Citibank 2011 Annual Report Download - page 230

Download and view the complete annual report

Please find page 230 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

208

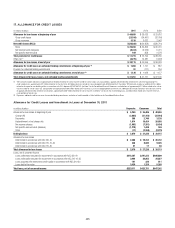

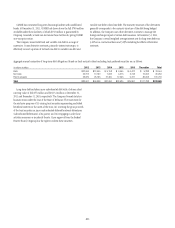

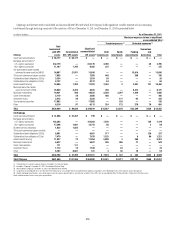

The following table shows reporting units with goodwill balances as of

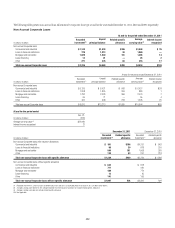

December 31, 2011 and the excess of fair value as a percentage over allocated

book value as of the annual impairment test.

In millions of dollars

Reporting unit (1)

Fair value as a % of

allocated book value Goodwill

North America Regional Consumer Banking 279% $ 2,542

EMEA Regional Consumer Banking 205 349

Asia Regional Consumer Banking 285 5,623

Latin America Regional Consumer Banking 277 1,722

Securities and Banking 136 9,173

Transaction Services 1,761 1,564

Brokerage and Asset Management 162 71

Local Consumer Lending—Cards 175 4,369

æ Local Consumer Lending—OtheræISæEXCLUDEDæFROMæTHEæTABLEæASæTHEREæISæNOæGOODWILLæALLOCATEDæTOæIT

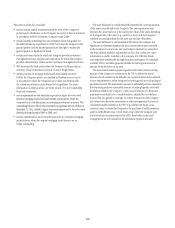

Citigroup engaged the services of an independent valuation specialist

to assist in the valuation of the reporting units at July 1, 2011, using a

combination of the market approach and/or income approach consistent

with the valuation model used in the past.

Under the market approach for valuing each reporting unit, the key

assumption is the selected price multiples. The selection of the multiples

considers the operating performance and financial condition of the reporting

unit operations as compared with those of a group of selected publicly traded

guideline companies and a group of selected acquired companies. Among

other factors, the level and expected growth in return on tangible equity

relative to those of the guideline companies and guideline transactions

is considered. Since the guideline company prices used are on a minority

interest basis, the selection of the multiple considers the recent acquisition

prices, which reflect control rights and privileges, in arriving at a multiple

that reflects an appropriate control premium.

For the valuation under the income approach, the assumptions used

as the basis for the model include cash flows for the forecasted period, the

assumptions embedded in arriving at an estimation of the terminal value

and the discount rate. The cash flows for the forecasted period are estimated

based on management’s most recent projections available as of the testing

date, giving consideration to targeted equity capital requirements based on

selected public guideline companies for the reporting unit. In arriving at the

terminal value for each reporting unit, using 2014 as the terminal year, the

assumptions used include a long-term growth rate and a price-to-tangible

book multiple based on selected public guideline companies for the reporting

unit. The discount rate is based on the reporting unit’s estimated cost of

equity capital computed under the capital asset pricing model.

Embedded in the key assumptions underlying the valuation model,

described above, is the inherent uncertainty regarding the possibility that

economic conditions that affect credit risk and behavior may vary or other

events will occur that will impact the business model. Deterioration in

the assumptions used in the valuations, in particular the discount-rate

and growth-rate assumptions used in the net income projections, could

affect Citigroup’s impairment evaluation and, hence, the Company’s net

income. While there is inherent uncertainty embedded in the assumptions

used in developing management’s forecasts, the assumptions used reflect

management’s best estimates as of the testing date.

If the future were to differ adversely from management’s best estimate of

key economic assumptions and associated cash flows were to significantly

decrease, Citi could potentially experience future impairment charges with

respect to goodwill. Any such charges, by themselves, would not negatively

affect Citi’s Tier 1 and Total Capital regulatory ratios, Tier 1 Common ratio,

its Tangible Common Equity or Citi’s liquidity position.