Capital One 2012 Annual Report Download - page 276

Download and view the complete annual report

Please find page 276 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Moreover, for the potential GSE repurchase liability remaining after bulk settlements, we have established a

negotiation pattern whereby the GSEs and our subsidiaries continually negotiate around individual repurchase

requests, leading to the GSEs rescinding some repurchase requests and our subsidiaries agreeing in some cases to

repurchase some loans or make the GSEs whole with respect to losses. Our lifetime representation and warranty

reserves with respect to GSE repurchase liability remaining after bulk settlements are grounded in this history.

One of our subsidiaries entered into a bulk settlement with a GSE to resolve present and future repurchase claims

in the first quarter of 2012, and our reserves allocated to the GSE segment reflect the amount of that settlement.

For the $16 billion original principal balance in Active Insured Securitizations, our reserving approach also

reflects our historical interaction with monoline bond insurers around repurchase requests. Typically, monoline

bond insurers allege a very high repurchase rate with respect to the mortgage loans in the Active Insured

Securitization category. In response to these repurchase requests, our subsidiaries typically request information

from the monoline bond insurers demonstrating that the contractual requirements around a valid repurchase

request have been satisfied. In response to these requests for supporting documentation, monoline bond insurers

typically initiate litigation. Accordingly, our reserves within the Active Insured Securitization segment are not

based upon the historical repurchase rate with monoline bond insurers, but rather upon the expected resolution of

litigation with the monoline bond insurers. Every bond insurer within this category is pursuing a substantially

similar litigation strategy either through active or probable litigation. Accordingly, our representation and

warranty reserves for this category are litigation reserves. In establishing litigation reserves for this category, we

consider current and future losses inherent within the securitization and apply legal judgment to the anticipated

factual and legal record to estimate the lifetime legal liability for each securitization. Our estimated legal liability

for each securitization within this category assumes that we will be responsible for only a portion of the losses

inherent in each securitization. Our litigation reserves with respect to the U.S. Bank Litigation, the DBSP

Litigation, and the Ambac Litigation, in each case as referenced below, are contained within the Active Insured

Securitization reserve category. Further, our litigation reserves with respect to indemnification risks from certain

representation and warranty lawsuits brought by monoline bond insurers against third-party securitizations

sponsors, where one of our subsidiaries provided some or all of the mortgage collateral within the securitization

but is not a defendant in the litigation, are also contained within this category.

For the $4 billion original principal balance of mortgage loans in the Inactive Insured Securitizations category

and the $80 billion original principal balance of mortgage loans in the Uninsured Securitizations and other whole

loan sales categories, we establish reserves by relying on our historical activity and repurchase rates to estimate

repurchase liabilities over the next twelve (12) months. We do not believe we can estimate repurchase liability

for these categories for a period longer than twelve (12) months because of the relatively irregular nature of

repurchase activity within these categories. Some Uninsured Securitization investors from this category who

have not made repurchase requests or filed representation and warranty lawsuits are currently suing investment

banks and securitization sponsors under federal and/or state securities laws. Although we face some direct and

indirect indemnity risks from these litigations, we generally have not established reserves with respect to these

indemnity risks because we do not consider them to be both probable and reasonably estimable liabilities.

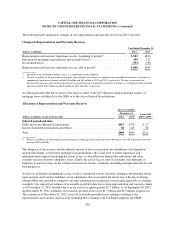

The aggregate reserves for all three subsidiaries totaled $899 million as of December 31, 2012, compared with

$943 million as of December 31, 2011. We recorded a total provision for mortgage representation and warranty

losses for our representation and warranty repurchase exposure of $349 million in 2012, which was primarily

driven by updated estimates of anticipated outcomes from various litigation and threatened litigation in the

insured securitization segment based on relevant factual and legal developments and an increased reserve

associated with a settlement in the first quarter of 2012 between a subsidiary and a GSE to resolve present and

future repurchase claims. The decrease in the reserve in 2012 was driven primarily by the settlement of claims.

During 2012, we had settlements of repurchase requests totaling $393 million that were charged against the

reserve.

257