Capital One 2012 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

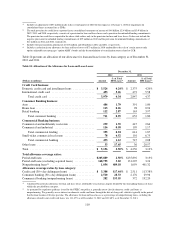

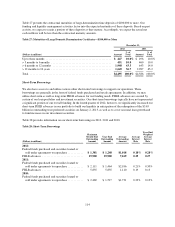

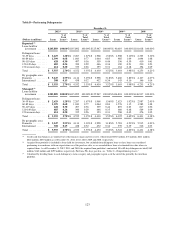

Table 32: Interest Rate Sensitivity Analysis

December 31, 2011

(Dollars in millions)

December 31,

2012

Excluding ING

Direct Swaps(1)

Including ING

Direct Swaps

Previous methodology:

Impact on adjusted projected base-line net interest income:

+ 200 basis points .................................... 1.3% 1.2% 13.7%

-50 basis points ...................................... (0.9) (0.5) (3.9)

Impact on economic value of equity:

+ 200 basis points .................................... (3.1) (1.0) 3.2

-50 basis points ...................................... (1.4) (0.4) (1.5)

Revised methodology:

Impact on adjusted projected base-line net interest income:

+ 200 basis points .................................... 2.7% NA NA

-50 basis points ...................................... (1.7) NA NA

Impact on economic value of equity:

+ 200 basis points .................................... (3.1) (1.0) 3.2

-50 basis points ...................................... (1.4) (0.4) (1.5)

NA Comparable information for December 31, 2011 is not available.

(1) Calculated excluding the impact of the interest rate swap transactions of approximately $24.8 billion entered into to mitigate some of the

interest rate risk related to the ING Direct acquisition.

Because of the large but temporary impact of the ING Direct-related swap transactions on our standard interest

rate risk reporting measures, we expanded our standard interest rate sensitivity analysis to present our interest

rate risk measures as of December 31, 2011 both with and without the impact of the $24.8 billion of interest rate

swaps described above. This presentation highlights changes in our core interest rate risk profile and the

incremental impact of the ING Direct-related swaps on our core profile over the time period that the swaps

remained outstanding. Excluding the $24.8 billion swap transactions, our interest rate sensitivity measures reflect

that we became modestly more asset sensitive between December 31, 2011 and December 31, 2012. Our

projected net interest income and economic value of equity sensitivity measures, both including and excluding

the impact of the ING Direct related swap transactions, were within our prescribed asset/liability policy limits as

of December 31, 2012 and 2011. Additionally, the new earnings sensitivity method results in a slightly higher

asset sensitivity position compared to the previous method, resulting from a higher forecasted volume of rate

sensitive assets versus rate sensitive liabilities in addition to the impact of an instantaneous rate shock.

Limitations of Market Risk Measures

The interest rate risk models that we use in deriving these measures incorporate contractual information,

internally-developed assumptions and proprietary modeling methodologies, which project borrower and deposit

behavior patterns in certain interest rate environments. Other market inputs, such as interest rates, market prices

and interest rate volatility, are also critical components of our interest rate risk measures. We regularly evaluate,

update and enhance these assumptions, models and analytical tools as we believe appropriate to reflect our best

assessment of the market environment and the expected behavior patterns of our existing assets and liabilities.

There are inherent limitations in any methodology used to estimate the exposure to changes in market interest

rates. The above sensitivity analyses contemplate only certain movements in interest rates and are performed at a

particular point in time based on the existing balance sheet and, in some cases, expected future business growth

and funding mix assumptions. The strategic actions that management may take to manage our balance sheet may

differ from our projections, which could cause our actual earnings and economic value of equity sensitivities to

differ from the above sensitivity analyses.

120