Capital One 2010 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2010 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

64

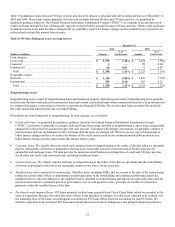

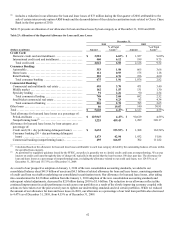

The following table sets forth the original principal balance of mortgage loan originations by vintage for the three general categories

of purchasers of mortgage loans:

Table 24: Original Principal Balance of Mortgage Loans Originated and Sold to Third Parties Based on Category of Purchaser

(Dollars in billions) 2005 2006 2007 2008 Total

Government sponsored enterprises (“GSEs”)(1) ...................... $ 3 $ 3 $ 4 $ 1 $ 11

Insured Securitizations ............................................ 9 8 1 0 18

Uninsured Securitizations and Other ............................... 33 30 16 3 82

Total .......................................................... $ 45 $ 41 $ 21 $ 4 $ 111

________________________

(1) GSEs include Fannie Mae and Freddie Mac.

Between 2005 and 2008, our subsidiaries sold an aggregate amount of $11 billion in original principal balance mortgage loans to the

GSEs.

Of the $18 billion in original principal balance of mortgage loans sold directly by our subsidiaries to private-label purchasers who

placed the loans into securitizations supported by bond insurance (“Insured Securitizations”), approximately $13 billion original

principal balance was placed in securitizations as to which the monoline bond insurers have made repurchase requests or loan file

requests to one of our subsidiaries (“Active Insured Securitizations”), and the remaining approximately $5 billion original

principal balance was placed in securitizations as to which the monoline bond insurers have not made repurchase requests or loan file

requests to one of our subsidiaries (“Inactive Insured Securitizations”). Insured Securitizations often allow the monoline bond insurer

to act independently of the investors. Bond insurers typically have indemnity agreements directly with both the mortgage originators

and the securitizers, and they often have super-majority rights within the trust documentation that allow them to direct trustees to

pursue mortgage repurchase requests without coordination with other investors.

Because we do not service most of the loans our subsidiaries sold to others, we do not have complete information about the current

ownership of the $82 billion in original principal balance of mortgage loans not sold directly to GSEs or placed in Insured

Securitizations. We have determined from third-party databases that about $39 billion original principal balance of these mortgage

loans are currently held by private-label publicly issued securitizations not supported by bond insurance (“Uninsured Securitizations”).

In contrast with the bond insurers in Insured Securitizations, investors in Uninsured Securitizations often face a number of legal and

logistical hurdles before they can direct a securitization trustee to pursue mortgage repurchases, including the need to coordinate with

a certain percentage of investors holding the securities and to indemnify the trustee for any litigation it undertakes. An additional

approximately $30 billion original principal balance of mortgage loans were initially sold to private investors as whole loans. Of this

amount, we believe approximately $10 billion original principal balance of mortgage loans were ultimately purchased by GSEs. For

purposes of our reserves-setting process, we consider these loans to be private-label loans rather than GSE loans. We do not have

information about the current holders or disposition of the remaining $13 billion original principal balance mortgage loans in this

category.

With respect to the $111 billion in original principal balance of mortgage loans originated and sold to others between 2005 and 2008,

we estimate that approximately $45 billion in unpaid principal balance remains outstanding, approximately $12 billion in losses have

been realized, and approximately $13 billion in unpaid principal balance is at least 90 days delinquent. Because we do not service

most of the loans we sold to others, we do not have complete information about the underlying credit performance levels of these

mortgage loans, but these amounts reflect our best estimates based on available data, including extrapolated estimates for the $13

billion original principal balance of mortgage loans about which we do not have information about the current holders. These

estimates could change as we get additional data or refine our analysis.

As of December 31, 2010, the subsidiaries had open repurchase requests relating to approximately $1.6 billion original principal

balance of mortgage loans as compared with $1.0 billion as of December 31, 2009.

Over the last year, the vast majority of new repurchase demands received and, as discussed below, almost all of our $816 million

reserves, relate to the $24 billion of original principal balance of mortgage loans originally sold to the GSEs or to Active Insured

Securitizations. Currently, repurchase demands predominantly relate to the 2006 and 2007 vintages. We have received relatively few

repurchase demands from the 2008 and 2009 vintages, mostly because GreenPoint ceased originating mortgages in August 2007.