Citibank 2014 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

41

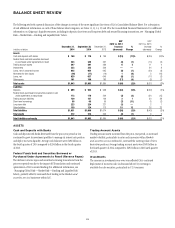

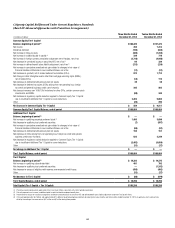

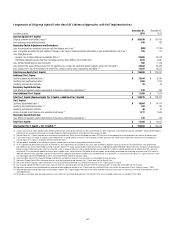

Citigroup Risk-Weighted Assets (Basel III Advanced Approaches with Transition Arrangements)

In millions of dollars

December 31,

2014

December 31,

2013 (14)

Credit Risk (15) $ 862,031 $ 834,082

Market Risk 100,481 112,154

Operational Risk (16) 312,500 231,500

Total Risk-Weighted Assets $1,275,012 $1,177,736

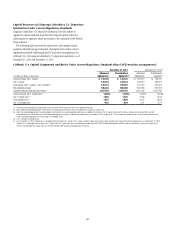

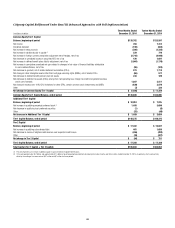

(1) Pro forma presentation of regulatory capital components and tiers based on application of the Final Basel III Rules consistent with current period presentation.

(2) Issuance costs of $124 million and $93 million related to preferred stock outstanding at December 31, 2014 and December 31, 2013, respectively, are excluded from common stockholders’ equity and netted against

preferred stock in accordance with Federal Reserve Board regulatory reporting requirements, which differ from those under U.S. GAAP.

(3) In addition, includes the net amount of unamortized loss on held-to-maturity (HTM) securities. This amount relates to securities that were previously transferred from AFS to HTM, and non-credit related factors such as

changes in interest rates and liquidity spreads for HTM securities with other-than-temporary impairment.

(4) The transition arrangements for significant regulatory capital adjustments and deductions impacting Common Equity Tier 1 Capital and/or Additional Tier 1 Capital are set forth above in the table entitled “Basel III

Transition Arrangements: Significant Regulatory Capital Adjustments and Deductions.”

(5) Common Equity Tier 1 Capital is adjusted for accumulated net unrealized gains (losses) on cash flow hedges included in AOCI that relate to the hedging of items not recognized at fair value on the balance sheet.

(6) The cumulative impact of changes in Citigroup’s own creditworthiness in valuing liabilities for which the fair value option has been elected and own-credit valuation adjustments on derivatives are excluded from

Common Equity Tier 1 Capital, in accordance with the Final Basel III Rules.

(7) Includes goodwill “embedded” in the valuation of significant common stock investments in unconsolidated financial institutions.

(8) Of Citi’s approximately $49.5 billion of net DTAs at December 31, 2014, approximately $25.5 billion of such assets were includable in regulatory capital pursuant to the Final Basel III Rules, while approximately

$24.0 billion of such assets were excluded in arriving at regulatory capital. Comprising the excluded net DTAs was an aggregate of approximately $25.6 billion of net DTAs arising from net operating loss, foreign tax

credit and general business credit carry-forwards as well as temporary differences, of which $14.4 billion were deducted from Common Equity Tier 1 Capital and $11.2 billion were deducted from Additional Tier 1

Capital. In addition, approximately $1.6 billion of net DTLs, primarily consisting of DTLs associated with goodwill and certain other intangible assets, partially offset by DTAs related to cash flow hedges, are permitted to

be excluded prior to deriving the amount of net DTAs subject to deduction under these rules. Separately, under the Final Basel III Rules, goodwill and these other intangible assets are deducted net of associated DTLs in

arriving at Common Equity Tier 1 Capital, while Citi’s current cash flow hedges and the related deferred tax effects are not required to be reflected in regulatory capital.

(9) Aside from MSRs, reflects DTAs arising from temporary differences and significant common stock investments in unconsolidated financial institutions.

(10) Represents Citigroup Capital XIII trust preferred securities, which are permanently grandfathered as Tier 1 Capital under the Final Basel III Rules, as well as 50% of non-grandfathered trust preferred securities. The

remaining 50% of non-grandfathered trust preferred securities are eligible for inclusion in Tier 2 Capital during 2014 in accordance with the transition arrangements for non-qualifying capital instruments under the

Final Basel III Rules.

(11) 50% of the minimum regulatory capital requirements of insurance underwriting subsidiaries must be deducted from each of Tier 1 Capital and Tier 2 Capital.

(12) Under the transition arrangements of the Final Basel III Rules, non-qualifying subordinated debt issuances which consist of those with a fixed-to-floating rate step-up feature where the call/step-up date has not passed

are eligible for 50% inclusion in Tier 2 Capital during 2014, with the threshold based upon the aggregate outstanding principal amounts of such issuances as of January 1, 2014.

(13) Advanced Approaches banking organizations are permitted to include in Tier 2 Capital eligible credit reserves that exceed expected credit losses to the extent that the excess reserves do not exceed 0.6% of credit

risk-weighted assets.

(14) Risk-weighted assets at December 31, 2013 are presented on a pro forma basis, assuming the application of the Final Basel III Rules consistent with current period presentation, including the resultant impact on credit

risk-weighted assets.

(15) Under the Final Basel III Rules, credit risk-weighted assets during the transition period reflect the effects of transitional arrangements related to regulatory capital adjustments and deductions and, as a result, will differ

from credit risk-weighted assets derived under full implementation of the rules.

(16) During 2014, Citi’s operational risk-weighted assets were increased by $81 billion, of which $56 billion was in conjunction with the granting of permission by the Federal Reserve Board to exit the parallel run period

and commence applying the Basel III Advanced Approaches framework, effective with the second quarter of 2014. Further, an additional $25 billion was recognized during the last six months of 2014, reflecting an

evaluation of ongoing events in the banking industry.