Citibank 2011 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

95

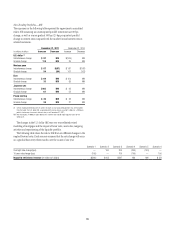

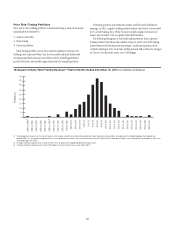

MARKET RISK

Market risk losses arise from fluctuations in the market value of trading

and non-trading positions, including the changes in value resulting from

fluctuations in rates. Market risk encompasses liquidity risk and price risk,

both of which arise in the normal course of business of a global financial

intermediary. For a discussion of funding and liquidity risk, see “Capital

Resources and Liquidity—Funding and Liquidity” above. Price risk is the

earnings risk from changes in interest rates, foreign exchange rates, equity

and commodity prices, and in their implied volatilities. Price risk arises in

non-trading portfolios, as well as in trading portfolios.

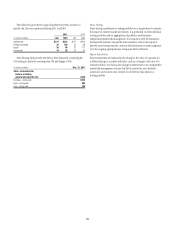

Market risks are measured in accordance with established standards

to ensure consistency across businesses and the ability to aggregate risk.

Each business is required to establish, with approval from Citi’s market risk

management, a market risk limit framework for identified risk factors that

clearly defines approved risk profiles and is within the parameters of Citi’s

overall risk tolerance. These limits are monitored by independent market

risk, country and business Asset and Liability Committees and the Global

Finance and Asset and Liability Committee. In all cases, the businesses are

ultimately responsible for the market risks taken and for remaining within

their defined limits.

Price Risk—Non-Trading Portfolios

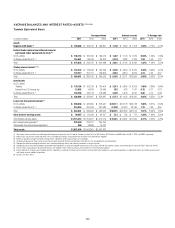

Net interest revenue and interest rate risk

One of Citi’s primary business functions is providing financial products

that meet the needs of its customers. Loans and deposits are tailored to the

customers’ requirements with regard to tenor, index (if applicable) and rate

type. Net interest revenue (NIR), for interest rate exposure (IRE) purposes,

is the difference between the yield earned on the non-trading portfolio assets

(including customer loans) and the rate paid on the liabilities (including

customer deposits or company borrowings). NIR is affected by changes in the

level of interest rates. For example:

At any given time, there may be an unequal amount of assets and

liabilities that are subject to market rates due to maturation or repricing.

Whenever the amount of liabilities subject to repricing exceeds the

amount of assets subject to repricing, a company is considered “liability

sensitive.” In this case, a company’s NIR will deteriorate in a rising

rate environment.

The assets and liabilities of a company may reprice at different speeds or

mature at different times, subjecting both “liability-sensitive” and “asset-

sensitive” companies to NIR sensitivity from changing interest rates. For

example, a company may have a large amount of loans that are subject

to repricing in the current period, but the majority of deposits are not

scheduled for repricing until the following period. That company would

suffer from NIR deterioration if interest rates were to fall.

NIR in any particular period is the result of customer transactions and

the related contractual rates originated in prior periods as well as new

transactions in the current period; those prior-period transactions will be

impacted by changes in rates on floating-rate assets and liabilities in the

current period.

Due to the long-term nature of portfolios, NIR will vary from quarter to

quarter even assuming no change in the shape or level of the yield curve

as assets and liabilities reprice. These repricings are a function of implied

forward interest rates, which represent the overall market’s estimate of future

interest rates and incorporate possible changes in the Federal Funds rate as

well as the shape of the yield curve.

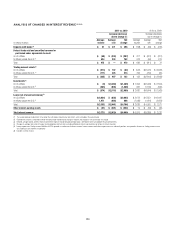

Interest Rate Risk Measurement

Citi’s principal measure of risk to NIR is interest rate exposure (IRE). IRE

measures the change in expected NIR in each currency resulting solely from

unanticipated changes in forward interest rates. Factors such as changes

in volumes, credit spreads, margins and the impact of prior-period pricing

decisions are not captured by IRE. IRE also assumes that businesses make no

additional changes in pricing or balances in response to the unanticipated

rate changes.

For example, if the current 90-day LIBOR rate is 3% and the one-year-

forward rate (i.e., the estimated 90-day LIBOR rate in one year) is 5%, the

+100 bps IRE scenario measures the impact on the company’s NIR of a

100 bps instantaneous change in the 90-day LIBOR to 6% in one year.

The impact of changing prepayment rates on loan portfolios is

incorporated into the results. For example, in the declining interest rate

scenarios, it is assumed that mortgage portfolios prepay faster and income is

reduced. In addition, in a rising interest rate scenario, portions of the deposit

portfolio are assumed to experience rate increases that may be less than the

change in market interest rates.

Mitigation and Hedging of Risk

In order to manage changes in interest rates effectively, Citi may modify

pricing on new customer loans and deposits, enter into transactions with

other institutions or enter into off-balance-sheet derivative transactions that

have the opposite risk exposures. Citi regularly assesses the viability of these

and other strategies to reduce its interest rate risks and implements such

strategies when it believes those actions are prudent.

Citigroup employs additional measurements, including: stress testing the

impact of non-linear interest rate movements on the value of the balance

sheet; the analysis of portfolio duration and volatility, particularly as they

relate to mortgage loans and mortgage-backed securities; and the potential

impact of the change in the spread between different market indices.