Citibank 2011 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

80

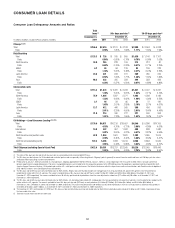

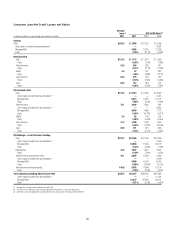

In billions of dollars December 31, 2011 $ECEMBERææ

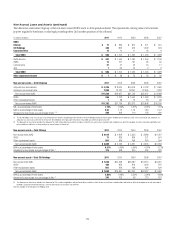

State (1) ENR (2)

ENR

Distribution

90+DPD

%

%

LTV >

100%

Refreshed

FICO %.2æ

%.2æ

$ISTRIBUTION

$0$æ

æ

,46ææ

2EFRESHEDæ

&)#/

#! $11.2 27% 2.3% 50% 721

.9.*#4 9.2 22 2.1 19 715

&, 2.8 7 3.3 69 698

), 1.6 4 2.3 62 705

)./(-) 1.5 4 2.6 66 678

!:.6 1.0 3 4.1 83 706

/THER 13.7 33 2.3 46 695

Total $41.0 100% 2.4% 45% 707

æ #ERTAINæOFæTHEæSTATESæAREæINCLUDEDæASæPARTæOFæAæREGIONæBASEDæONæ#ITISæVIEWæOFæSIMILARæHOMEæPRICESæ(0)æWITHINæTHEæREGION

æ %NDINGæNETæRECEIVABLESæ%XCLUDESæLOANSæINæ#ANADAæANDæ0UERTOæ2ICOæANDæLOANSæSUBJECTæTOæ,43#S

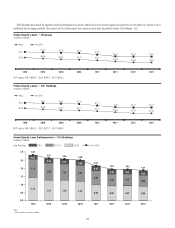

Similar to residential first mortgages (see “Residential First Mortgages—

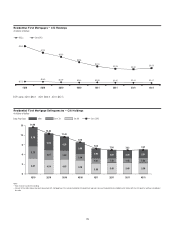

State Delinquency Trends” above), at December 31, 2011, Citi’s home

equity loan portfolio was primarily concentrated in California and the

New York/New Jersey/Connecticut region. Year over year, 90+ days past

due delinquencies improved or remained stable across each of the states

and regions shown in the tables. See also “Consumer Mortgage FICO and

LTV” below.

North America Consumer Mortgages – Loan Loss Reserve Coverage

At December 31, 2011, approximately $9.8 billion of Citi’s total loan loss

reserves of $30.1 billion was allocated to North America real estate lending

in Citi Holdings, representing approximately 31 months of coincident net

credit loss coverage as of such date. With respect to Citi’s aggregate North

America Consumer mortgage portfolio, including Citi Holdings as well as

the residential first mortgages and home equity loans in Citicorp, Citi’s loan

loss reserves of $10.0 billion at December 31, 2011 represented 30 months of

coincident net credit loss coverage.

As evidenced by the tables above, the pace of improvement in home equity

loan delinquencies has slowed or remained flat. Given the lack of market in

which to sell delinquent home equity loans, as well as the relatively smaller

number of home equity loan modifications and modification programs,

Citi’s ability to offset increased delinquencies and net credit losses in its home

equity loan portfolio in Citi Holdings has been more limited as compared to

residential first mortgages, as discussed above. Accordingly, Citi could begin

to experience increased delinquencies and thus increased net credit losses

in this portfolio going forward. Citi has taken these trends and uncertainties

into consideration in determining its loan loss reserves. See “North America

Consumer Mortgages – Loan Loss Reserve Coverage” below.

Home Equity Loans– State Delinquency Trends

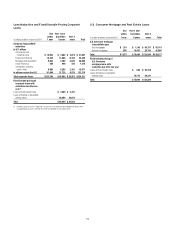

The following tables set forth, for total Citigroup, the six states and/or regions

with the highest concentration of Citi’s home equity loans as of December 31,

2011 and December 31, 2010.

Consumer Mortgage FICO and LTV

As a consequence of the financial crisis, economic environment and the

decrease in housing prices, LTV and FICO scores for Citi’s residential first

mortgage and home equity loan portfolios have generally deteriorated

since origination, particularly in the case of originations between 2006 and

2007, although, as set forth in the tables below, the negative migration has

generally stabilized. Generally, on a refreshed basis, approximately 30%

of residential first mortgages had a LTV ratio above 100%, compared to

approximately 0% at origination. Similarly, approximately 36% of residential

first mortgages had FICO scores less than 660 on a refreshed basis, compared

to 27% at origination. With respect to home equity loans, approximately

45% of home equity loans had refreshed LTVs above 100%, compared

to approximately 0% at origination. Approximately 24% of home equity

loans had FICO scores less than 660 on a refreshed basis, compared to 9%

at origination.