Capital One 2010 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2010 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

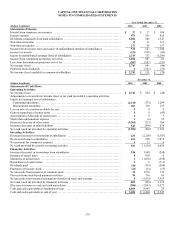

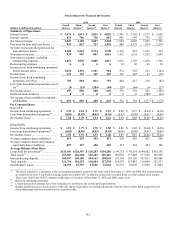

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED STATEMENTS

172

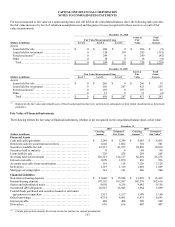

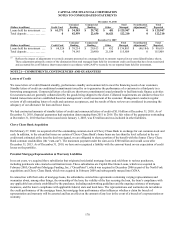

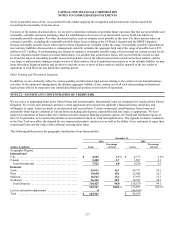

As of December 31, 2010, the subsidiaries had open repurchase requests relating to approximately $1.6 billion original principal

balance of mortgage loans as compared with $1.0 billion as of December 31, 2009.

Over the last year, the vast majority of new repurchase demands received and, as discussed below, almost all of our $816 million

reserves, relate to the $24 billion of original principal balance of mortgage loans originally sold to the GSEs or to Active Insured

Securitizations. Currently, repurchase demands predominantly relate to the 2006 and 2007 vintages. We have received relatively few

repurchase demands from the 2008 and 2009 vintages, mostly because GreenPoint ceased originating mortgages in August 2007.

The following tables set forth information on pending repurchase requests by counterparty category and timing of initial repurchase

request:

Open Pipeline All Vintages (all entities) (1)

(Dollars in millions) (All amounts are Original

Principal Balance)

Open

Claims at

12/31/09

Gross New

Demands

Received in

2010

Loans

Repurchased/Made

Whole in 2010(2)

Demands

Rescinded

in 2010(2)

Open

Claims at

12/31/10

GSEs .........................................

.

$ 61 $ 204 $ (52) $ (87) $ 126

Insured Securitizations .........................

.

366 645 (179) 0 832

Uninsured Securitizations and Others ............

.

588 104 (5) (22) 665

Total ........................................

.

$ 1,015 $ 953 $ (236) $ (109) $ 1,623

________________________

(1) The open pipeline includes all repurchase requests ever received by our subsidiaries where either the requesting party has not formally rescinded

the repurchase request and where our subsidiary has not agreed to either repurchase the loan at issue or make the requesting party whole with

respect to its losses. Accordingly, repurchase requests denied by our subsidiaries and not pursued by the counterparty remain in the open

pipeline. Moreover, repurchase requests submitted by parties without contractual standing to pursue repurchase requests are included within the

open pipeline unless the requesting party has formally rescinded its repurchase request. Finally, the amounts reflected in this chart are the

original principal balance amounts of the mortgage loans at issue and do not correspond to the losses our subsidiary would incur upon the

repurchase of these loans.

(2) Activity in 2010 relates to repurchase demands from all years.

We have established representation and warranty reserves for losses that we consider to be both probable and reasonably estimable

associated with the mortgage loans sold by each subsidiary, including both litigation and non-litigation liabilities. These reserves are

reported in our consolidated balance sheets as a component of other liabilities. The reserve-setting process relies heavily on estimates,

which are inherently uncertain, and requires the application of judgment. We evaluate these estimates on a quarterly basis. We build

our representation and warranty reserves through the provision for repurchase losses, which we report in our consolidated statements

of income as a component of non-interest income for loans originated and sold by Chevy Chase Bank and Capital One Home Loans

and as a component of discontinued operations for loans originated and sold by GreenPoint. In establishing the representation and

warranty reserves, we consider a variety of factors depending on the category of purchaser.

In establishing reserves for the $11 billion original principal balance of GSE loans, we rely on the historical relationship between GSE

loan losses and repurchase outcomes to estimate: (1) the percentage of current and future GSE loan defaults that we anticipate will

result in repurchase requests from the GSEs over the lifetime of the GSE loans; and (2) the percentage of those repurchase requests

that we anticipate will result in actual repurchases. We also rely on estimated collateral valuations and loss forecast models to estimate

our lifetime liability on GSE loans. This reserving approach to the GSE loans reflects the historical interaction with the GSEs around

repurchase requests. The GSEs have stronger contractual rights than non-GSE counterparties because GSE contracts typically do not

contain prompt notice requirements for repurchase requests or materiality qualifications to the representations and warranties.

Moreover, although we often disagree with the GSEs about the validity of their repurchase requests, we have established a negotiation

pattern whereby the GSEs and our subsidiaries continually negotiate around individual repurchase requests, leading to the GSEs

rescinding some repurchase requests and our subsidiaries agreeing in some cases to repurchase some loans or make the GSEs whole

with respect to losses. Our lifetime representation and warranty reserves with respect to GSE loans are grounded in this history.

For the $13 billion original principal balance in Active Insured Securitizations, our reserving approach also reflects our historical

interaction with monoline bond insurers around repurchase requests. Typically, monoline bond insurers allege a very high repurchase

rate with respect to the mortgage loans in the Active Insured Securitization category. In response to these repurchase requests, our

subsidiaries typically request information from the monoline bond insurers demonstrating that the contractual requirements for a valid

repurchase request have been satisfied, typically, for example, that the counterparty promptly notify us upon discovery of any breach

and that any breach materially and adversely affect the value of the mortgage loan at issue. In response to these requests for supporting