Capital One 2012 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

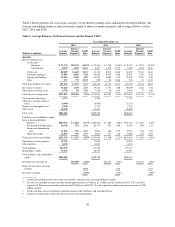

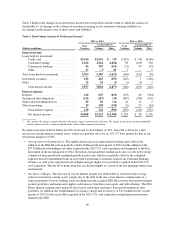

We have identified the following accounting policies as critical because they require significant judgments and

assumptions about highly complex and inherently uncertain matters and the use of reasonably different estimates

and assumptions could have a material impact on our reported results of operations or financial condition. These

critical accounting policies govern:

• Loan loss reserves

• Asset impairment

• Fair value

• Representation and warranty reserve

• Customer rewards reserve

• Income taxes

We evaluate our critical accounting estimates and judgments on an ongoing basis and update them, as necessary,

based on changing conditions. Management has reviewed and approved these critical accounting policies and has

discussed judgments and assumptions with the Audit and Risk Committee of the Board of Directors.

Loan Loss Reserves

We maintain an allowance for loan and lease losses that represents management’s estimate of incurred loan and

lease losses inherent in our held-for-investment credit card, consumer banking and commercial banking loan

portfolios as of each balance sheet date. We maintain a separate reserve for the uncollectible portion of billed

finance charges and fees on credit card loans.

Allowance for Loan and Lease Losses

We have an established process, using analytical tools, benchmarks and management judgment, to determine our

allowance for loan and lease losses. We calculate the allowance for loan and lease losses by estimating incurred

losses for segments of our loan portfolio with similar risk characteristics and record a provision for credit losses.

We build our allowance for loan and lease losses and unfunded lending commitment reserves through the

provision for credit losses. Our provision for credit losses in each period is driven by charge-offs and the level of

allowance for loan and lease losses that we determine is necessary to provide for probable loan and lease losses

incurred that are inherent in our loan portfolio as of each balance sheet date. We recorded a provision for credit

losses of $4.4 billion, $2.4 billion and $3.9 billion in 2012, 2011, and 2010, respectively. The allowance totaled

$5.2 billion as of December 31, 2012, compared with $4.3 billion as of December 31, 2011.

We review and assess our allowance methodologies and adequacy of the allowance for loan and lease losses on a

quarterly basis. Our assessment involves evaluating many factors including, but not limited to, historical loss and

recovery experience, recent trends in delinquencies and charge-offs, risk ratings, the impact of bankruptcy

filings, the value of collateral underlying secured loans, account seasoning, changes in our credit evaluation,

underwriting and collection management policies, seasonality, general economic conditions, changes in the legal

and regulatory environment and uncertainties in forecasting and modeling techniques used in estimating our

allowance for loan and lease losses. Key factors that have a significant impact on our allowance for loan and

lease losses include assumptions about unemployment rates, home prices, and the valuation of commercial

properties, consumer real estate, and autos.

Although we examine a variety of externally available data, as well as our internal loan performance data, to

determine our allowance for loan and lease losses, our estimation process is subject to risks and uncertainties,

including a reliance on historical loss and trend information that may not be representative of current conditions

and indicative of future performance. Accordingly, our actual credit loss experience may not be in line with our

expectations. For example, excluding the initial allowance build of $1.2 billion established for certain loans

related to the 2012 U.S. card acquisition, we recorded an allowance release of $294 million in 2012, attributable

to a significant improvement in underlying credit performance trends in our Commercial Banking business.

Similarly, as a result of improving credit performance trends during 2011, charge-offs began to decrease across

all of our business segments, and we recorded a significant allowance release of $1.4 billion in 2011.

50