Citibank 2011 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

117

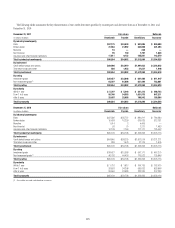

Regardless of the classification of the securities as available-for-sale or

held-to-maturity, Citi assesses each position with an unrealized loss for OTTI.

Management assesses equity method investments with fair value less

than carrying value for OTTI, as discussed in Note 15 to the Consolidated

Financial Statements. For investments that management does not plan to sell

prior to recovery of value, or Citi is not likely to be required to sell, various

factors are considered in assessing OTTI. For investments that Citi plans to

sell prior to recovery of value, or would likely be required to sell and there

is no expectation that the fair value will recover prior to the expected sale

date, the full impairment would be recognized in the Consolidated Statement

of Income.

At December 31, 2011, Citi had several equity method investments that

had temporary impairment, including its investments in Akbank and the

Morgan Stanley Smith Barney joint venture. As of December 31, 2011,

management does not plan to sell those investments prior to recovery of

value and it is not more likely than not that Citi will be required to sell those

investments. For additional information on these equity method investments,

see Note 15 to the Consolidated Financial Statements (Evaluating

Investments for Other-Than-Temporary Impairments) below.

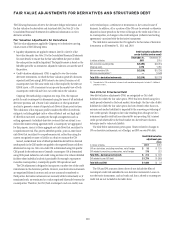

CVA/DVA Methodology

ASC 820-10 requires that Citi’s own credit risk be considered in determining

the market value of any Citi liability carried at fair value. These liabilities

include derivative instruments as well as debt and other liabilities for which

the fair value option has been elected. The credit valuation adjustment (CVA)

is recognized on the balance sheet as a reduction or increase in the associated

derivative asset or liability to arrive at the fair value (carrying value) of

the derivative asset or liability. The debt valuation adjustment (DVA) is

recognized on the balance sheet as a reduction or increase in the associated

fair value option debt liability to arrive at the fair value of the liability. For

additional information, see “Fair Value Adjustments for Derivatives and

Structured Debt” above.

Allowance for Credit Losses

Allowance for Funded Lending Commitments

Management provides reserves for an estimate of probable losses inherent

in the funded loan portfolio on the Consolidated Balance Sheet in the

form of an allowance for loan losses. These reserves are established in

accordance with Citigroup’s credit reserve policies, as approved by the

Audit Committee of the Board of Directors. Citi’s Chief Risk Officer and

Chief Financial Officer review the adequacy of the credit loss reserves each

quarter with representatives from the risk management and finance staffs

for each applicable business area. Applicable business areas include those

having classifiably managed portfolios, where internal credit-risk ratings

are assigned (primarily Institutional Clients Group and Global Consumer

Banking), or modified Consumer loans, where concessions were granted due

to the borrowers’ financial difficulties.

The above-mentioned representatives covering these respective business

areas present recommended reserve balances for their funded and unfunded

lending portfolios along with supporting quantitative and qualitative data.

The quantitative data include:

Estimated probable losses for non-performing, non-homogeneous

exposures within a business line’s classifiably managed portfolio

and impaired smaller-balance homogeneous loans whose terms

have been modified due to the borrowers’ financial difficulties, where

it was determined that a concession was granted to the borrower.

Consideration may be given to the following, as appropriate, when

determining this estimate: (i) the present value of expected future cash

flows discounted at the loan’s original effective rate; (ii) the borrower’s

overall financial condition, resources and payment record; and (iii) the

prospects for support from financially responsible guarantors or the

realizable value of any collateral. When impairment is measured based

on the present value of expected future cash flows, the entire change in

present value is recorded in the Provision for loan losses.

Statistically calculated losses inherent in the classifiably managed

portfolio for performing and de minimis non-performing exposures.

The calculation is based upon: (i) Citigroup’s internal system of credit-risk

ratings, which are analogous to the risk ratings of the major credit rating

agencies; and (ii) historical default and loss data, including rating agency

information regarding default rates from 1983 to 2011, and internal data

dating to the early 1970s on severity of losses in the event of default.

Additional adjustments. These include: (i) statistically calculated

estimates to cover the historical fluctuation of the default rates over the

credit cycle, the historical variability of loss severity among defaulted

loans, and the degree to which there are large obligor concentrations in

the global portfolio; and (ii) adjustments made for specifically known

items, such as current environmental factors and credit trends.

In addition, representatives from both the risk management and finance

staffs that cover business areas with delinquency-managed portfolios

containing smaller homogeneous loans present their recommended reserve

balances based upon leading credit indicators, including loan delinquencies

and changes in portfolio size, as well as economic trends, including housing

prices, unemployment and GDP. This methodology is applied separately for

each individual product within each different geographic region in which

these portfolios exist.