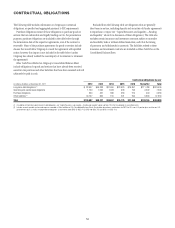

Citibank 2011 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

63

Citi’s ability to increase its common stock dividend

or initiate a share repurchase program is subject to

regulatory and government approval.

Since the second quarter of 2011, Citi has paid a quarterly common stock

dividend of $0.01 per share. In addition to Board of Directors’ approval, any

decision by Citi to increase its common stock dividend, including the amount

thereof, or initiate a share repurchase program is subject to regulatory

approval, including the results of the Comprehensive Capital Analysis and

Review (CCAR) process required by the Federal Reserve Board. Restrictions on

Citi’s ability to increase the amounts of its common stock dividend or engage

in share repurchase programs could negatively impact market perceptions of

Citi, including the price of its common stock.

In addition, pursuant to its agreements with certain U.S. government

entities, dated June 9, 2009, executed in connection with Citi’s exchange

offers consummated in July and September 2009, Citi remains subject

to dividend and share repurchase restrictions for as long as the U.S.

government continues to hold any Citi trust preferred securities acquired

in connection with the exchange offers. While these restrictions may be

waived, they generally prohibit Citi from paying regular cash dividends in

excess of $0.01 per share of common stock per quarter or from redeeming

or repurchasing any Citi equity securities, which includes its common stock,

or trust preferred securities. As of December 31, 2011, approximately $3.025

billion of trust preferred securities issued to the FDIC remained outstanding

(of which approximately $800 million is being held for the benefit of the

U.S. Treasury).

Citi may be unable to maintain or reduce its level of

expenses as it expects, and investments in its businesses

may not be productive.

Citi continues to pursue a disciplined expense-management strategy,

including re-engineering, restructuring operations and improving the

efficiency of functions, such as call centers and collections, to achieve a

targeted percentage expense savings annually. However, there is no guarantee

that Citi will be able to maintain or reduce its level of expenses in the

future, particularly as expenses incurred in Citi’s foreign entities are subject

to foreign exchange volatility, and regulatory compliance and legal and

related costs are difficult to predict or control, particularly given the current

regulatory and litigation environment. Moreover, Citi has incurred, and will

likely continue to incur, costs of investing in its businesses. These investments

may not be as productive as Citi expects or at all. Furthermore, as the wind

down of Citi Holdings slows, Citi’s ability to continue to reduce its expenses as

a result of this wind down will also decline.

The value of Citi’s deferred tax assets (DTAs) could be reduced

if corporate tax rates in the U.S. or certain state or foreign

jurisdictions are decreased or as a result of other potential

significant changes in the U.S. corporate tax system.

There have been discussions in Congress and by the Obama Administration

regarding potentially decreasing the U.S. corporate tax rate. Similar

discussions have taken place in certain state and foreign jurisdictions. While

Citi may benefit in some respects from any decreases in these corporate tax

rates, any reduction in the U.S., state or foreign corporate tax rates would

result in a decrease to the value of Citi’s DTAs, which could be significant.

There have also been recent discussions of more sweeping changes to the

U.S. tax system, including changes to the tax treatment of foreign business

income. It is uncertain whether or when any such tax reform proposals will

be enacted into law, and whether or how they will affect Citi’s ability to make

effective use of its DTAs.

The expiration of a provision of the U.S. tax law that

allows Citi to defer U.S. taxes on certain active financing

income could significantly increase Citi’s tax expense.

Citi’s tax provision has historically been reduced because active financing

income earned and indefinitely reinvested outside the U.S. is taxed at the

lower local tax rate rather than at the higher U.S. tax rate. Such reduction

has been dependent upon a provision of the U.S. tax law that defers the

imposition of U.S. taxes on certain active financing income until that income

is repatriated to the U.S. as a dividend. This “active financing exception”

expired on December 31, 2011 with respect to taxable years beginning after

such date. While the exception has been scheduled to expire on numerous

prior occasions, Congress has extended it each time, including retroactively

to the start of the tax year. Congress could still take action to retroactively

extend the active financing exception to the beginning of 2012. However,

there can be no assurance that it will do so. If the exception is not extended,

the U.S. tax imposed on Citi’s active financing income earned outside

the U.S. would increase, which could further result in Citi’s tax expense

increasing significantly, particularly beginning in 2013.