Citibank 2014 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

112

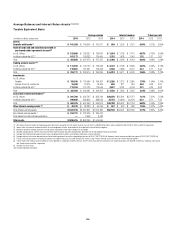

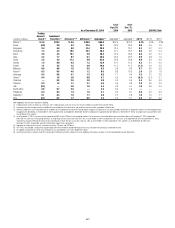

The following table provides the VAR for ICG during 2014, excluding the

CVA relating to derivative counterparties, hedges of CVA, fair value option

loans and hedges to the loan portfolio.

In millions of dollars Dec. 31, 2014

Total—all market risk

factors, including general and specific risk $122

Average—during year $109

High—during year 159

Low—during year 82

VAR Model Review and Validation

Generally, Citi’s VAR review and model validation process entails reviewing

the model framework, major assumptions, and implementation of the

mathematical algorithm. In addition, as part of the model validation

process, product specific back-testing on portfolios is periodically completed

and reviewed with Citi’s U.S. banking regulators. Furthermore, Regulatory

VAR (as described below) back-testing is performed against buy-and-hold

profit and loss on a monthly basis for approximately 167 portfolios across the

organization (trading desk level, ICG business segment and Citigroup) and

the results are shared with the U.S. banking regulators.

Significant VAR model and assumption changes must be independently

validated within Citi’s risk management organization. This validation

process includes a review by Citi’s model validation group and further

approval from its model validation review committee, which is composed

of senior quantitative risk management officers. In the event of significant

model changes, parallel model runs are undertaken prior to implementation.

In addition, significant model and assumption changes are subject to the

periodic reviews and approval by Citi’s U.S. banking regulators.

In the second quarter of 2014, Citi implemented two VAR model

enhancements that were reviewed by Citi’s U.S. banking regulators as well

as Citi’s model validation group. Specifically, Citi enhanced the correlation

among mortgage products as well as introduced industry sectors (financial

and non-financial) into the credit spread component of the VAR model.

Citi uses the same independently validated VAR model for both Regulatory

VAR and Risk Management VAR (i.e., Total Trading and Total Trading and

Credit Portfolios VARs) and, as such, the model review and oversight process

for both purposes is as described above.

Regulatory VAR, which is calculated in accordance with Basel III, differs

from Risk Management VAR due to the fact that certain positions included

in Risk Management VAR are not eligible for market risk treatment in

Regulatory VAR. The composition of Risk Management VAR is discussed

under “Value at Risk” above. The applicability of the VAR model for positions

eligible for market risk treatment under U.S. regulatory capital rules is

periodically reviewed and approved by Citi’s U.S. banking regulators.

In accordance with Basel III, Regulatory VAR includes all trading book

covered positions and all foreign exchange and commodity exposures.

Pursuant to Basel III, Regulatory VAR excludes positions that fail to meet

the intent and ability to trade requirements and are therefore classified as

non-trading book and categories of exposures that are specifically excluded

as covered positions. Regulatory VAR excludes CVA on derivative instruments

and DVA on Citi’s own fair value option liabilities. With the April 2014

implementation of the U.S. final Basel III rules, CVA hedges are excluded

from Regulatory VAR and included in credit risk-weighted assets as computed

under the Advanced Approaches for determining risk-weighted assets.