital, changes in a very limited number of

the most liquid market factors are defined over a shorter three-month

horizon. The limited set of market factors subject to the shorter three-month

time horizon are those that in management’s judgment have historically

remained very liquid during financial crises, even as the trading liquidity of

most other market factors materially decreased.

Factor Sensitivities

Factor sensitivities are expressed as the change in the value of a position for

a defined change in a market risk factor, such as a change in the value of a

Treasury bill for a one-basis-point change in interest rates. Citi’s independent

market risk management ensures that factor sensitivities are calculated,

monitored, and in most cases, limited, for all material risks taken in a

trading portfolio.