Capital One 2010 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2010 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

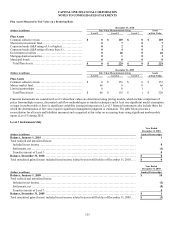

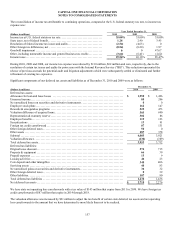

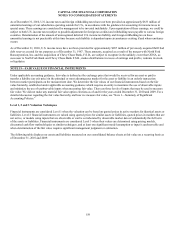

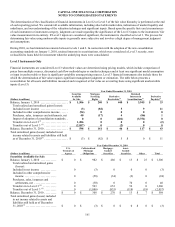

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED STATEMENTS

164

The following describes the valuation techniques used in estimating the fair value of our financial instruments as of December 31,

2010 and 2009. We applied the fair value provisions, to the financial instruments not recognized on the consolidated balance sheet at

fair value, which include loans held for investment, interest receivable, non-interest bearing and interest bearing deposits, other

borrowings, senior and subordinated notes, and interest payable. The provisions requiring us to maximize the use of observable inputs

and to measure fair value using a notion of exit price were factored into our selection of inputs of our established valuation techniques.

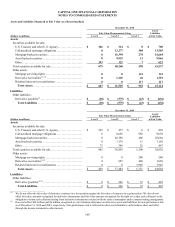

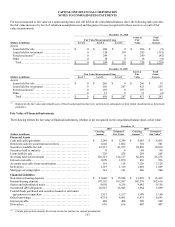

Financial Assets

Cash and Cash Equivalents

The carrying amounts of cash and due from banks, federal funds sold and resale agreements and interest-bearing deposits at other

banks approximate fair value.

Restricted Cash or Securitization Investors

The carrying amounts of restricted cash for securitization investors approximate their fair value due to their relatively short-term

nature.

Securities Held To Maturity

The carrying amounts of securities held to maturity, which consists of negative amortization bonds, approximate fair value. We

recorded these securities at fair value on the date of acquisition. Fair value is determined using a discounted cash flow method, a form

of the income approach. Discount rates were determined considering market rates at which similar instruments would be sold to third

parties.

Securities Available For Sale

Quoted prices in active markets are used to measure the fair value of U.S. Treasury securities. For other investment categories, we

utilize multiple third party pricing services to obtain fair value measures for the large majority of our securities. A pricing service may

be considered as the primary pricing provider for certain types of securities, and the designation of the primary pricing provider may

vary depending on the type of securities. The determination of the primary pricing provider is based on our experience and validation

benchmark of the pricing service’s performance in terms of providing fair value measurement for the various types of securities.

Certain securities available for sale are classified as Level 2 and 3, the majority of which are collateralized mortgage obligations and

mortgage-backed securities. Classification indicates that significant valuation assumptions are not consistently observable in the

market. When significant assumptions are not consistently observable, fair values are derived using the best available data. Such data

may include quotes provided by a dealer, the use of external pricing services, independent pricing models, or other model-based

valuation techniques such as calculation of the present values of future cash flows incorporating assumptions such as benchmark

yields, spreads, prepayment speeds, credit ratings, and losses. The techniques used by the pricing services utilize observable market

data to the extent available. Pricing models may be used, which can vary by asset class and may incorporate available trade, bid and

other market information. Across asset classes, information such as trader/dealer input, credit spreads, forward curves, and

prepayment speeds are used to help determine appropriate valuations. Because many fixed income securities do not trade on a daily

basis, the evaluated pricing applications may apply available information through processes such as benchmarking curves, like

securities, sector groupings, and matrix pricing to prepare valuations. In addition, model processes are used by the pricing services to

develop prepayment and interest rate scenarios.

We validate the pricing obtained from the primary pricing providers through comparison of pricing to additional sources, including

other pricing services, dealer pricing indications in transaction results, and other internal sources. Pricing variances among different

pricing sources are analyzed and validated.

As of December 31, 2010, we saw significant improvements in the market value of our portfolio holdings driven by stabilization of

the financial markets and reduced risk premiums as compared to 2009. The decrease in the amount of Level 3 securities reflected

continued run-off of the securities, the liquidation of our CMBS and MBS securities, and improvement in pricing consistency.