Capital One 2012 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

credit losses to properly recognize an estimate of incurred losses on the existing principal balances, which

represents a portion of the total amounts not expected to be collected described above. In 2012, we recorded a

provision for credit losses of $1.2 billion to establish an initial allowance primarily related to these loans. The

allowance was calculated using the same methodology utilized for determining the allowance for our existing

credit card portfolio. The provision for credit losses of $1.2 billion related to these loans is included in the total

provision for credit losses of $4.4 billion recorded in 2012.

Excluded from the amounts above are revolving loans acquired in the 2012 U.S. card acquisition with a fair value

of $471 million that we designated as held for sale at acquisition. We closed on the sale of these receivables early

in the third quarter of 2012.

See “Note 1—Summary of Significant Accounting Policies—Loans” for additional information on our

accounting for loans, including purchased loans. See “Note 5—Loans” and “Note 6—Allowance for Loan and

Lease Losses” for additional information on the credit quality of our loan portfolio.

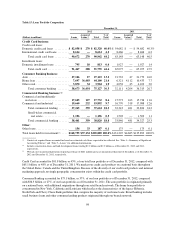

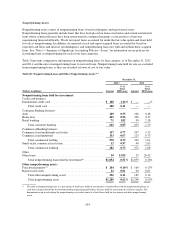

Loan Maturity Profile

Table 16 presents the maturities of loans in our held-for-investment portfolio as of December 31, 2012.

Table 16: Loan Maturity Schedule

December 31, 2012

(Dollars in millions)

Due Up to

1 Year

> 1 Year

to 5 Years > 5 Years Total

Fixed rate:

Credit card(1) (2) ...................................... $ 3,357 $16,699 $ 45 $ 20,101

Consumer .......................................... 762 22,249 12,927 35,938

Commercial ........................................ 1,288 5,880 5,887 13,055

Other .............................................. — — 35 35

Total fixed-rate loans ..................................... 5,407 44,828 18,894 69,129

Variable rate:

Credit card(1) ........................................ 71,639 15 — 71,654

Consumer .......................................... 7,176 833 31,180 39,189

Commercial ........................................ 23,350 2,265 150 25,765

Other .............................................. 128 15 9 152

Total variable-rate loans ................................... 102,293 3,128 31,339 136,760

Total loans ............................................. $107,700 $47,956 $50,233 $205,889

(1) Due to the revolving nature of credit card loans, we report all variable-rate credit card loans as due in one year or less. We report fixed-

rate credit card loans with introductory rates that expire after a certain period of time as due in one year or less. We assume that our

remaining fixed-rate credit card loans will mature within one to three years.

(2) Includes installment loans of $813 million as of December 31, 2012.

Credit Risk Measurement

We closely monitor economic conditions and loan performance trends to assess and manage our exposure to

credit risk. Key metrics we track in evaluating the credit quality of our loan portfolio include delinquency and

nonperforming asset rates, as well as charge-off rates and our internal risk ratings of larger balance, commercial

loans. Trends in delinquency rates are a primary indicator of credit risk within our consumer loan portfolios, as

changes in delinquency rate provide an early warning of changes in credit losses. The primary indicator of credit

risk in our commercial loan portfolios is risk ratings. Because we generally classify loans that have been

100