Citibank 2014 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2014 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

|

|

113

Regulatory VAR Back-testing

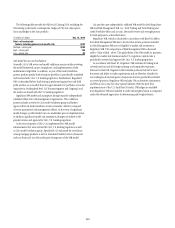

In accordance with Basel III, Citi is required to perform back-testing to

evaluate the effectiveness of its Regulatory VAR model. Regulatory VAR back-

testing is the process in which the daily one-day VAR, at a 99% confidence

interval, is compared to the buy-and-hold profit and loss (e.g., the profit and

loss impact if the portfolio is held constant at the end of the day and re-priced

the following day). Buy-and-hold profit and loss represents the daily mark-

to-market profit and loss attributable to price movements in covered positions

from the close of the previous business day. Buy-and-hold profit and loss

excludes realized trading revenue, net interest, fees and commissions, intra-

day trading profit and loss, and changes in reserves.

Based on a 99% confidence level, Citi would expect two to three days in

any one year where buy-and-hold losses exceeded the Regulatory VAR. Given

the conservative calibration of Citi’s VAR model (as a result of taking the

greater of short- and long-term volatilities and fat-tail scaling of volatilities),

Citi would expect fewer exceptions under normal and stable market

conditions. Periods of unstable market conditions could increase the number

of back-testing exceptions.

The following graph shows the daily buy-and-hold profit and loss

associated with Citi’s covered positions compared to Citi’s one-day Regulatory

VAR during 2014. As the graph indicates, for the 12-month period ending

December 31, 2014, there was one back testing exception where trading

losses exceeded the VAR estimate at the Citigroup level. This occurred

on October 15, 2014, a day on which significant market movements

and volatility impacted various fixed income as well as equities trading

businesses. The difference between the 56% of days with buy-and-hold gains

for Regulatory VAR back-testing and the 94% of days with buy-and-hold

gains shown in the histogram of daily trading related revenue above reflects,

among other things, that a significant portion of Citi’s trading-related

revenue is not generated from daily price movements on these positions and

exposures, as well as differences in the portfolio composition of Regulatory

VAR and Risk Management VAR.

Regulatory Trading VAR and Associated Buy-and-Hold Profit and Loss(1) — Twelve Months Ended December 31, 2014

In millions of dollars

-200

-150

-100

-50

0

50

100

150

Total Regulatory VAR Buy-and-Hold Profit and Loss

Regulatory VAR

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

(1) Buy-and-hold profit and loss, as defined by the banking regulators under Basel III, represents the daily mark-to-market revenue movement attributable to the trading position from the close of the previous business day.

Buy-and-hold profit and loss excludes realized trading revenue, net interest, intra-day trading profit and loss on new and terminated trades, as well as changes in reserves. Therefore it is not comparable to the trading-

related revenue presented in the previous histogram of Daily Trading-Related Revenue.