Citibank 2011 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

89

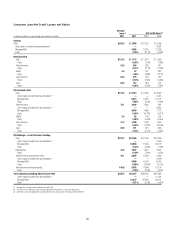

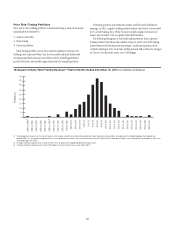

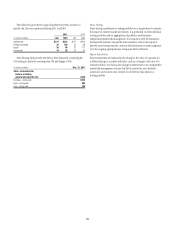

The unpaid principal balance of loans repurchased due to representation

and warranty claims for the years ended December 31, 2011 and 2010,

respectively, was as follows:

December 31, 2011 $ECEMBERææ

In millions of dollars

Unpaid principal

balance

5NPAIDæPRINCIPALææ

BALANCE

'3%S $505

0RIVATEæINVESTORS 8

Total $513

As evidenced in the tables above, Citi’s repurchases have primarily been

from the GSEs. In addition to the amounts set forth in the tables above, Citi

recorded make-whole payments of $530 million and $310 million for the

years ended December 31, 2011 and 2010, respectively.

Repurchase Reserve

Citi has recorded a reserve for its exposure to losses from the obligation to

repurchase or make-whole payments in respect of previously sold loans

(referred to as the repurchase reserve) that is included in Other liabilities

in the Consolidated Balance Sheet. In estimating the repurchase reserve,

Citi considers reimbursements estimated to be received from third-party

correspondent lenders and indemnification agreements relating to previous

acquisitions of mortgage servicing rights. The estimated reimbursements are

based on Citi’s analysis of its most recent collection trends and the financial

solvency of the correspondents.

In the case of a repurchase of a credit-impaired SOP 03-3 loan, the

difference between the loan’s fair value and unpaid principal balance at the

time of the repurchase is recorded as a utilization of the repurchase reserve.

Make-whole payments to the investor are also treated as utilizations and

charged directly against the reserve. The repurchase reserve is estimated

when Citi sells loans (recorded as an adjustment to the gain on sale, which is

included in Other revenue in the Consolidated Statement of Income) and is

updated quarterly. Any change in estimate is recorded in Other revenue.

The repurchase reserve is calculated by individual sales vintage (i.e., the

year the loans were sold). During 2011, the majority of Citi’s repurchases

continued to be from the 2006 through 2008 sales vintages, which also

represented the vintages with the largest loss severity. An insignificant

percentage of repurchases have been from vintages prior to 2006, and Citi

continues to believe that this percentage will continue to decrease, as those

vintages are later in the credit cycle. Although still early in the credit cycle,

Citi continued to experience lower repurchases and loss per repurchase or

make-whole from post-2008 sales vintages.

The repurchase reserve is based on various assumptions. These

assumptions contain a level of uncertainty and risk that, if different from

actual results, could have a material impact on the reserve amounts

(see “Sensitivity of Repurchase Reserve” below). The most significant

assumptions used to calculate the reserve levels are as follows:

Loan documentation requests: Assumptions regarding future expected

loan documentation requests exist as a means to predict future repurchase

claim trends. These assumptions are based on recent historical trends in

loan documentation requests, recent trends in historical delinquencies,

forecasted delinquencies and general industry knowledge about the

current repurchase environment. During 2011, the actual number of loan

documentation requests declined as compared to 2010. However, because

such requests remain elevated from historical levels, and because of the

continued increased focus on mortgage-related matters, the assumption

for estimated future loan documentation requests increased during 2011.

Citi currently believes the level of actual loan documentation requests will

remain elevated from historical levels and will continue to be volatile.

Repurchase claims as a percentage of loan documentation requests:

Given that loan documentation requests are a potential indicator

of future repurchase claims, an assumption is made regarding the

conversion rate from loan documentation requests to repurchase claims,

which assumption is based on historical performance. During 2011, the

conversion rate, or the number of repurchase claims as a percentage of

loan documentation requests, increased as compared to 2010, and thus

the assumption regarding future repurchase claims also increased. Citi

currently believes the claims as a percentage of loan documentation

requests will remain at elevated levels.

Claims appeal success rate: This assumption represents Citi’s

expected success at rescinding a claim by satisfying the demand for

more information, disputing the claim validity, or similar matters. This

assumption is based on recent historical successful appeals rates, which

can fluctuate based on changes in the validity or composition of claims.

During 2011, Citi’s appeal success rate remained stable as compared

to 2010, meaning approximately half of the repurchase claims were

successfully appealed and resulted in no loss to Citi.

Estimated loss per repurchase or make-whole: The assumption of

the estimated loss per repurchase or make-whole payment is based on

actual and estimated losses of recent historical repurchases/make-whole

payments calculated for each sales vintage year in order to capture

volatile housing price highs and lows. The estimated loss per repurchase

or make-whole payment assumption is also impacted by estimates of loan

size at the time of repurchase or make-whole payment. During 2011, the

severity of losses increased slightly as compared to 2010, but was more

than offset by the reduction in loan size, resulting in a decline in the

actual loss per repurchase or make-whole payment. Citi would expect to

continue to see reductions in loan size, including for the 2006 to 2008

sales vintages, as the loans continue to amortize through the loan cycle.