Capital One 2012 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

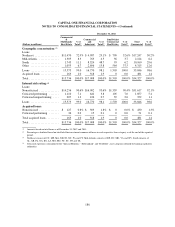

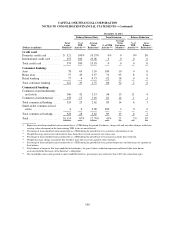

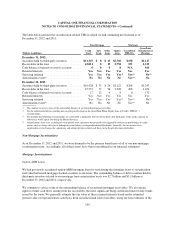

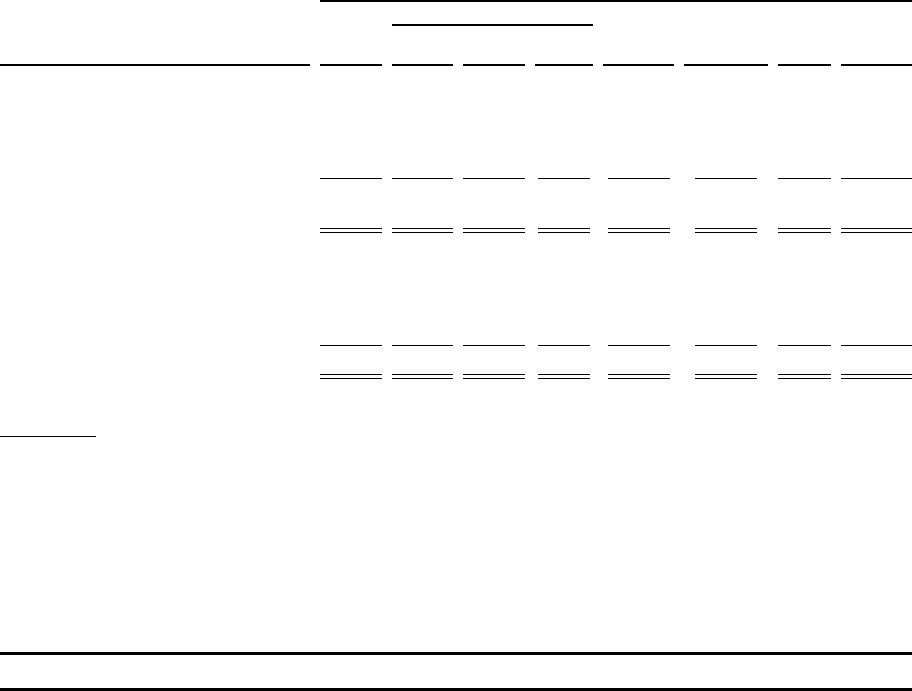

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

December 31, 2011

Consumer

(Dollars in millions)

Credit

Card Auto

Home

Loan

Retail

Banking

Total

Consumer Commercial Other Total

Allowance for loan and lease losses by

impairment methodology:

Collectively evaluated(1) ............. $ 2,494 $ 383 $ 65 $ 150 $ 598 $ 638 $ 36 $ 3,766

Asset-specific(2) ................... 353 8 10 12 30 75 0 458

Acquired loans(3) .................. 0 0 23 1 24 2 0 26

Total allowance for loan and lease

losses ......................... $ 2,847 $ 391 $ 98 $ 163 $ 652 $ 715 $ 36 $ 4,250

Held-for-investment loans by

impairment methodology:

Collectively evaluated(1) ............. $64,177 $21,674 $ 6,217 $3,968 $31,859 $33,198 $ 175 $129,409

Asset-specific(2) ................... 898 58 104 90 252 648 0 1,798

Acquired loans(3) .................. 0 47 4,112 45 4,204 481 0 4,685

Total held-for-investment loans ....... $65,075 $21,779 $10,433 $4,103 $36,315 $34,327 $ 175 $135,892

Allowance as a percentage of period-

end held-for-investment loans ...... 4.37% 1.80% 0.94% 3.97% 1.80% 2.08% 20.57% 3.13%

(1) The collectively evaluated component of the allowance for credit card and other consumer loans that we collectively evaluate for

impairment is based on a statistical calculation. The collectively evaluated component of the allowance for commercial loans, which we

collectively evaluate for impairment, is based on our historical loss experience for loans with similar characteristics and consideration of

credit quality supplemented by management judgment and interpretation.

(2) The asset-specific component of the allowance for smaller-balance impaired loans is calculated on a pool basis using historical loss

experience for the respective class of assets. The asset-specific component of the allowance for larger-balance commercial loans is

individually calculated for each loan.

(3) The acquired loans component of the allowance is accounted for based on expected cash flows. See “Note 5 – Loans” for details on these

loans.

NOTE 7—VARIABLE INTEREST ENTITIES AND SECURITIZATIONS

In the normal course of business, we enter into various types of transactions with entities that are considered to

be VIEs. Historically, our primary involvement with VIEs has been related to our securitization transactions in

which we transferred assets from our balance sheet to securitization trusts. These securitization trusts typically

meet the definition of a VIE. We have generally securitized credit card loans, auto loans, home loans and

installment loans, which have provided a source of funding for us and as a means of transferring a certain portion

of the economic risk of the loans or debt securities to third parties.

The entity that has a controlling financial interest in a VIE is referred to as the primary beneficiary and is

required to consolidate the VIE. The vast majority of the VIEs in which we are involved have been consolidated

in our financial statements.

Summary of Consolidated and Unconsolidated VIEs

The table below presents a summary of VIEs, aggregated based on VIEs with similar characteristics, in which we

had continuing involvement or held a variable interest as of December 31, 2012 and 2011. We separately present

information for consolidated and unconsolidated VIEs.

196