Citibank 2014 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

7

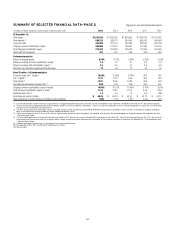

Expenses

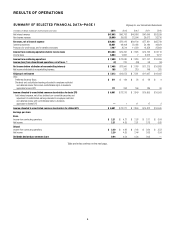

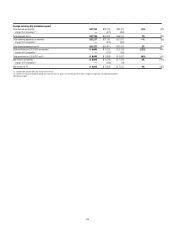

Citigroup expenses increased 14% versus 2013 to $55.1 billion. Excluding

the impact of the mortgage settlement in 2014 and the net fraud loss in

2013, operating expenses increased 7% versus the prior year to $51.3 billion

driven by higher legal and related expenses ($5.8 billion compared to

$3.0 billion in the prior year) and repositioning costs ($1.6 billion compared

to $590 million in the prior year).

Excluding the legal and related expenses, net fraud loss in 2013,

repositioning charges and the impact of foreign exchange translation into

U.S. dollars for reporting purposes (FX translation), which lowered reported

expenses by approximately $503 million in 2014 compared to 2013, expenses

were roughly unchanged at $43.9 billion as repositioning savings, expense

reductions in Citi Holdings and other productivity initiatives were fully offset

by the impact of higher regulatory and compliance and volume-related

costs. (Citi’s results of operations excluding the impact of legal and related

expenses, repositioning charges and FX translation are non-GAAP financial

measures. Citi believes the presentation of its results of operations excluding

these impacts provides a more meaningful depiction for investors of the

underlying fundamentals of its businesses.)

Excluding the impact of the net fraud loss in 2013, Citicorp’s expenses

were $47.3 billion, up 12% from the prior year, primarily reflecting higher

legal and related expenses, largely in Corporate/Other ($4.8 billion

compared to $432 million in 2013), higher repositioning costs ($1.6 billion

compared to $547 million in 2013), higher regulatory and compliance

costs and higher volume-related costs, partially offset by efficiency savings.

Excluding the impact of the mortgage settlement in 2014, Citi Holdings’

expenses were $4.0 billion, down 34% from 2013, reflecting lower legal and

related expenses as well as the ongoing decline in Citi Holdings’ assets.

Credit Costs and Allowance for Loan Losses

Citi’s total provisions for credit losses and for benefits and claims of

$7.5 billion declined 12% from 2013. Excluding the impact of the mortgage

settlement in 2014, total provisions for credit losses and for benefits and

claims declined 13% to $7.4 billion versus the prior year. Net credit losses

of $9.0 billion were down 14% versus the prior year. Consumer net credit

losses declined 15% to $8.7 billion, reflecting continued improvements in

the North America mortgage portfolio within Citi Holdings, as well as North

America Citi-branded cards and Citi retail services in Citicorp. Corporate

net credit losses increased 43% to $288 million in 2014. Corporate net credit

losses in 2014 included approximately $113 million of incremental net

credit losses related to the Pemex supplier program in Mexico (for additional

information regarding the Pemex supplier program, see “Institutional

Clients Group” below).

The net release of allowance for loan losses and unfunded lending

commitments was $2.3 billion in 2014. Excluding the impact of the

mortgage settlement in 2014, the net release of allowance for loan losses

and unfunded lending commitments was $2.4 billion in 2014 compared

to a $2.8 billion release in the prior year. Citicorp’s net reserve release

increased to $1.4 billion from $736 million in 2013 due to higher reserve

releases in North America GCB and ICG, reflecting improved credit trends.

Citi Holdings’ net reserve release, excluding the impact of the mortgage

settlement in 2014, decreased 53% to $958 million, primarily due to lower

releases related to the North America mortgage portfolio (which also had

lower net credit losses).

Citigroup’s total allowance for loan losses was $16.0 billion at year end, or

2.50% of total loans, compared to $19.6 billion, or 2.97%, at the end of 2013.

The decline in the total allowance for loan losses reflected the continued

wind down of Citi Holdings and overall continued improvement in the credit

quality of Citi’s loan portfolios. The consumer allowance for loan losses

was $13.6 billion, or 3.68% of total consumer loans, at year end, compared

to $17.1 billion, or 4.34% of total loans, at the end of 2013. The consumer

90+ days past due delinquencies were $4.6 billion, or 1.27% of consumer

loans, at year end, a decline from $5.7 billion or 1.49% of loans in the prior

year. Total non-accrual assets fell to $7.4 billion, a 22% reduction compared

to 2013. Corporate non-accrual loans declined 38% to $1.2 billion, while

Consumer non-accrual loans declined 17% to $5.9 billion, both reflecting the

continued improvement in credit trends.

Capital

Despite the challenging operating environment and elevated legal and

related expenses during 2014, Citi was able to maintain its regulatory

capital, primarily through net income and the further reduction of its DTAs.

Citigroup’s Basel III Tier 1 Capital and Common Equity Tier 1 Capital ratios,

on a fully implemented basis, were 11.5% and 10.6% as of December 31,

2014, respectively, compared to 11.3% and 10.6% as of December 31, 2013

(all based on the Advanced Approaches for determining risk-weighted

assets). Citigroup’s estimated Basel III Supplementary Leverage ratio as

of December 31, 2014 was 6.0% compared to 5.4% as of December 31,

2013, each based on the revised final U.S. Basel III rules. For additional

information on Citi’s capital ratios and related components, see “Capital

Resources” below.

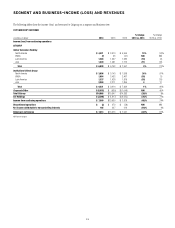

Citicorp

Citicorp net income decreased 32% from the prior year to $10.7 billion.

CVA/DVA, recorded in ICG, was negative $343 million (negative $211 million

after-tax) in 2014, compared to negative $345 million (negative

$214 million after-tax) in the prior year (for a summary of CVA/DVA by

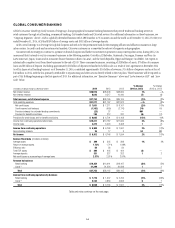

business within ICG, see “Institutional Clients Group” below).

Excluding CVA/DVA as well as the impact of the net fraud loss in Mexico,

the tax items and the divestiture of Credicard noted above, Citicorp’s net

income was $11.1 billion, down 29% from the prior year, as higher expenses,

a higher effective tax rate and lower revenues were partially offset by

continued improvement in credit costs.

Citicorp revenues, net of interest expense, decreased 1% from the prior

year to $71.1 billion. Excluding CVA/DVA, Citicorp revenues were $71.4 billion

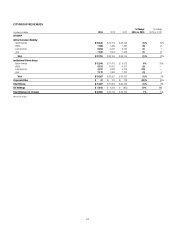

in 2014, also down 1% from the prior year. GCB revenues of $37.8 billion

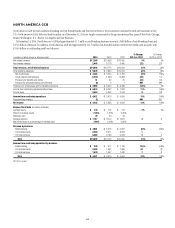

decreased 1% versus the prior year. North America GCB revenues declined

1% to $19.6 billion driven by lower retail banking revenues, partially offset

by higher revenues in Citi-branded cards and Citi retail services. Retail

banking revenues declined 9% to $4.9 billion versus the prior year, primarily

reflecting lower mortgage origination revenues and spread compression in