Citibank 2011 Annual Report Download - page 259

Download and view the complete annual report

Please find page 259 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

237

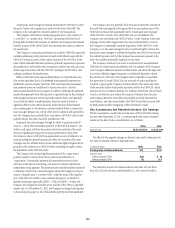

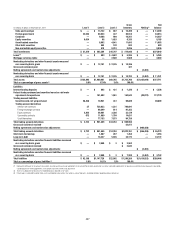

The following table summarizes the gains (losses) on the Company’s fair value hedges for the years ended December 31, 2011, 2010 and 2009:

Gains (losses) on fair value hedges

Year ended December 31,

(1)

In millions of dollars 2011

Gain (loss) on derivatives in designated and qualifying fair value hedges

)NTERESTæRATEæCONTRACTS $ 4,423

&OREIGNæEXCHANGEæCONTRACTS (117)

Total gain (loss) on derivatives in designated and qualifying fair value hedges $ 4,306

Gain (loss) on the hedged item in designated and qualifying fair value hedges

)NTERESTæRATEæHEDGES $(4,296)

&OREIGNæEXCHANGEæHEDGES 26

Total gain (loss) on the hedged item in designated and qualifying fair value hedges $(4,270)

Hedge ineffectiveness recognized in earnings on designated and qualifying fair value hedges

)NTERESTæRATEæHEDGES $ 118

&OREIGNæEXCHANGEæHEDGES 1

Total hedge ineffectiveness recognized in earnings on designated and qualifying fair value hedges $ 119

Net gain (loss) excluded from assessment of the effectiveness of fair value hedges

)NTERESTæRATEæCONTRACTS $9

&OREIGNæEXCHANGEæCONTRACTS (92)

Total net gain (loss) excluded from assessment of the effectiveness of fair value hedges $ (83)

æ !MOUNTSæAREæINCLUDEDæINæOther revenueæONæTHEæ#ONSOLIDATEDæ3TATEMENTæOFæ)NCOMEæ4HEæACCRUEDæINTERESTæINCOMEæONæFAIRæVALUEæHEDGESæISæRECORDEDæINæNet interest revenueæANDæISæEXCLUDEDæFROMæTHISæTABLE

Cash Flow Hedges

Hedging of benchmark interest rate risk

Citigroup hedges variable cash flows resulting from floating-rate liabilities

and rollover (re-issuance) of short-term liabilities. Variable cash flows

from those liabilities are converted to fixed-rate cash flows by entering into

receive-variable, pay-fixed interest rate swaps and receive-variable, pay-fixed

forward-starting interest rate swaps. These cash-flow hedging relationships

use either regression analysis or dollar-offset ratio analysis to assess whether

the hedging relationships are highly effective at inception and on an ongoing

basis. When certain interest rates do not qualify as a benchmark interest

rate, Citigroup designates the risk being hedged as the risk of overall changes

in the hedged cash flows. Since efforts are made to match the terms of the

derivatives to those of the hedged forecasted cash flows as closely as possible,

the amount of hedge ineffectiveness is not significant.

Hedging of foreign exchange risk

Citigroup locks in the functional currency equivalent cash flows of long-

term debt and short-term borrowings that are denominated in a currency

other than the functional currency of the issuing entity. Depending on the

risk management objectives, these types of hedges are designated as either

cash flow hedges of only foreign exchange risk or cash flow hedges of both

foreign exchange and interest rate risk, and the hedging instruments used

are foreign exchange cross-currency swaps and forward contracts. These

cash flow hedge relationships use dollar-offset ratio analysis to determine

whether the hedging relationships are highly effective at inception and on an

ongoing basis.

Hedging total return

Citigroup generally manages the risk associated with highly leveraged

financing it has entered into by seeking to sell a majority of its exposures

to the market prior to or shortly after funding. The portion of the highly

leveraged financing that is retained by Citigroup is generally hedged with a

total return swap.

The amount of hedge ineffectiveness on the cash flow hedges recognized

in earnings for the years ended December 31, 2011, 2010 and 2009 is

not significant.