Citibank 2011 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

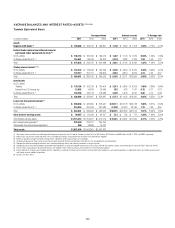

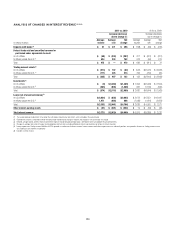

99

The table below provides the range of market factor VARs, inclusive of

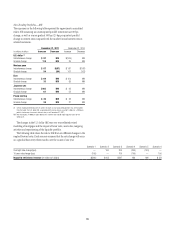

specific risk, that was experienced during 2011 and 2010.

2011

In millions of dollars Low High ,OW (IGH

)NTERESTæRATE $187 $322

&OREIGNæEXCHANGE 34 105

%QUITY 26 86

#OMMODITY 14 36

The following table provides the VAR for S&B during 2011 excluding the

CVA relating to derivative counterparties CVA and hedges of CVA.

In millions of dollars Dec. 31, 2011

Total—all market risk

factors, including

general and specific risk $144

!VERAGEDURINGæYEAR $153

(IGHDURINGæYEAR 205

,OWDURINGæYEAR 104

Stress Testing

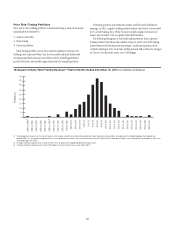

Stress testing is performed on trading portfolios on a regular basis to estimate

the impact of extreme market movements. It is performed on both individual

trading portfolios and on aggregations of portfolios and businesses.

Independent market risk management, in conjunction with the businesses,

develops both systemic and specific stress scenarios, reviews the output of

periodic stress-testing exercises, and uses the information to make judgments

as to the ongoing appropriateness of exposure levels and limits.

Factor Sensitivities

Factor sensitivities are expressed as the change in the value of a position for

a defined change in a market risk factor, such as a change in the value of a

Treasury bill for a one-basis-point change in interest rates. Citi’s independent

market risk management ensures that factor sensitivities are calculated,

monitored, and in most cases, limited, for all relevant risks taken in a

trading portfolio.