Capital One 2010 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2010 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED STATEMENTS

102

Foreclosed Property and Repossessed Assets

Foreclosed property and repossessed assets are comprised of any asset or property acquired through loan restructurings, workouts,

foreclosure proceeding or acceptance of a deed-in-lieu of foreclosure. Acquired property may include commercial and residential real

estate properties or personal property, such as autos.

Upon repossession of property acquired in satisfaction of a loan, we reclassify the loan to repossessed assets and record the acquired

property at the lower of the recorded investment in the loan or the estimated fair value of the underlying collateral less estimated

selling costs. We estimate fair values primarily based on appraisals, when available, or quoted market prices on liquid assets.

Anticipated recoveries from private mortgage insurance and government guarantees are also considered in evaluating the potential

impairment of loans at the date of transfer. When the anticipated future cash flows associated with a loan are less than its net carrying

value, a charge-off is recognized against the allowance for loan losses.

We regularly evaluate the fair value of acquired property and subsequently record at the lower of the amount recorded at acquisition or

the current fair value less estimated disposition costs. Any valuation adjustments on acquired property or gains or losses realized from

disposition of the property are reflected in non-interest expense.

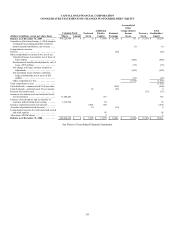

Foreclosed property and repossessed assets, which we report in our consolidated balance sheet under other assets, totaled $306 million

and $20 million, respectively, as of December 31, 2010, compared with $234 million and $24 million, respectively, as of December

31, 2009.

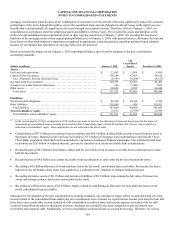

Allowance for Loan and Lease Losses

We maintain an allowance for loan and lease losses (“the allowance”) that represents management’s best estimate of incurred loan and

lease credit losses inherent in our held-for-investment portfolio as of each balance sheet date. We do not maintain an allowance for

held-for-sale loans or purchased-credit impaired loans that are performing in accordance with or better than our expectations as of the

date of acquisition, as the fair values of these loans already reflect a credit component. The allowance for loan and lease losses is

increased through the provision for loan and lease losses and reduced by net charge-offs. The provision for loan and lease losses,

which is charged to earnings, reflects credit losses we believe have been incurred and will eventually be reflected over time in our

charge-offs. Charge-offs of uncollectible amounts are deducted from the allowance and subsequent recoveries are added.

In determining the allowance for loan and lease losses, we disaggregate loans in our portfolio with similar credit risk characteristics

into portfolio segments. Management performs quarterly analysis of these portfolios to determine if impairment has occurred and to

assess the adequacy of the allowance based on historical and current trends and other factors affecting credit losses. We apply

documented systematic methodologies to separately calculate the allowance for our consumer loan and commercial loan portfolio and

for loans within each of these portfolios that we identify as individually impaired. Our allowance for loan and lease losses consists of

three components that are allocated to cover the estimated probable losses in each loan portfolio based on the results of our detailed

review and loan impairment assessment process: (1) a formula-based component for loans collectively evaluated for impairment; (2)

an asset-specific component for individually impaired loans; and (3) a component related to purchased credit-impaired loans that have

experienced significant decreases in expected cash flows subsequent to acquisition.

Our consumer loan portfolio consists of smaller-balance, homogeneous loans, divided into four primary portfolio segments: credit

card loans, auto loans, residential home loans and retail banking loans. Each of these portfolios is further divided by our business units

into pools based on common risk characteristics, such as origination year, contract type, interest rate and geography, that are

collectively evaluated for impairment. The commercial loan portfolio is primarily composed of larger-balance, non-homogeneous

loans. These loans are subject to individual reviews that result in risk ratings. In assessing the risk rating of a particular loan, among

the factors we consider are the financial condition of the borrower, geography, collateral performance, historical loss experience, and

industry-specific information that management believes is relevant in determining the occurrence of a loss event and measuring

impairment. These factors are based on an evaluation of historical and current information, and involve subjective assessment and

interpretation. Emphasizing one factor over another or considering additional factors could impact the risk rating assigned to that loan.

The formula-based component of the allowance for credit card and other consumer loans that we collectively evaluate for impairment

is based on a statistical calculation. Because of the homogenous nature of our consumer loan portfolios, the allowance is based on the

aggregated portfolio segment evaluations. The allowance is established through a process that begins with estimates of incurred losses

in each pool based upon various statistical analyses. Loss forecast models are utilized to estimate incurred losses and consider several

portfolio indicators including, but not limited to, historical loss experience, account seasoning, the value of collateral underlying

secured loans, estimated foreclosures or defaults based on observable trends, delinquencies, bankruptcy filings, unemployment and

credit bureau scores, and general economic and business trends. Management believes these factors are relevant in estimating incurred