Capital One 2012 Annual Report Download - page 280

Download and view the complete annual report

Please find page 280 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

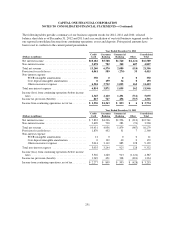

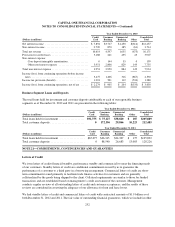

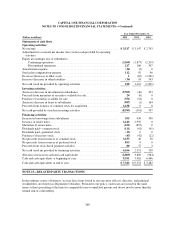

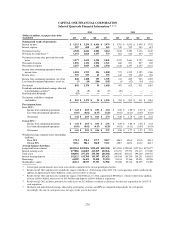

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

not their antitrust conspiracy claims. In June 2009, the Ninth Circuit Court of Appeals stayed the matter pending

the bankruptcy proceedings of one of the defendant financial institutions. After numerous stays since 2009, the

Ninth Circuit entered an order lifting the stay on August 29, 2012, and will now hear the appeal.

Credit Card Interest Rate Litigation

In July 2010, the U.S. Court of Appeals for the Ninth Circuit reversed a dismissal entered in favor of COBNA in

Rubio v. Capital One Bank, which was filed in the U.S. District Court for the Central District of California in

2007. The plaintiff in Rubio alleges in a putative class action that COBNA breached its contractual obligations

and violated the Truth In Lending Act (the “TILA”) and the California Unfair Competition Law (“UCL”) when it

raised interest rates on certain credit card accounts. In May, 2012, the parties agreed to a California-only

settlement for a non-material amount, and the Court stayed the case for all purposes except for approval of the

settlement. On November 29, 2012, the court granted preliminary court approval of the class settlement and set a

hearing on final approval of the class settlement for April 1, 2013.

The Capital One Bank Credit Card Interest Rate Multi-district Litigation matter was created as a result of a June

2010 transfer order issued by the United States Judicial Panel on Multi-district Litigation (“MDL”), which

consolidated for pretrial proceedings in the U.S. District Court for the Northern District of Georgia two pending

putative class actions against COBNA—Nancy Mancuso, et al. v. Capital One Bank (USA), N.A., et al., (E.D.

Virginia); and Kevin S. Barker, et al. v. Capital One Bank (USA), N.A., (N.D. Georgia), A third action, Jennifer

L. Kolkowski v. Capital One Bank (USA), N.A., (C.D. California) was subsequently transferred into the MDL.

On August 2, 2010, the plaintiffs in the MDL filed a Consolidated Amended Complaint. The Consolidated

Amended Complaint alleges in a putative class action that COBNA breached its contractual obligations, and

violated the TILA, the California Consumers Legal Remedies Act, the UCL, the California False Advertising

Act, the New Jersey Consumer Fraud Act, and the Kansas Consumer Protection Act when it raised interest rates

on certain credit card accounts. The MDL plaintiffs seek statutory damages, restitution, attorney’s fees and an

injunction against future rate increases. Fact discovery is now closed. On August 8, 2011, Capital One filed a

motion for summary judgment, which remains pending with the court. As a result of the settlement in Rubio v.

Capital One Bank, the California-based UCL and TILA claims in the MDL are extinguished.

Mortgage Repurchase Litigation

On February 5, 2009, GreenPoint was named as a defendant in a lawsuit commenced in the New York County

Supreme Court , by U.S. Bank, N. A., Syncora Guarantee Inc. (formerly known as XL Capital Assurance Inc.)

and CIFG Assurance North America, Inc. (the “U.S. Bank Litigation”). Plaintiffs allege, among other things, that

GreenPoint breached certain representations and warranties in two contracts pursuant to which GreenPoint sold

approximately 30,000 mortgage loans having an aggregate original principal balance of approximately $1.8

billion to a purchaser that ultimately transferred most of these mortgage loans to a securitization trust. Some of

the securities issued by the trust were insured by two of the plaintiffs. Plaintiffs seek unspecified damages and an

order compelling GreenPoint to repurchase the entire portfolio of 30,000 mortgage loans based on alleged

breaches of representations and warranties relating to a limited sampling of loans in the portfolio, or,

alternatively, the repurchase of specific mortgage loans to which the alleged breaches of representations and

warranties relate. On March 3, 2010, the Court granted GreenPoint’s motion to dismiss with respect to plaintiffs

Syncora and CIFG and denied the motion with respect to U.S. Bank. GreenPoint subsequently answered the

complaint with respect to U.S. Bank, denying the allegations, and filed a counterclaim against U.S. Bank alleging

breach of covenant of good faith and fair dealing. On February 28, 2012, the Court denied plaintiffs’ motion for

leave to file an amended complaint and dismissed Syncora and CIFG from the case. Syncora and CIFG have

appealed. Discovery between U.S. Bank and GreenPoint has been ongoing since January, 2011. As noted above,

261