Capital One 2012 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

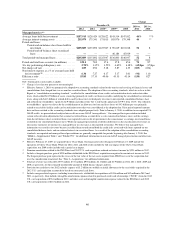

|

|

Change

December 31, 2010 vs.

2011

2011 vs.

20102012 2011 2010(1) 2009(2) 2008

Managed metrics(26)

Average loans held for investment ............. $187,915 $128,424 $128,622 $143,514 $147,812 46% **%

Average interest-earning assets ............... 255,079 175,341 175,815 185,976 179,348 46 **

Period-end loans:

Period-end on-balance sheet loans held for

investment .......................... $205,889 $135,892 $125,947 $ 90,619 $101,018 52 8

Period-end off-balance sheet securitized

loans .............................. —— — 46,184 45,919 ——

Total period-end managed loans ............... $205,889 $135,892 $125,947 $136,803 $146,937 52 8

Period-end total loan accounts (in millions) ...... 122.1 70.0 37.4 37.8 45.4 74 87

30+ day performing delinquency rate ........... 2.70% 3.35% 3.52% 4.62% 4.38% (65)bps (17)bps

Net charge-off rate ......................... 1.89 2.94 5.18 5.87 4.35 (105) (224)

Non-interest expense as a % of average loans held

for investment(20) ......................... 6.36 7.27 6.17 5.17 5.01 (91) 110

Efficiency ratio ............................ 55.83 57.33 49.06 43.35 43.14 (150) 827

N/A—Information is not readily available.

** Change is less than one percent or not meaningful.

(1) Effective January 1, 2010, we prospectively adopted two accounting standards related to the transfer and servicing of financial assets and

consolidations that changed how we account for securitized loans. The adoption of these accounting standards, which we refer o in this

Report as “consolidation accounting standards,” resulted in the consolidation of our credit card securitization trusts and certain other

trusts, which added $41.9 billion of assets, consisting primarily of credit card loan receivables underlying the consolidated securitization

trusts, along with $44.3 billion of related debt issued by these trusts to third-party investors to our reported consolidated balance sheet

and reduced our stockholders’ equity by $2.9 billion and reduced our Tier 1 risk-based capital ratio to 9.9% from 13.8%. The reduction

to stockholders’ equity was driven by the establishment of an allowance for loan and lease losses of $4.3 billion (pre-tax) primarily

related to receivables held in credit card securitization trusts that were consolidated at the adoption date. Prior period reported amounts

have not been restated as the accounting standards were adopted prospectively. Prior to January 1, 2010, in addition to our reported U.S.

GAAP results, we presented and analyzed our results on a non-GAAP “managed basis.” Our managed-basis presentation included

certain reclassification adjustments that assumed securitized loans accounted for as sales remained on balance sheet, and the earnings

from the off-balance sheet securitized loans were reported in our results of operations in the same manner as earnings on retained loans

recorded on our consolidated balance sheet. While our managed presentation resulted in differences in the classification of revenues in

our income statement, net income on a managed basis was the same as our reported net income. We believe this managed-basis

information was useful to investors because it enabled them to understand both the credit risks associated with loans reported on our

consolidated balance sheets and our retained interests in securitized loans. As a result of the adoption of the consolidation accounting

standards, our reported and managed based presentations are generally comparable for periods beginning after January 1, 2010. See

“MD&A—Supplemental Tables” and “Exhibit 99.1” for additional information on our non-GAAP managed presentation and other non-

GAAP measures.

(2) Effective February 27, 2009, we acquired Chevy Chase Bank. Our financial results subsequent to February 27, 2009 include the

operations of Chevy Chase Bank. While our 2012, 2011 and 2010 results include the full year impact of the Chevy Chase Bank

acquisition, our 2009 results include only a partial year impact.

(3) Premium amortization related to the ING Direct and 2012 U.S. card acquisitions reduced net interest income by $391 million in 2012.

(4) Includes a bargain purchase gain of $594 million attributable to the ING Direct acquisition recognized in non-interest income in 2012.

The bargain purchase gain represents the excess of the fair value of the net assets acquired from ING Direct as of the acquisition date

over the consideration transferred. See “Note 2—Acquisitions” for additional information.

(5) Total net revenue was reduced by $937 million, $371 million, $950 million, $2.1 billion and $1.9 billion in 2012, 2011, 2010, 2009 and

2008, respectively, for the estimated uncollectible amount of billed finance charges and fees.

(6) Provision for credit losses for 2012 includes expense of $1.2 billion to establish an initial allowance for the receivables acquired in the

2012 U.S. card acquisition accounted for based on contractual cash flows.

(7) Includes merger-related expenses, including transaction costs, attributable to acquisitions of $336 million and $45 million in 2012 and

2011, respectively. Also includes intangible amortization expense related to purchased credit card relationships (“PCCR”) from the 2012

U.S. card acquisition of $334 million in 2012, and other asset and intangible amortization expense related to the ING Direct and 2012

U.S. card acquisitions of $147 million in 2012.

40