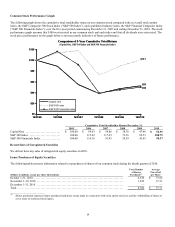

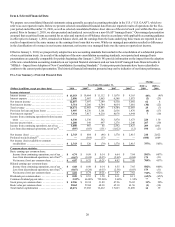

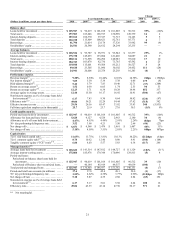

Capital One 2010 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2010 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

28

Actual results could differ materially from those in our forward-looking statements. Forward-looking statements do not reflect (i) any

change in current dividend or repurchase strategies, (ii) the effect of any acquisitions, divestitures or similar transactions or (iii) any

changes in laws, regulations or regulatory interpretations, in each case after the date as of which such statements are made. See

“Forward-Looking Statements” in “Item 1. Business” of this report for factors that could materially influence our results.

Total Company Expectations

We believe we are emerging from the recession in a strong position to deliver attractive and sustainable results over the long-term,

including moderate growth and attractive risk-adjusted returns on assets in our Credit Card and Auto Finance businesses, moderate

growth in low-risk loans in our Commercial Banking business and strong growth in low-cost deposits and high-quality commercial

and retail customer relationships. Based on recent trends and our targeted initiatives to attract new business and develop customer

relationships, we believe there is reasonable potential for loan growth during 2011, which will depend on consumer demand.

• Total Loans: Loan balances stabilized in the second half of 2010, reflecting the decline in charge-offs, gradual abatement of

expected portfolio run-offs and seasonal consumer spending trends. The lower starting point for loan balances from 2010 will

cause the average loan balances in 2011 to be comparable to 2010, even as we expect period-end balances to grow. The timing

and pace of expected growth will depend on broader economic trends that impact overall consumer and commercial demand.

• Expenses: We anticipate that non-interest expenses will increase in 2011, assuming that the increase in marketing opportunities

we observed in late 2010 continues through 2011.

• Provision for Loan and Lease Losses: Based on the underlying credit trends we are experiencing, we expect that charge-offs will

continue their downward trend, although the pace of the allowance releases of 2010 is likely to abate during 2011. We expect that

the improvement in credit trends in our Consumer Lending businesses will continue to outpace the economic recovery. We

believe that the worst of the Commercial Banking business credit downturn is behind us; however, we expect a few more quarters

of fluctuations in the charge-off and nonperforming loan metrics in our Commercial Banking business.

• Margins: Margins will be affected as the onboarding of lower yield and lower loss assets are offset by a lower year-over-year

average cost of funds and higher transaction volume. We expect margins to remain at strong levels, although they may drift

downward modestly, depending upon the competitive environment and the timing and pace of loan growth. We expect continued

funding mix shift towards deposits in 2011, which should provide modest funding cost benefits to net interest margin.

• Capital: We expect regulatory capital ratios to rise steadily after a temporary decline in the first quarter of 2011. Although capital

measures such as our non-GAAP TCE are expected to rise steadily, we expect our Tier 1 risk-based capital ratio and our non-

GAAP Tier 1 common equity ratio to decline into the first quarter of 2011, primarily due to two factors that affect the numerator

and denominator used in calculating these ratios: (i) a decrease in the numerator resulting from the disallowance of a portion of

the deferred tax assets and (ii) an increase in the denominator due to the remaining phase-in during the first quarter of 2011 of

risk-weighted assets resulting from the new consolidation accounting standards. Even with the expected increase in our loan

balances, the completion of this consolidation will most likely lead to slower growth in the denominator of our regulatory capital

ratios over the next couple of years as compared to the recent past. We expect the numerator of these ratios will rise not only as

we generate earnings but also with the steady decline in our disallowed deferred tax asset amount, which we expect will be

around $2.0 billion at the end of the first quarter of 2011 and will largely disappear over the next couple of years.

Based on the current definitions proposed by the Basel Committee, we expect to exceed in 2011 the Basel III minimum common

equity ratio, including the capital conservation buffer.

We expect that our strong capital position and generation will enable us to deploy capital in the service of shareholders to

generate attractive returns in 2011 and beyond.

Business Segment Expectations

Credit Card Business

We expect that normal seasonal patterns will drive a decline in Domestic Card loan balances in the first quarter of 2011, and that the

first quarter of 2011 will be the low-point for Domestic Card loan balances. After the first quarter of 2011, we expect loan balances in

our Credit Card business to grow. By the end of the second quarter of 2011, we expect Domestic Card loan balances to be higher than

balances at the end of 2010. We expect further growth in the second half of 2011. We anticipate modest improvements from current

charge-off levels in 2011. We expect to add partnership loan portfolios and growth platforms, including launching the recently

announced partnership with Kohl’s Department Stores, Inc., which we expect to settle in the second quarter of 2011.