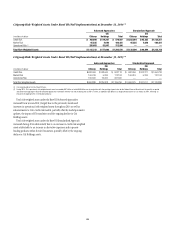

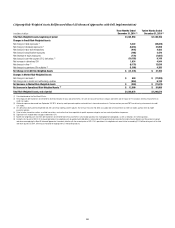

Citibank 2014 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

55

Moreover, in December 2014, the Federal Reserve Board issued a notice of

proposed rulemaking that would establish a risk-based capital surcharge for

global systemically important bank holding companies (GSIB) in the U.S.,

including Citi. The Federal Reserve Board’s proposal is based on the Basel

Committee on Banking Supervision’s (Basel Committee) GSIB surcharge

framework, but adds an alternative method for calculating a U.S. GSIBs score

(and thus its GSIB surcharge), which Citi expects will result in a significantly

higher surcharge than the 2% calculated under the Basel Committee’s

framework (for additional information on the details of the proposal, see

“Capital Resources—Regulatory Capital Standards Developments” above).

The Federal Reserve Board’s GSIB proposal creates ongoing uncertainty

with respect to the ultimate surcharge applicable to Citi due to, among other

things, the (i) requirement to recalculate the surcharge on an annual basis;

(ii) complex calculations required to determine the amount of the surcharge;

and (iii) the score for the indicators aligned with the Basel Committee GSIB

framework is to be determined by converting Citi’s indicators into Euros and

calibrating proportionally against a denominator based upon the aggregate

indicator scores of other large global banking organizations, meaning

that Citi’s score will fluctuate based on actions taken by these banking

organizations, as well as movements in foreign exchange rates. Moreover,

based on the Financial Stability Board’s (FSB) proposed “total loss-absorbing

capacity” (TLAC) requirements, a higher GSIB surcharge would limit the

amount of Common Equity Tier 1 Capital otherwise available to satisfy, in

part, the TLAC requirements and thus potentially result in the need for Citi

to issue higher levels of qualifying debt and preferred equity (for additional

information, see “Regulatory Risks” and “Managing Global Risk—Market

Risk—Funding and Liquidity Risk” below).

In addition to the Federal Reserve Board’s GSIB proposal, various other

proposals which could impact Citi’s regulatory capital framework are also

being considered by regulatory bodies both in the U.S. and internationally,

which further contribute to the uncertainties faced by financial institutions,

including Citi. For example, the SEC has indicated that it is considering

adopting rules that would impose a leverage ratio requirement for U.S.

broker-dealers, which could result in the reduction of certain types of short-

term funding, among other potential negative impacts. In addition, the

Basel Committee continues to review and revise various aspects of its rules,

including its model-based capital framework and standardized approaches to

market, credit and operational risk.

As a result of these ongoing uncertainties, Citi’s capital planning and

management remains challenging. The Federal Reserve Board’s GSIB

surcharge and other U.S. and international proposals could require Citi to

further increase its capital and limit or otherwise restrict how Citi utilizes its

capital, which could negatively impact its businesses, product offerings and

results of operations. It also remains uncertain as to what the overall impact

of these regulatory capital changes will be on Citi’s competitive position,

among both domestic and international peers.

Citi’s Inability to Enhance its 2015 Resolution Plan

Submission Could Subject Citi to More Stringent Capital,

Leverage or Liquidity Requirements, or Restrictions on Its

Growth, Activities or Operations, and Could Eventually

Require Citi to Divest Assets or Operations in Ways That

Could Negatively Impact Its Operations or Strategy.

Title I of The Dodd-Frank Wall Street Reform and Consumer Protection Act

of 2010 (Dodd-Frank Act) requires Citi to prepare and submit annually a

plan for the orderly resolution of Citigroup (the bank holding company)

and its significant legal entities under the U.S. Bankruptcy Code or other

applicable insolvency law in the event of future material financial distress

or failure. Citi is also required to prepare and submit an annual resolution

plan for its primary insured depository institution subsidiary, Citibank, N.A.,

and to demonstrate how Citibank, N.A. is adequately protected from the risks

presented by non-bank affiliates. These plans, which require substantial

effort, time and cost across all of Citi’s businesses and geographies, are

subject to review by the Federal Reserve Board and the FDIC.

In August 2014, the Federal Reserve Board and the FDIC announced

the completion of reviews of the 2013 resolution plans submitted by Citi

and 10 other financial institutions. The agencies identified shortcomings

with the firms’ 2013 resolution plans, including Citi’s. These shortcomings

generally included (i) assumptions that the agencies regarded as unrealistic

or inadequately supported, such as assumptions about the likely behavior

of customers, counterparties, investors, central clearing facilities, and

regulators; and (ii) the failure to make, or identify, the kinds of changes in

firm structure and practices that would be necessary to enhance the prospects

for orderly resolution. At the same time, the Federal Reserve Board and FDIC

indicated that if the identified shortcomings are not addressed in the firms’

2015 plan submissions, the agencies expect to use their authority under Title

I of the Dodd-Frank Act.

Under Title I, if the Federal Reserve Board and the FDIC jointly determine

that Citi’s 2015 resolution plan is not “credible” (which, although not

defined, is generally believed to mean the regulators do not believe the

plan is feasible or would otherwise allow the regulators to resolve Citi in a

way that protects systemically important functions without severe systemic

disruption), Citi could be subjected to more stringent capital, leverage or

liquidity requirements or restrictions, or restrictions on its growth, activities

or operations, and eventually be required to divest certain assets or operations

in ways that could negatively impact its operations and strategy. In August

2014, the FDIC determined that the 2013 resolution plans submitted by the

11 “first wave” filers, including Citi, were “not credible.”

Other jurisdictions, such as the U.K., have also requested or are expected

to request resolution plans from financial institutions, including Citi, and

the requirements and timing relating to these plans are or are expected to

be different from the U.S. requirements and from each other. Responding

to these additional requests will require additional effort, time and cost,

and regulatory review and requirements in these jurisdictions could be in

addition to, or conflict with, changes required by Citi’s regulators in the U.S.