Capital One 2010 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2010 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

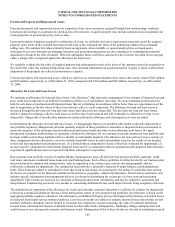

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED STATEMENTS

98

Loans Held for Investment

Loans that we have the ability and intent to hold for the foreseeable future or to maturity and loans associated with on-balance sheet

securitization transactions accounted for as secured borrowings are classified as held for investment. The substantial majority of our

loans, which include unrestricted loans and restricted loans for securitization investors, are classified as held for investment.

Credit card loans classified as held for investment are reported at their outstanding unpaid principal balance plus uncollected billed

interest and fees net of billed interest and fees deemed uncollectible. Other loans classified as held for investment, except for

purchased credit-impaired loans, are reported at amortized cost. Amortized cost is measured based on the outstanding unpaid principal

amount, net of unearned income, unamortized deferred fees and costs and charge-offs. We generally defer certain loan origination fees

and direct loan origination costs on originated loans, premiums and discounts on purchased loans and loan commitment fees and

recognize these amounts in interest income as yield adjustments over the life of the loan and/or commitment period using the level

yield interest method. Interest income is recognized on loans held for investment, other than purchased credit-impaired loans, on an

accrual basis. We establish an allowance for loan losses for probable losses inherent in our held for investment loan portfolio as of

each balance sheet date.

Cash flows related to unrestricted loans held for investment are included in cash flows from investing activities in our consolidated

statements of cash flows regardless of a subsequent change in intent. Because our securitization transactions are accounted for under

the new consolidation accounting standards as secured borrowings, the cash flows from these transactions are presented as cash flows

from financing activities rather than as cash flows from operating or investing activities in our consolidated statement of cash flows

beginning in 2010.

Loans Held for Sale

Loans that we intend to sell or for which we do not have the ability and intent to hold for the foreseeable future are classified as held

for sale. We historically classified credit card loans necessary to support new securitization transactions expected to take place in the

next three months as held for sale. Management limited the timeframe in which it believed it could reasonably estimate the amount of

existing credit card loans to support securitization transactions to three months because of the uncertainity of customer repayment

behavior and the revolving nature of credit cards.

Loans classified as held for sale are reported at the lower of amortized cost or fair value as determined on an aggregate homogeneous

portfolio basis, with any write-downs or recoveries in fair value up to the amortized cost recorded in our consolidated statements of

income as a component of other non-interest income. We recognize interest on loans held for sale classified as performing on an

accrual basis. Because loans held for sale are reported at lower of cost or fair value, an allowance for loan losses is not established for

loans held for sale. The fair value of loans held for sale is estimated based on secondary market prices for loan portfolios with similar

characteristics.

In certain circumstances, we may transfer loans to/from held for sale or held for investment based on a change in strategy. We transfer

these loans at the lower of cost or fair value on the date of transfer and establish a new cost basis upon transfer. Write-downs on loans

transferred from held for investment to held for sale are recorded as charge-offs at the time of transfer.

We execute whole loan sales with either servicing rights released to the buyer or retained. When loans are sold and the servicing rights

are released to the buyer, the gain or loss recognized on the sale is calculated based on the difference between the proceeds received

and the carrying value of the loans sold. When loans are sold and the servicing rights are retained, the fair value attributed to the

retained servicing rights impacts the gain or loss recognized on the sale. We report gains or losses on loans held for sale when realized

in other non-interest income.

Loans Acquired

All purchased loans, including loans transferred in a business combination, acquired on or after January 1, 2009, are initially recorded

at fair value at the date of acquisition based on the present value of cash flows expected to be collected. Accordingly, any related

allowance for loan losses cannot be carried over or established at acquisition. Prior to January 1, 2009, non-impaired purchased loans

aquired in a business combination were generally recorded at the present value of amounts received, determined at appropriate current

interest rates, less allowances for uncollectibility and collection costs, if necessary.

Loans acquired with evidence of credit deterioration since origination and for which it is probable at the date of acquisition that we

will not collect all contractually required principal and interest payments are considered purchased credit impaired (“PCI”) loans.

Evidence of credit deterioration as of the acquisition date may include statistics such as delinquency and accrual status; current loan-