Capital One 2010 Annual Report Download - page 194

Download and view the complete annual report

Please find page 194 of the 2010 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

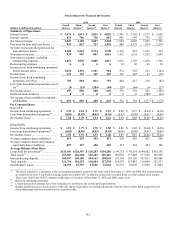

|

|

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED STATEMENTS

174

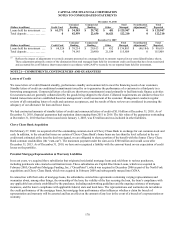

Allocation of Representation and Warranty Reserves

December 31, 2010

(Dollars in millions, except for loans sold)

Loans Sold

2005 to 2008(1)

Reserve

Liability

GSEs and Active Insured Securitizations .................................................... $ 24 $ 796

Inactive Insured Securitizations and Others .................................................. 87 20

Total ................................................................................... $ 111 $ 816

________________________

(1) Reflects, in billions, the total original principal balance of mortgage loans originated by our subsidiaries and sold to third party investors

between 2005 and 2008.

The adequacy of the reserves and the ultimate amount of losses incurred by our subsidiaries will depend on, among other things,

actual future mortgage loan performance, the actual level of future repurchase and indemnification requests (including the extent, if

any, to which Inactive Insured Securitizations and other currently inactive investors ultimately assert claims), the actual success rates

of claimants, developments in litigation, actual recoveries on the collateral and macroeconomic conditions (including unemployment

levels and housing prices).

As part of our business planning processes, we have considered various outcomes relating to the potential future representation and

warranty liabilities of our subsidiaries that are possible but do not arise to the level of being both probable and reasonably estimable

outcomes that would justify an incremental reserve accrual under applicable accounting standards. We believe that the upper end of

the reasonably possible future losses from representation and warranty claims beyond the current accrual levels, including reasonably

possible future losses relating to the US Bank Litigation and DBSP Litigation (see below), could be as high as $1.1 billion.

Notwithstanding our attempt to estimate a reasonably possible amount of loss beyond our current accrual levels based on current

information, it is possible that actual future losses will exceed both the current accrual level and the amount of reasonably possible losses

estimated here. There is still significant uncertainty as to numerous factors that contribute to ultimate liability levels, including, but not

limited to, litigation outcomes, future repurchase claims levels, ultimate repurchase success rates, and mortgage loan performance levels.

Litigation

In accordance with the current accounting standards for loss contingencies, we establish reserves for litigation related matters when it

is probable that a loss associated with a claim or proceeding has been incurred and the amount of the loss can be reasonably estimated.

Litigation claims and proceedings of all types are subject to many uncertain factors that generally cannot be predicted with assurance.

Below we provide a description of material legal proceedings and claims.

The Banks are members of Visa U.S.A., Inc. (“Visa”). As members, our subsidiary banks have indemnification obligations to Visa

with respect to final judgments and settlements of certain litigation against Visa. In 2005, a number of entities, each purporting to

represent a class of retail merchants, filed antitrust lawsuits (the “Interchange Lawsuits”) against MasterCard and Visa and several

member banks, including the Company and its subsidiaries, alleging among other things, that the defendants conspired to fix the level

of interchange fees. The complaints seek injunctive relief and civil monetary damages, which could be trebled. Separately, a number

of large merchants have asserted similar claims against Visa and MasterCard only. In October 2005, the class and merchant

Interchange lawsuits were consolidated before the U.S. District Court for the Eastern District of New York for certain purposes,

including discovery. Fact and expert discovery have closed. The parties have briefed and presented oral argument on motions to

dismiss and class certification and are awaiting decisions from the court.

In the first quarter of 2008, Visa completed an IPO of its stock. With IPO proceeds, Visa established an escrow account for the benefit of

member banks to fund certain litigation settlements and claims, including the Interchange Lawsuits. As a result, in the first quarter of

2008, we reduced our Visa-related indemnification liabilities of $91 million recorded in other liabilities with a corresponding reduction of

other non-interest expense. We made an election in accordance with the accounting guidance for fair value option for financial assets and

liabilities on the indemnification guarantee to Visa, and the fair value of the guarantee at December 31, 2010 and December 31, 2009 was

zero. In January, 2011, we entered into a MasterCard Settlement and Judgment Sharing Agreement, along with other defendant banks,

which apportions any costs and liabilities of any judgment or settlement arising from the Interchange Lawsuits.

In 2007, a number of individual plaintiffs, each purporting to represent a class of cardholders, filed antitrust lawsuits in the U.S.

District Court for the Northern District of California against several issuing banks, including the Company (the “In Re Late Fees

Litigation”). These lawsuits allege, among other things, that the defendants conspired to fix the level of late fees and over-limit fees

charged to cardholders, and that these fees are excessive. In May 2007, the cases were consolidated for all purposes, and a

consolidated amended complaint was filed alleging violations of federal statutes and state law. The amended complaint requests civil

monetary damages, which could be trebled, and injunctive relief. In November 2007, the court dismissed the amended complaint.