Capital One 2012 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

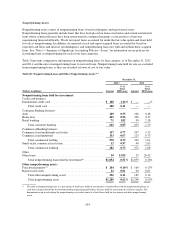

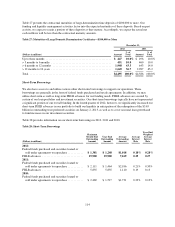

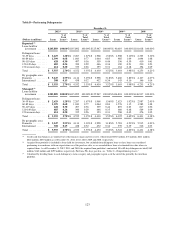

Table 27 presents the contractual maturities of large-denomination time deposits of $100,000 or more. Our

funding and liquidity management activities factor into the expected maturities of these deposits. Based on past

activity, we expect to retain a portion of these deposits as they mature. Accordingly, we expect the actual net

cash outflows will be less than the contractual maturity amounts.

Table 27: Maturities of Large Domestic Denomination Certificates—$100,000 or More

December 31,

2012 2011

(Dollars in millions) Amount

% of

Total Amount

% of

Total

Up to three months .............................................. $ 447 10.0% $ 496 10.8%

> 3 months to 6 months .......................................... 451 10.0 460 10.0

> 6 months to 12 months ......................................... 1,948 43.3 643 14.0

> 12 months to 10 years .......................................... 1,649 36.7 2,987 65.2

Total ......................................................... $4,495 100.0% $4,586 100.0%

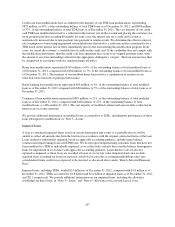

Short-Term Borrowings

We also have access to and utilize various other short-term borrowings to support our operations. These

borrowings are generally in the form of federal funds purchased and resale agreements. In addition, we may

utilize short-term as well as long-term FHLB advances for our funding needs. FHLB advances are secured by

certain of our loan portfolios and investment securities. Our short-term borrowings typically have not represented

a significant portion of our overall funding. In the fourth quarter of 2012, however, we significantly increased our

short-term FHLB advances in our portfolio to build our liquidity in anticipation of the redemption of the $3.65

billion in outstanding trust preferred securities on January 2, 2013, as well as to cover seasonal loan growth and

to fund increases in our investment securities.

Table 28 provides information on our short-term borrowings in 2012, 2011 and 2010.

Table 28: Short-Term Borrowings

(Dollars in millions)

Maximum

Month-End

Outstanding

Amount

Year-End

Outstanding

Amount

Average

Outstanding

Amount

Average

Interest

Rate

Year-End

Weighted

Average

Interest

Rate

2012:

Federal funds purchased and securities loaned or

sold under agreements to repurchase ........... $ 1,381 $ 1,248 $1,018 0.18% 0.28%

FHLB advances ............................. 19,900 19,900 7,169 0.25 0.27

2011:

Federal funds purchased and securities loaned or

sold under agreements to repurchase ........... $ 2,111 $ 1,464 $2,186 0.21% 0.30%

FHLB advances ............................. 5,835 5,835 1,110 0.19 0.13

2010:

Federal funds purchased and securities loaned or

sold under agreements to repurchase ........... $ 2,469 $ 1,517 $1,731 0.23% 0.13%

114