Citibank 2011 Annual Report Download - page 260

Download and view the complete annual report

Please find page 260 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

238

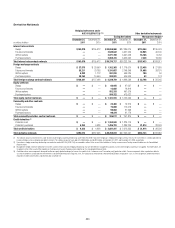

The pretax change in Accumulated other comprehensive income (loss) from cash flow hedges for is presented below:

Year ended December 31,

In millions of dollars 2011

Effective portion of cash flow hedges included in AOCI

)NTERESTæRATEæCONTRACTS $(1,827)

&OREIGNæEXCHANGEæCONTRACTS 81

Total effective portion of cash flow hedges included in AOCI $(1,746)

Effective portion of cash flow hedges reclassified from AOCI to earnings

)NTERESTæRATEæCONTRACTS $(1,224)

&OREIGNæEXCHANGEæCONTRACTS (257)

Total effective portion of cash flow hedges reclassified from AOCI to earnings (1) $(1,481)

æ )NCLUDEDæPRIMARILYæINæOther revenueæANDæNet interest revenue ONæTHEæ#ONSOLIDATEDæ)NCOMEæ3TATEMENT

For cash flow hedges, any changes in the fair value of the end-user

derivative remaining in Accumulated other comprehensive income (loss)

on the Consolidated Balance Sheet will be included in earnings of future

periods to offset the variability of the hedged cash flows when such cash

flows affect earnings. The net loss associated with cash flow hedges expected

to be reclassified from Accumulated other comprehensive income (loss)

within 12 months of December 31, 2011 is approximately $1.1 billion. The

maximum length of time over which forecasted cash flows are hedged is

10 years.

The after-tax impact of cash flow hedges on AOCI is shown in Note 21 to

the Consolidated Financial Statement

Net Investment Hedges

Consistent with ASC 830-20, Foreign Currency Matters—Foreign

Currency Transactions (formerly SFAS 52, Foreign Currency

Translation), ASC 815 allows hedging of the foreign currency risk of a net

investment in a foreign operation. Citigroup uses foreign currency forwards,

options, swaps and foreign-currency-denominated debt instruments to

manage the foreign exchange risk associated with Citigroup’s equity

investments in several non-U.S. dollar functional currency foreign

subsidiaries. Citigroup records the change in the carrying amount of these

investments in the Foreign currency translation adjustment account

within Accumulated other comprehensive income (loss). Simultaneously,

the effective portion of the hedge of this exposure is also recorded in the

Foreign currency translation adjustment account and the ineffective

portion, if any, is immediately recorded in earnings.

For derivatives used in net investment hedges, Citigroup follows the

forward-rate method from FASB Derivative Implementation Group Issue

H8 (now ASC 815-35-35-16 through 35-26), “Foreign Currency Hedges:

Measuring the Amount of Ineffectiveness in a Net Investment Hedge.”

According to that method, all changes in fair value, including changes

related to the forward-rate component of the foreign currency forward

contracts and the time value of foreign currency options, are recorded in the

Foreign currency translation adjustment account within Accumulated

other comprehensive income (loss).

For foreign-currency-denominated debt instruments that are designated

as hedges of net investments, the translation gain or loss that is recorded in

the Foreign currency translation adjustment account is based on the spot

exchange rate between the functional currency of the respective subsidiary

and the U.S. dollar, which is the functional currency of Citigroup. To the

extent the notional amount of the hedging instrument exactly matches the

hedged net investment and the underlying exchange rate of the derivative

hedging instrument relates to the exchange rate between the functional

currency of the net investment and Citigroup’s functional currency (or, in the

case of a non-derivative debt instrument, such instrument is denominated in

the functional currency of the net investment), no ineffectiveness is recorded

in earnings.

The pretax gain (loss) recorded in the Foreign currency translation

adjustment account within Accumulated other comprehensive income

(loss), related to the effective portion of the net investment hedges, is

$904 million, $(3,620) million, and $(4,727) million, for the years ended

December 31, 2011, 2010 and 2009, respectively.

Credit Derivatives

A credit derivative is a bilateral contract between a buyer and a seller

under which the seller agrees to provide protection to the buyer against the

credit risk of a particular entity (“reference entity” or “reference credit”).

Credit derivatives generally require that the seller of credit protection make

payments to the buyer upon the occurrence of predefined credit events

(commonly referred to as “settlement triggers”). These settlement triggers

are defined by the form of the derivative and the reference credit and are

generally limited to the market standard of failure to pay on indebtedness

and bankruptcy of the reference credit and, in a more limited range of

transactions, debt restructuring. Credit derivative transactions referring to

emerging market reference credits will also typically include additional

settlement triggers to cover the acceleration of indebtedness and the risk of

repudiation or a payment moratorium. In certain transactions, protection

may be provided on a portfolio of referenced credits or asset-backed securities.

The seller of such protection may not be required to make payment until a

specified amount of losses has occurred with respect to the portfolio and/or

may only be required to pay for losses up to a specified amount.