Capital One 2012 Annual Report Download - page 213

Download and view the complete annual report

Please find page 213 of the 2012 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

|

|

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

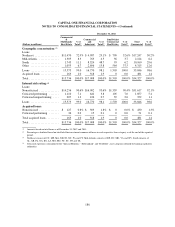

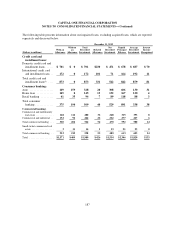

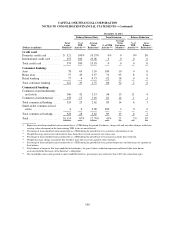

(4) Represents changes in accretable yields for those pools with reductions that are driven primarily by changes in actual and estimated

prepayments.

Unfunded Lending Commitments

We manage the potential risk in credit commitments by limiting the total amount of arrangements, both by

individual customer and in total, by monitoring the size and maturity structure of these portfolios and by applying

the same credit standards for all of our credit activities. Unused credit card lines available to our customers

totaled $298.9 billion and $206.0 billion as of December 31, 2012 and 2011, respectively. While these amounts

represented the total available unused credit card lines, we have not experienced and do not anticipate that all of

our customers will access their entire available line at any given point in time.

In addition to available unused credit card lines, we enter into commitments to extend credit that are legally

binding conditional agreements having fixed expirations or termination dates and specified interest rates and

purposes. These commitments generally require customers to maintain certain credit standards. Collateral

requirements and loan-to-value ratios are the same as those for funded transactions and are established based on

management’s credit assessment of the customer. These commitments may expire without being drawn upon;

therefore, the total commitment amount does not necessarily represent future funding requirements. The

outstanding unfunded commitments to extend credit, other than credit card lines, were approximately

$17.5 billion and $14.8 billion as of December, 2012 and 2011, respectively.

We maintain a reserve for unfunded loan commitments and letters of credit to absorb estimated probable losses

related to these unfunded credit facilities in other liabilities on our consolidated balance sheets. Our reserve for

unfunded loan commitments and letters of credit was $35 million and $66 million as of December 31, 2012 and

2011, respectively. See “Note 6—Allowance for Loan and Lease Losses” below for additional information.

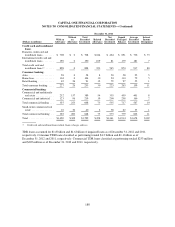

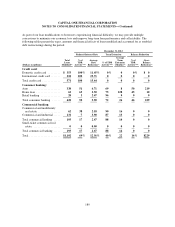

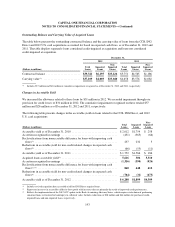

NOTE 6—ALLOWANCE FOR LOAN AND LEASE LOSSES

We maintain an allowance for loan and lease losses that represents management’s best estimate of incurred loan

and lease losses inherent in our held-for-investment portfolio as of each balance sheet date. We do not maintain

an allowance for held-for-sale loans or acquired loans that are performing, in accordance with or better than our

expectations, as of the date of acquisition, as the fair value of these loans already reflect a credit component.

In addition to the allowance for loan and lease losses, we also estimate probable losses related to unfunded lending

commitments, such as letters of credit, financial guarantees, and binding unfunded loan commitments. The provision

for unfunded lending commitments is included in the provision for credit losses on our consolidated statements of

income and the related reserve for unfunded lending commitments is included in other liabilities on our consolidated

balance sheets. See “Note 1—Summary of Significant Accounting Policies” for a description of the methodologies and

policies for determining our allowance for loan and lease losses for each of our loan portfolio segments.

194