Capital One 2010 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2010 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED STATEMENTS

129

We continue to service some of the outstanding balance of securitized mortgage receivables. We also retain rights to future cash flows

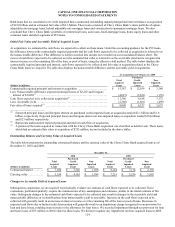

arising from the receivables, the most significant being certificated interest-only bonds issued by the trusts, certain of which we sold

during the year ended December 31, 2010. We generally estimate the fair value of these retained interests based on the estimated

present value of expected future cash flows from securitized and sold receivables, using our best estimates of the key assumptions –

credit losses, prepayment speeds and discount rates commensurate with the risks involved.

In connection with the securitization of certain option arm mortgage loans, a third party is obligated to advance a portion of any

“negative amortization” resulting from monthly payments that are less than the interest accrued for that payment period. We have an

agreement in place with the third party that mirrors this advance requirement. The amount advanced is tracked through mortgage-

backed securities retained as part of the securitization transaction. As the borrowers make principal payments, these securities receive

their net pro rata portion of those payments in cash, and advances of negative amortization are refunded accordingly. As advances

occur, we record an asset in the form of negative amortization bonds, which are classified as available-for-sale securities. We have

also entered into certain derivative contracts related to the securitization activities. These are classified as free standing derivatives,

with fair value adjustments recorded in non-interest income. See “Note 11—Derivative Instruments and Hedging Activities” for

further details on these derivatives.

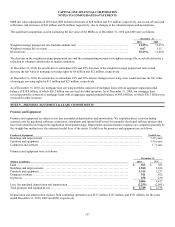

Prior to January 1, 2010, 21 mortgage securitization trusts were off-balance sheet due to the QSPE exemption from the consolidation

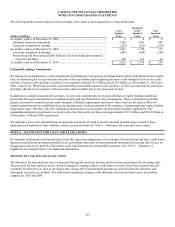

provisions of the previous consolidation guidance. Upon the adoption of the new consolidation guidance on January 1, 2010, we were

required to consolidate 15 of the mortgage trusts because we were considered the primary beneficiary of the impacted trusts, due to the

power held through our servicing rights and due to the right to receive benefits that could potentially be significant to the trusts

through the interest-only bonds we retained. As a result of consolidation, we recorded a $1.5 billion increase to loans held for

investment, a $73 million increase to the allowance for loan losses, a $1.5 billion increase to securitized debt obligations, a $29

million decrease to other net assets, and a $114 million reduction in stockholders’ equity. As part of the consolidation, we eliminated

retained interests from our consolidated balance sheet, including mortgage servicing rights, interest-only bonds and negative

amortization bonds. See “Note 1—Summary of Significant Accounting Policies.”

On March 10, 2010, we sold the interest-only bonds associated with each of the consolidated mortgage trusts to a third party. While

continuing to service the related loans, we are no longer considered the primary beneficiary of the mortgage trusts because without the

interest-only bonds, we no longer have the right to receive benefits that could potentially be significant nor the obligation to absorb

losses that could potentially be significant to the trusts. Therefore, we deconsolidated the mortgage trusts as of March 10, 2010.

Deconsolidation resulted in the removal of all trust assets and liabilities from the consolidated balance sheet including $1.5 billion of

mortgage loan receivables along with the related allowance of $73 million, debt securities held by third party investors of $1.5 billion,

and other net assets of $52 million. It also resulted in the recognition on the consolidated balance sheet of $64 million of interests in

the mortgage securitization that continued to be retained after the sale of the interest-only bonds, including mortgage servicing rights,

negative amortization bonds, and other interests. The deconsolidation resulted in an increase to non-interest income of $128 million.

The remaining mortgage trusts with $3.0 billion of outstanding mortgage loans and $3.1 billion of securities issued to third parties

were not consolidated because we are no longer servicing the mortgage loans and are not considered to be the primary beneficiary of

the mortgage trusts. These trusts were not consolidated upon initial adoption because the insurer of the mortgage securitization had the

power to remove us as the servicer of the loans prior to the adoption of the new consolidation standards and formally exercised that

right during the first quarter of 2010.

GreenPoint Mortgage HELOCs

Our discontinued wholesale mortgage banking unit, GreenPoint, previously sold home equity lines of credit in whole loan sales and

subsequently acquired a residual interest in certain trusts which securitized some of those loans. As the residual interest holder,

GreenPoint is required to fund advances on the home equity lines of credit when certain performance triggers are met due to

deterioration in asset performance. We have funded $26 million in advances through December 31, 2010, all of which has been

expensed as funded. Our unfunded commitment related to these residual interests was $13 million as of December 31, 2010. We did

not consolidate the trusts because the residual certificates did not provide the obligation to absorb losses or the right to receive benefits

that could potentially be significant to the trusts.

GreenPoint Mortgage Manufactured Housing

We retain the primary obligation for certain provisions of corporate guarantees, recourse sales and clean-up calls related to the

discontinued manufactured housing operations of GreenPoint Credit LLC (“GPC”) which was sold to a third party in 2004. Although

we are the primary obligor, recourse obligations related to former GPC whole loan sales, commitments to exercise mandatory clean-up

calls on certain GPC securitization transactions and servicing were transferred to a third party in the sale transaction. We do not