Citibank 2014 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

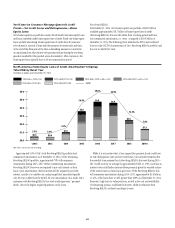

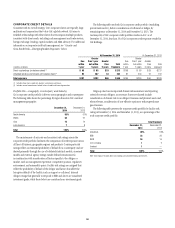

93

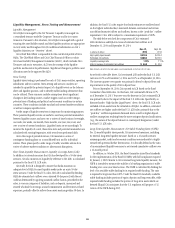

MARKET RISK

Market risk encompasses funding and liquidity risk and price risk, each

of which arises in the normal course of business of a global financial

intermediary such as Citi.

Market Risk Management

Each business is required to establish, with approval from Citi’s market risk

management, a market risk limit framework for identified risk factors that

clearly defines approved risk profiles and is within the parameters of Citi’s

overall risk tolerance. These limits are monitored by independent market

risk, Citi’s country and business Asset and Liability Committees and the

Citigroup Asset and Liability Committee. In all cases, the businesses are

ultimately responsible for the market risks taken and for remaining within

their defined limits.

Funding and Liquidity Risk

Adequate liquidity and sources of funding are essential to Citi’s businesses.

Funding and liquidity risks arise from several factors, many of which Citi

cannot control, such as disruptions in the financial markets, changes in key

funding sources, credit spreads, changes in Citi’s credit ratings and political

and economic conditions in certain countries. For additional information,

see “Risk Factors” above.

Overview

Citi’s funding and liquidity objectives are to maintain adequate liquidity

to (i) fund its existing asset base; (ii) grow its core businesses in Citicorp;

(iii) maintain sufficient liquidity, structured appropriately, so that it can

operate under a wide variety of market conditions, including market

disruptions for both short- and long-term periods; and (iv) satisfy regulatory

requirements. Citigroup’s primary liquidity objectives are established by

entity, and in aggregate, across three major categories:

• the parent entity, which includes the parent holding company (Citigroup)

and Citi’s broker-dealer subsidiaries that are consolidated into Citigroup

(collectively referred to in this section as “parent”);

• Citi’s significant Citibank entities, which consist of Citibank, N.A.

units domiciled in the U.S., Western Europe, Hong Kong, Japan and

Singapore (collectively referred to in this section as “significant Citibank

entities”); and

• other Citibank and Banamex entities.

At an aggregate level, Citigroup’s goal is to maintain sufficient funding

in amount and tenor to fully fund customer assets and to provide an

appropriate amount of cash and high quality liquid assets (as discussed

further below), even in times of stress. The liquidity framework provides that

entities be self-sufficient or net providers of liquidity, including in conditions

established under their designated stress tests.

Citi’s primary sources of funding include (i) deposits via Citi’s bank

subsidiaries, which are Citi’s most stable and lowest cost source of long-

term funding, (ii) long-term debt (primarily senior and subordinated

debt) primarily issued at the parent and certain bank subsidiaries, and

(iii) stockholders’ equity. These sources may be supplemented by short-term

borrowings, primarily in the form of secured funding transactions.

As referenced above, Citigroup works to ensure that the structural tenor of

these funding sources is sufficiently long in relation to the tenor of its asset

base. The goal of Citi’s asset/liability management is to ensure that there is

excess tenor in the liability structure so as to provide excess liquidity after

funding the assets. The excess liquidity resulting from a longer-term tenor

profile can effectively offset potential decreases in liquidity that may occur

under stress. This excess funding is held in the form of high-quality liquid

assets (HQLA), as set forth in the table below.