Citibank 2011 Annual Report Download - page 216

Download and view the complete annual report

Please find page 216 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

194

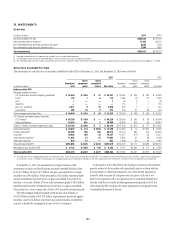

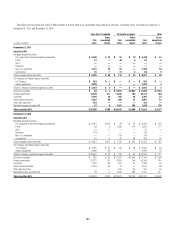

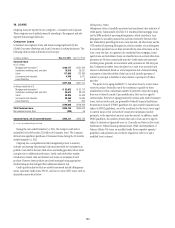

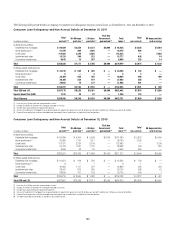

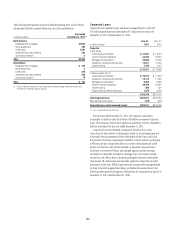

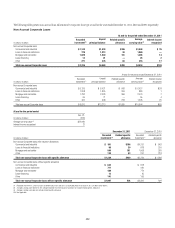

16. LOANS

Citigroup loans are reported in two categories—Consumer and Corporate.

These categories are classified primarily according to the segment and sub-

segment that manages the loans.

Consumer Loans

Consumer loans represent loans and leases managed primarily by the

Global Consumer Banking and Local Consumer Lending businesses. The

following table provides information by loan type:

In millions of dollars Dec. 31, 2011 æ$ECææ

Consumer loans

)Næ53æOFFICES

-ORTGAGEæANDæREALæESTATEæ $139,177

)NSTALLMENTæREVOLVINGæCREDITæANDæOTHER 15,616

#ARDS 117,908

#OMMERCIALæANDæINDUSTRIAL 4,766

,EASEæFINANCING 1

$277,468

)NæOFFICESæOUTSIDEæTHEæ53

-ORTGAGEæANDæREALæESTATEæ $ 52,052 æ

)NSTALLMENTæREVOLVINGæCREDITæANDæOTHER 34,613

#ARDS 38,926

#OMMERCIALæANDæINDUSTRIAL 20,366

,EASEæFINANCING 711

$146,668

Total Consumer loans $424,136

.ETæUNEARNEDæINCOMEæLOSS (405)

Consumer loans, net of unearned income $423,731

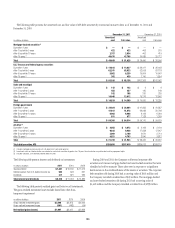

æ ,OANSæSECUREDæPRIMARILYæBYæREALæESTATE

During the year ended December 31, 2011, the Company sold and/or

reclassified (to held-for-sale) $21 billion of Consumer loans. The Company

did not have significant purchases of Consumer loans during the 12 months

ended December 31, 2011.

Citigroup has a comprehensive risk management process to monitor,

evaluate and manage the principal risks associated with its Consumer loan

portfolio. Included in the loan table above are lending products whose terms

may give rise to additional credit issues. Credit cards with below-market

introductory interest rates and interest-only loans are examples of such

products. However, these products are closely managed using appropriate

credit techniques that mitigate their additional inherent risk.

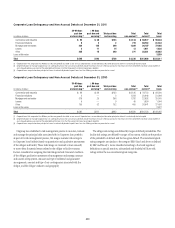

Credit quality indicators that are actively monitored include delinquency

status, consumer credit scores (FICO), and loan to value (LTV) ratios, each as

discussed in more detail below.

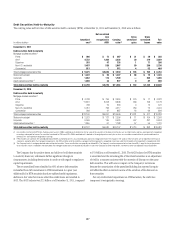

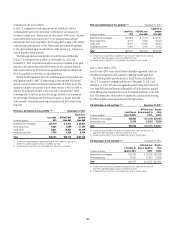

Delinquency Status

Delinquency status is carefully monitored and considered a key indicator of

credit quality. Substantially all of the U.S. residential first mortgage loans

use the MBA method of reporting delinquencies, which considers a loan

delinquent if a monthly payment has not been received by the end of the

day immediately preceding the loan’s next due date. All other loans use the

OTS method of reporting delinquencies, which considers a loan delinquent

if a monthly payment has not been received by the close of business on the

loan’s next due date. As a general rule, residential first mortgages, home

equity loans and installment loans are classified as non-accrual when loan

payments are 90 days contractually past due. Credit cards and unsecured

revolving loans generally accrue interest until payments are 180 days past

due. Commercial market loans are placed on a cash (non-accrual) basis

when it is determined, based on actual experience and a forward-looking

assessment of the collectability of the loan in full, that the payment of

interest or principal is doubtful or when interest or principal is 90 days

past due.

The policy for re-aging modified U.S. Consumer loans to current status

varies by product. Generally, one of the conditions to qualify for these

modifications is that a minimum number of payments (typically ranging

from one to three) be made. Upon modification, the loan is re-aged to

current status. However, re-aging practices for certain open-ended Consumer

loans, such as credit cards, are governed by Federal Financial Institutions

Examination Council (FFIEC) guidelines. For open-ended Consumer loans

subject to FFIEC guidelines, one of the conditions for the loan to be re-aged

to current status is that at least three consecutive minimum monthly

payments, or the equivalent amount, must be received. In addition, under

FFIEC guidelines, the number of times that such a loan can be re-aged is

subject to limitations (generally once in 12 months and twice in five years).

Furthermore, Federal Housing Administration (FHA) and Department of

Veterans Affairs (VA) loans are modified under those respective agencies’

guidelines, and payments are not always required in order to re-age a

modified loan to current.