Citibank 2011 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

17

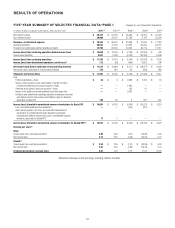

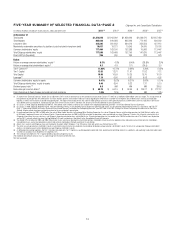

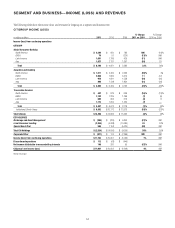

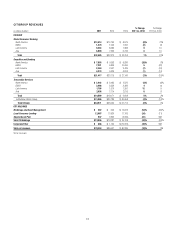

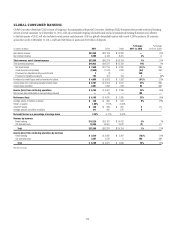

Net interest revenue decreased 8%, driven primarily by lower cards net

interest margin which was negatively impacted by the look-back provision of

The Credit Card Accountability Responsibility and Disclosure Act (CARD Act).

As previously disclosed, the look-back provision of the CARD Act generally

requires a review to be done once every six months for card accounts where

the annual percentage rate (APR) has been increased since January 1, 2009

to assess whether changes in credit risk, market conditions or other factors

merit a future decline in the APR. In addition, net interest margin for cards

was negatively impacted by higher promotional balances and lower total

average loans. As a result, cards net interest revenue as a percentage of

average loans decreased to 9.48% from 10.28% in the prior year. Citi expects

margin growth to remain under pressure into 2012 given the continued

investment spending in the business during 2012, which largely began in the

second half of 2011.

Non-interest revenue decreased 9%, primarily due to lower gains

from the sale of mortgage loans as Citi held more loans on-balance sheet.

In addition, the decline in non-interest revenue reflected lower banking

fee income.

Expenses increased 19%, primarily driven by the higher investment

spending in the business during the second half of 2011, particularly

in cards marketing and technology, and increases in litigation accruals

related to the interchange litigation (see Note 29 to the Consolidated

Financial Statements).

Provisions decreased $5.5 billion, or 71%, primarily due to a loan loss

reserve release of $2.7 billion in 2011, compared to a loan loss reserve release

of $0.3 billion in 2010, and lower net credit losses in the Citi-branded cards

portfolio. Cards net credit losses were down $3.0 billion, or 39%, from 2010,

and the net credit loss ratio decreased 366 basis points to 6.36% for 2011. The

decline in credit costs was driven by improving credit conditions as well as

continued stricter underwriting criteria, which lowered the cards risk profile.

As referenced above, Citi believes the improvements in, and Citi’s resulting

benefit from, declining credit costs in NA RCB will likely slow into 2012.

2010 vs. 2009

Net income declined by $139 million, or 18%, as compared to the prior year,

driven by higher credit costs due to Citi’s adoption of SFAS 166/167, partially

offset by higher revenues.

Revenues increased 72% from the prior year, primarily due to the

consolidation of securitized credit card receivables pursuant to the adoption

of SFAS 166/167 effective January 1, 2010. On a comparable basis, revenues

declined 3% from the prior year, mainly due to lower volumes in Citi-branded

cards as well as the net impact of the CARD Act on cards revenues. This

decrease was partially offset by better mortgage-related revenues driven by

higher refinancing activity.

Net interest revenue was down 6% on a comparable basis driven

primarily by lower volumes in cards, with average managed loans down

7% from the prior year, and in retail banking, where average loans declined

11%. The decline in cards was driven by the stricter underwriting criteria

referenced above as well as the impact of CARD Act. The increase in deposit

volumes, up 3% from the prior year, was offset by lower spreads due to the

then-current interest rate environment.

Non-interest revenue increased 6% on a comparable basis from the prior

year mainly driven by better servicing hedge results and higher gains on sale

from the sale of mortgage loans.

Expenses increased 5% from the prior year, driven by the impact of

higher litigation accruals, primarily in the first quarter of 2010, and higher

marketing costs.

Provisions increased $6.0 billion, primarily due to the consolidation of

securitized credit card receivables pursuant to the adoption of SFAS 166/167.

On a comparable basis, provisions decreased $0.9 billion, or 11%, primarily

due to a net loan loss reserve release of $0.3 billion in 2010 compared to a

$0.5 billion loan loss reserve build in the prior year coupled with lower net

credit losses in the cards portfolio. Also on a comparable basis, the cards

net credit loss ratio increased 61 basis points to 10.02%, driven by lower

average loans.