Capital One 2012 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

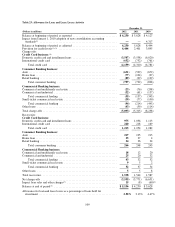

(1) Includes an adjustment of $53 million made in the second quarter of 2010 for the impact as of January 1, 2010 of impairment on

consolidated loans accounted for as TDRs.

(2) The total provision for credit losses reported in our consolidated statements of income of $4.4 billion, $2.4 billion and $3.9 billion in

2012, 2011 and 2010, respectively, consists of a provision for loan and lease losses and a provision for unfunded lending commitments.

The provision for credit losses reported in the above table relates only to the provision for loan and lease losses. It does not include the

negative provision for unfunded lending commitments of $35 million in 2012 and the provision for unfunded lending commitments of

$12 million in 2011 and 2010, respectively.

(3) Includes foreign translation adjustments of $15 million and $8 million in 2012 and 2011, respectively.

(4) Includes a reduction in our allowance for loan and lease losses of $73 million in 2010 attributable to the sale of certain interest-only

option-adjustable rate mortgage (“option-ARM”) bonds and the deconsolidation of securitization trusts related to CCB.

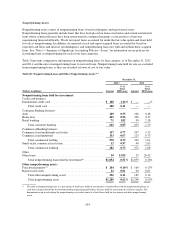

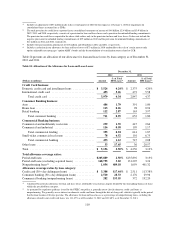

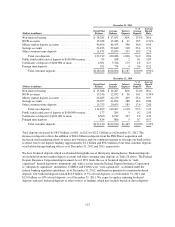

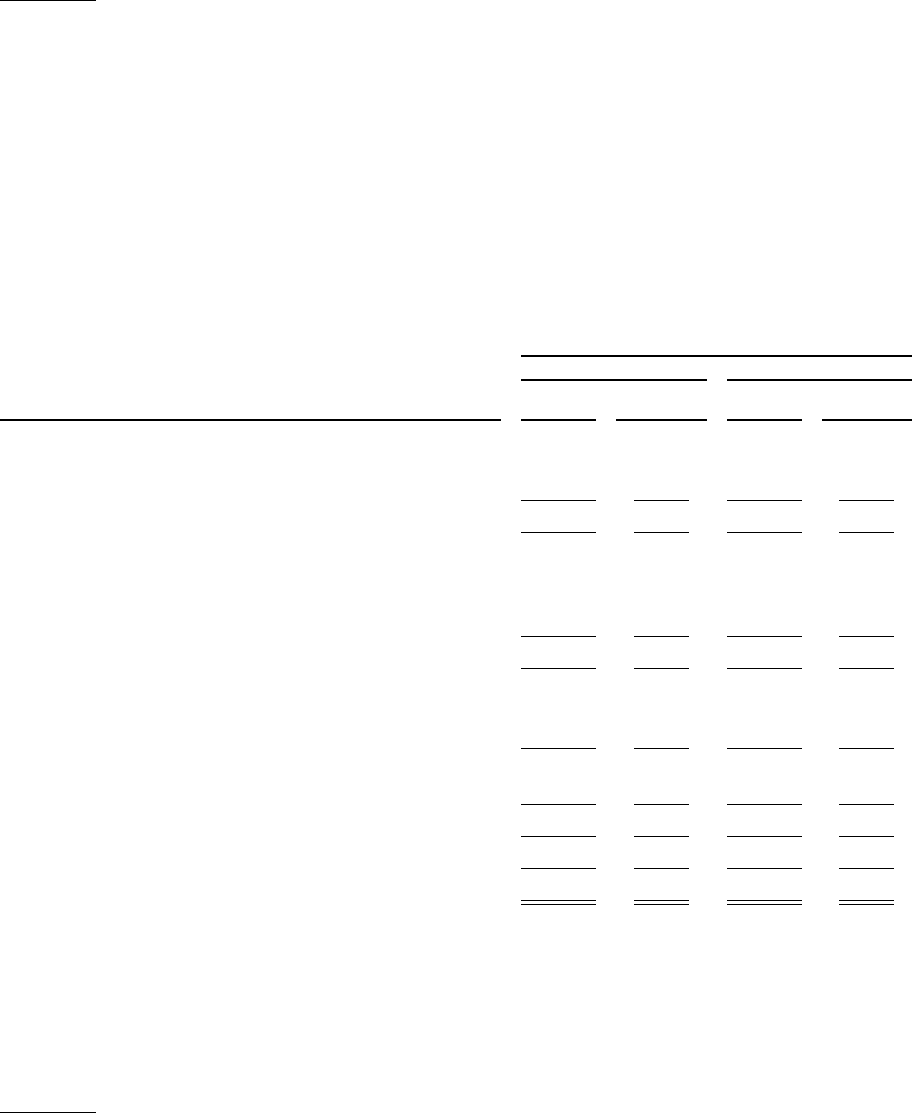

Table 24 presents an allocation of our allowance for loan and lease losses by loan category as of December 31,

2012 and 2011.

Table 24: Allocation of the Allowance for Loan and Lease Losses

December 31,

2012 2011

(Dollars in millions) Amount

% of Total

HFI Loans(1) Amount

% of Total

HFI Loans(1)

Credit Card business:

Domestic credit card and installment loans ............... $ 3,526 4.24% $ 2,375 4.20%

International credit card .............................. 453 5.26 472 5.58

Total credit card ................................ 3,979 4.34 2,847 4.37

Consumer Banking business:

Auto .............................................. 486 1.79 391 1.80

Home loan ......................................... 113 0.26 98 0.94

Retail banking ...................................... 112 2.87 163 3.97

Total consumer banking .......................... 711 0.95 652 1.80

Commercial Banking business:

Commercial and multifamily real estate .................. 239 1.35 415 2.64

Commercial and industrial ............................ 116 0.58 199 1.17

Total commercial lending ......................... 355 0.94 614 1.87

Small-ticket commercial real estate ..................... 78 6.52 101 6.75

Total commercial banking ........................ 433 1.12 715 2.08

Other loans ........................................ 33 17.65 36 20.57

Total ............................................. $ 5,156 2.50% $ 4,250 3.13%

Total allowance coverage ratios:

Period-end loans .................................... $205,889 2.50% $135,892 3.13%

Period-end loans (excluding acquired loans) .............. 168,755 3.02 131,207 3.24

Nonperforming loans(2) ............................... 1,054 489.18 1,059 401.32

Allowance coverage ratios by loan category:

Credit card (30 + day delinquent loans) .................. $ 3,388 117.44% $ 2,511 113.38%

Consumer banking (30 + day delinquent loans) ............ 2,510 28.33 2,176 29.96

Commercial banking (nonperforming loans) .............. 282 153.55 372 192.20

(1) Calculated based on the allowance for loan and lease losses attributable to each loan category divided by the outstanding balance of loans

within the specified loan category.

(2) As permitted by regulatory guidance issued by the FFIEC, our policy is generally not to classify domestic credit card loans as

nonperforming. We generally accrue interest on domestic credit card loans through the date of charge-off, which is typically in the period

that the loan becomes 180 days past due. The allowance for loan and lease losses as a percentage of nonperforming loans, excluding the

allowance related to our credit card loans, was 111.67% as of December 31, 2012 and 132.48% as of December 31, 2011.

110