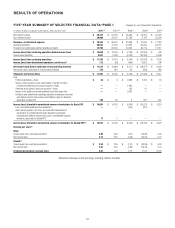

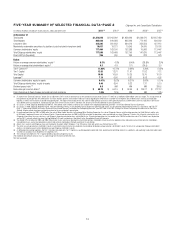

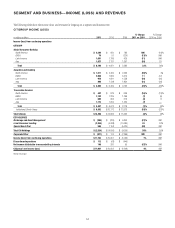

Citibank 2011 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2011 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

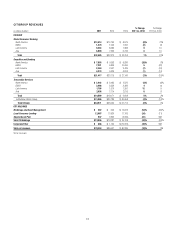

16

NORTH AMERICA REGIONAL CONSUMER BANKING

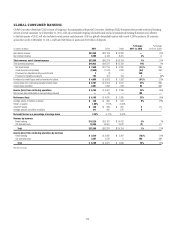

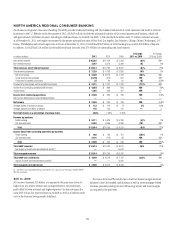

North America Regional Consumer Banking (NA RCB) provides traditional banking and Citi-branded card services to retail customers and small to mid-size

businesses in the U.S. Effective in the first quarter of 2012, NA RCB will also include the substantial majority of Citi’s retail partner cards business, which will

add approximately $45 billion of assets, including $41 billion of loans, to NA RCB. NA RCB’s 1,016 retail bank branches and 12.7 million customer accounts,

as of December 31, 2011, are largely concentrated in the greater metropolitan areas of New York, Los Angeles, San Francisco, Chicago, Miami, Washington, D.C.,

Boston, Philadelphia and certain larger cities in Texas. At December 31, 2011, NA RCB had $38.9 billion of retail banking loans and $148.8 billion of deposits.

In addition, NA RCB had 22.0 million Citi-branded credit card accounts, with $75.9 billion in outstanding card loan balances.

In millions of dollars 2011

% Change

2011 vs. 2010

æ#HANGEæ

æVSæ

.ETæINTERESTæREVENUE $ 10,367 (8)% .-

.ONINTERESTæREVENUE 3,247 (9)

Total revenues, net of interest expense $ 13,614 (8)%

4OTALæOPERATINGæEXPENSES $ 7,329 19%

.ETæCREDITæLOSSES $ 4,949 (38)% .-

#REDITæRESERVEæBUILDæRELEASE (2,740) NM .-

0ROVISIONSæFORæBENEFITSæANDæCLAIMS 22 (8)

0ROVISIONSæFORæLOANæLOSSESæANDæFORæBENEFITSæANDæCLAIMS $ 2,231 (71)% .-

)NCOMEæFROMæCONTINUINGæOPERATIONSæBEFOREæTAXES $ 4,054 NM

)NCOMEæTAXESæ 1,465 NM

Income from continuing operations $ 2,589 NM

.ETæINCOMEæATTRIBUTABLEæTOæNONCONTROLLINGæINTERESTS — —

Net income $ 2,589 NM

!VERAGEæASSETSæ(in billions of dollars) $ 123 3%

!VERAGEæDEPOSITS (in billions of dollars) 145 —

Net credit losses as a percentage of average loans 4.60%

Revenue by business

2ETAILæBANKING $ 5,111 (4)%

#ITIBRANDEDæCARDS 8,503 (10) .-

Total $ 13,614 (8)%

Income (loss) from continuing operations by business

2ETAILæBANKING $ 488 (36)%

#ITIBRANDEDæCARDS 2,101 NM .-

Total $ 2,589 NM

Total GAAP revenues $ 13,614 (8)%

.ETæIMPACTæOFæCREDITæCARDæSECURITIZATIONSæACTIVITYæ —

Total managed revenues $ 13,614

Total GAAP net credit losses $ 4,949 (38)% .-

)MPACTæOFæCREDITæCARDæSECURITIZATIONSæACTIVITYæ —

Total managed net credit losses $ 4,949

ææ 3EEæ.OTEææTOæTHEæ#ONSOLIDATEDæ&INANCIALæ3TATEMENTSæFORæAæDISCUSSIONæOFæTHEæIMPACTæOFæ3&!3æ

.-æ .OTæMEANINGFUL

2011 vs. 2010

Net income increased $1.9 billion as compared to the prior year, driven by

higher loan loss reserve releases and an improvement in net credit losses,

partly offset by lower revenues and higher expenses. Citi does not expect the

same level of loan loss reserve releases in NA RCB in 2012 as it believes credit

costs in the business have generally stabilized.

Revenues decreased 8% mainly due to lower net interest margin and loan

balances in the Citi-branded cards business as well as lower mortgage-related

revenues, primarily relating to lower refinancing activity and lower margins

as compared to the prior year.