Capital One 2012 Annual Report Download - page 278

Download and view the complete annual report

Please find page 278 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

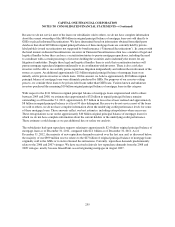

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Litigation, the Ambac Litigation, the FHFA Litigation, and the FHLB of Boston Litigation. The increase since

September 30, 2012 is attributable to updated assessments of reasonably possible future losses based primarily on

increased securitization trustee activity and adverse legal developments in litigation in which our subsidiaries are

not parties, but which could influence litigation in which our subsidiaries are parties, in each case occurring after

the end of 2012. Notwithstanding our ongoing attempts to estimate a reasonably possible amount of future loss

beyond our current accrual levels based on current information, it is possible that actual future losses will exceed

both the current accrual level and our current estimate of the amount of reasonably possible losses. This estimate

involves considerable judgment, and reflects that there is still significant uncertainty regarding the numerous

factors that may impact the ultimate loss levels, including, but not limited to, anticipated litigation outcomes,

future repurchase and indemnification claim levels, ultimate repurchase and indemnification rates, future

mortgage loan performance levels, actual recoveries on the collateral and macroeconomic conditions (including

unemployment levels and housing prices). In light of the significant uncertainty as to the ultimate liability our

subsidiaries may incur from these matters, an adverse outcome in one or more of these matters could be material

to our results of operations or cash flows for any particular reporting period.

Litigation

In accordance with the current accounting standards for loss contingencies, we establish reserves for litigation

related matters when it is probable that a loss associated with a claim or proceeding has been incurred and the

amount of the loss can be reasonably estimated. Litigation claims and proceedings of all types are subject to

many uncertain factors that generally cannot be predicted with assurance. Below we provide a description of

material legal proceedings and claims.

For some of the matters disclosed below, we are able to determine estimates of potential future outcomes that are

not probable and reasonably estimable outcomes justifying either the establishment of a reserve or an incremental

reserve build, but which are reasonably possible outcomes. For other disclosed matters, such an estimate is not

possible at this time. For those matters below where an estimate is possible, excluding the reasonably possible

future losses relating to the U.S. Bank Litigation, the DBSP Litigation, the Ambac Litigation, the FHFA Litigation,

and the FHLB of Boston Litigation because reasonably possible losses with respect to those litigations are included

within the reasonably possible representation and warranty liabilities discussed above, management currently

estimates the reasonably possible future losses could be approximately $150 million. Notwithstanding our attempt

to estimate a reasonably possible range of loss beyond our current accrual levels for some litigation matters based

on current information, it is possible that actual future losses will exceed both the current accrual level and the range

of reasonably possible losses disclosed here. Given the inherent uncertainties involved in these matters, and the very

large or indeterminate damages sought in some of these matters, there is significant uncertainty as to the ultimate

liability we may incur from these litigation matters and an adverse outcome in one or more of these matters could be

material to our results of operations or cash flows for any particular reporting period.

Interchange Litigation

In 2005, a number of entities, each purporting to represent a class of retail merchants, filed antitrust lawsuits (the

“Interchange Lawsuits”) against MasterCard and Visa and several member banks, including our subsidiaries and

us, alleging among other things, that the defendants conspired to fix the level of interchange fees. The complaints

seek injunctive relief and civil monetary damages, which could be trebled. Separately, a number of large

merchants have asserted similar claims against Visa and MasterCard only. In October 2005, the class and

merchant Interchange Lawsuits were consolidated before the U.S. District Court for the Eastern District of New

York for certain purposes, including discovery. On July 13, 2012, the parties executed and filed with the court a

Memorandum of Understanding agreeing to resolve the litigation on certain terms set forth in a settlement

259