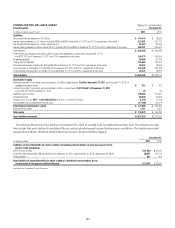

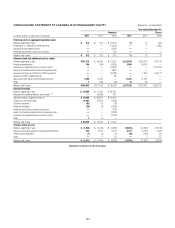

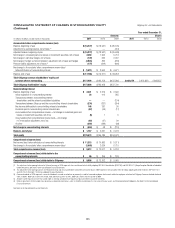

Citibank 2011 Annual Report Download - page 162

Download and view the complete annual report

Please find page 162 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

140

Non-bank loans secured by real estate are written down to the estimated

value of the property, less costs to sell, at the earlier of the receipt of title or

12 months in foreclosure (a process that must commence when payments

are 120 days contractually past due).

Non-bank auto loans are written down to the estimated value of the

collateral, less costs to sell, at repossession or, if repossession is not

pursued, no later than 180 days contractually past due.

Non-bank unsecured personal loans are charged off when the loan is

180 days contractually past due if there have been no payments within

the last six months, but in no event can these loans exceed 360 days

contractually past due.

Unsecured loans in bankruptcy are charged off within 60 days of

notification of filing by the bankruptcy court or in accordance with Citi’s

charge-off policy, whichever occurs earlier.

Real estate-secured loans in bankruptcy are written down to the estimated

value of the property, less costs to sell, at the later of 60 days after

notification or 60 days contractually past due.

Non-bank unsecured personal loans in bankruptcy are charged off when

they are 30 days contractually past due.

Commercial market loans are written down to the extent that principal is

judged to be uncollectable.

Corporate loans

Corporate loans represent loans and leases managed by ICG or the Special

Asset Pool. Corporate loans are identified as impaired and placed on a cash

(non-accrual) basis when it is determined, based on actual experience and

a forward-looking assessment of the collectability of the loan in full, that the

payment of interest or principal is doubtful or when interest or principal is 90

days past due, except when the loan is well collateralized and in the process

of collection. Any interest accrued on impaired Corporate loans and leases

is reversed at 90 days and charged against current earnings, and interest is

thereafter included in earnings only to the extent actually received in cash.

When there is doubt regarding the ultimate collectability of principal, all

cash receipts are thereafter applied to reduce the recorded investment in

the loan.

Impaired Corporate loans and leases are written down to the extent

that principal is judged to be uncollectable. Impaired collateral-dependent

loans and leases, where repayment is expected to be provided solely by

the sale of the underlying collateral and there are no other available and

reliable sources of repayment, are written down to the lower of cost or

collateral value. Cash-basis loans are returned to an accrual status when

all contractual principal and interest amounts are reasonably assured of

repayment and there is a sustained period of repayment performance in

accordance with the contractual terms.

Loans Held-for-Sale

Corporate and Consumer loans that have been identified for sale are

classified as loans held-for-sale included in Other assets. The practice of

the U.S. prime mortgage business has been to sell substantially all of its

conforming loans. As such, U.S. prime mortgage conforming loans are

classified as held-for-sale and the fair value option is elected at the time of

origination. With the exception of these loans for which the fair value option

has been elected, held-for-sale loans are accounted for at the lower of cost

or market value, with any write-downs or subsequent recoveries charged

to Other revenue. The related cash flows are classified in the Consolidated

Statement of Cash Flows in the cash flows from operating activities category

on the line Change in loans held-for-sale.

Allowance for Loan Losses

Allowance for loan losses represents management’s best estimate of probable

losses inherent in the portfolio, as well as probable losses related to large

individually evaluated impaired loans and troubled debt restructurings.

Attribution of the allowance is made for analytical purposes only, and

the entire allowance is available to absorb probable loan losses inherent

in the overall portfolio. Additions to the allowance are made through the

Provision for loan losses. Loan losses are deducted from the allowance, and

subsequent recoveries are added. Assets received in exchange for loan claims

in a restructuring are initially recorded at fair value, with any gain or loss

reflected as a recovery or charge-off to the allowance.

Corporate loans

In the corporate portfolios, the Allowance for loan losses includes an asset-

specific component and a statistically based component. The asset-specific

component is calculated under ASC 310-10-35, Receivables—Subsequent

Measurement (formerly SFAS 114) on an individual basis for larger-

balance, non-homogeneous loans, which are considered impaired. An asset-

specific allowance is established when the discounted cash flows, collateral

value (less disposal costs), or observable market price of the impaired loan is

lower than its carrying value. This allowance considers the borrower’s overall

financial condition, resources, and payment record, the prospects for support

from any financially responsible guarantors (discussed further below)

and, if appropriate, the realizable value of any collateral. The asset-specific

component of the allowance for smaller balance impaired loans is calculated

on a pool basis considering historical loss experience.

The allowance for the remainder of the loan portfolio is calculated under

ASC 450, Contingencies (formerly SFAS 5) using a statistical methodology,

supplemented by management judgment. The statistical analysis considers

the portfolio’s size, remaining tenor, and credit quality as measured by

internal risk ratings assigned to individual credit facilities, which reflect

probability of default and loss given default. The statistical analysis considers

historical default rates and historical loss severity in the event of default,

including historical average levels and historical variability. The result is an

estimated range for inherent losses. The best estimate within the range is

then determined by management’s quantitative and qualitative assessment